Ai Overview

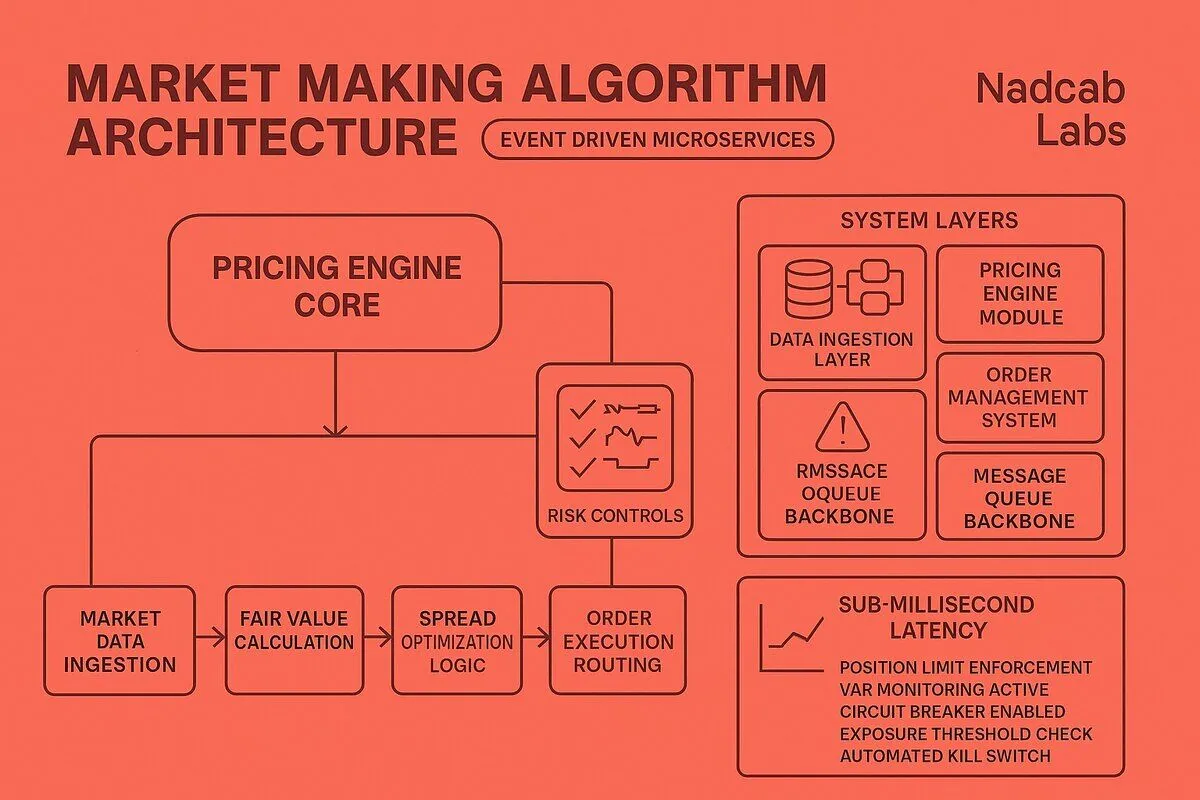

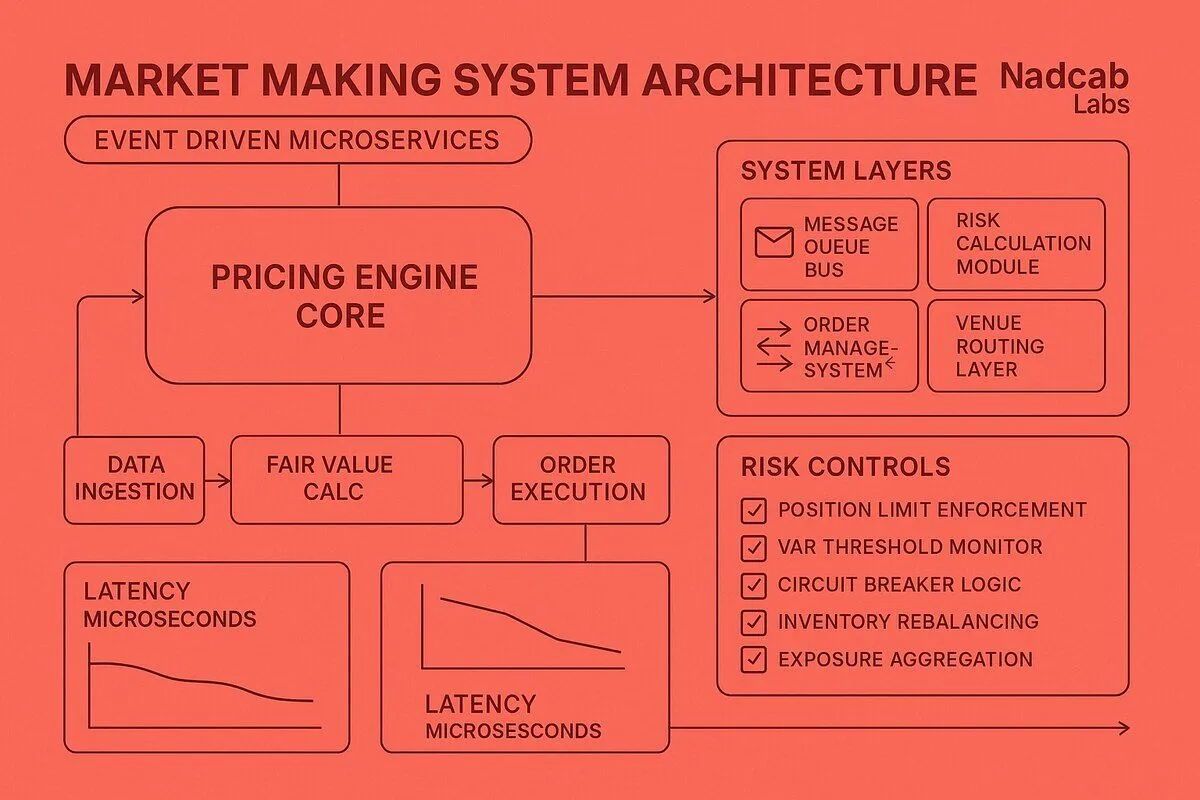

Market making algorithm architecture design in 2026 requires a modular, event-driven system that balances speed, reliability, and risk control. A well-designed architecture separates data ingestion, pricing logic, order management, and risk calculation into independent layers that communicate through asynchronous message queues, enabling sub-millisecond decision cycles and horizontal scalability across multiple trading venues.

Market making algorithm architecture design in 2026 requires a modular, event-driven system that balances speed, reliability, and risk control. A well-designed architecture separates data ingestion, pricing logic, order management, and risk calculation into independent layers that communicate through asynchronous message queues, enabling sub-millisecond decision cycles and horizontal scalability across multiple trading venues.

Key Takeaways

- Modern market making system architecture uses layered design: data ingestion, pricing engine, order management, and risk modules operate as decoupled microservices.

- Event-driven patterns with message queues enable real-time order lifecycle management and low-latency execution routing across venues.

- Pricing algorithm frameworks combine fair value models, dynamic spread logic, and machine learning for adaptive quote optimization.

- Risk calculation modules enforce position limits, VaR monitoring, and automated circuit breakers to protect capital during volatility spikes.

- Latency optimization through co-location, in-memory caching, and kernel bypass techniques is critical for competitive advantage in high-frequency environments.

- Microservices architecture with stateless design, distributed tracing, and chaos engineering ensures resilience and horizontal scalability.

What Are the Core Layers in Market Making Algorithm Architecture Design for 2026?

The foundation of market making algorithm architecture design rests on three primary layers that work in concert to process market data, calculate optimal quotes, and execute trades with minimal latency. Each layer handles a distinct responsibility while maintaining loose coupling through well-defined interfaces.

The data ingestion layer aggregates real-time order book feeds, trade streams, and market depth information from multiple exchanges and liquidity venues. This layer normalizes disparate data formats into a unified schema, filters noise, and maintains a synchronized view of market state. High-throughput message brokers like Apache Kafka or NATS handle the streaming workload, while in-memory data grids cache the most recent snapshots for instant access. The ingestion pipeline must handle burst traffic during volatile periods without dropping messages or introducing latency spikes.

The pricing engine layer consumes normalized market data to calculate fair value, derive bid-ask spreads, and generate dynamic quote adjustments. This layer implements sophisticated algorithms that account for order book imbalance, recent trade flow, inventory position, and volatility estimates. The pricing logic runs continuously in a tight loop, recalculating quotes whenever market conditions change. For blockchain and crypto markets, the pricing engine must also factor in cross-exchange arbitrage opportunities and liquidity fragmentation across decentralized venues.

The order management layer translates pricing decisions into executable orders, routes them to appropriate venues, tracks order lifecycle states, and reconciles positions in real time. This layer maintains an authoritative record of all open orders, filled trades, and current inventory across all trading pairs and venues. It enforces business rules like maximum order size, rate limits per exchange, and position concentration constraints. The order management engine coordinates with the risk calculation module to ensure every action stays within predefined risk parameters.

These three layers communicate through asynchronous event streams rather than synchronous RPC calls, which eliminates blocking and allows each component to scale independently. When the data ingestion layer receives a new order book update, it publishes an event that the pricing engine consumes, recalculates quotes, and publishes a new pricing event that the order management layer acts upon. This event-driven architecture enables the system to handle thousands of updates per second while maintaining deterministic behavior and auditability.

What Pricing Algorithm Frameworks Support Market Making Architecture in 2026?

Pricing algorithm frameworks translate raw market data into actionable bid and ask quotes that balance profitability with competitive positioning. The framework must calculate fair value, determine optimal spreads, and adjust quotes dynamically as market conditions evolve. Modern implementations combine classical quantitative models with machine learning techniques to achieve adaptive behavior.

Fair value models form the anchor for all pricing decisions. The simplest approach uses the mid-price—the average of the best bid and best ask—as the fair value estimate. More sophisticated models incorporate order book imbalance, weighting the fair value toward the side with greater depth to anticipate short-term price movement. Volatility-adjusted spreads widen during periods of high uncertainty to compensate for increased adverse selection risk. For crypto assets with fragmented liquidity, the fair value model may aggregate prices from multiple exchanges, weighting by volume and adjusting for basis differentials.

Dynamic spread management adjusts the distance between bid and ask quotes based on inventory position, recent trade flow, and market microstructure signals. When the market maker accumulates a long position, the algorithm skews quotes by widening the bid and tightening the ask to encourage selling and discourage further buying. This inventory skew mechanism prevents runaway positions and maintains delta neutrality. Adverse selection protection widens spreads when the system detects informed order flow—such as large trades or rapid directional moves—reducing the likelihood of being picked off by better-informed participants. Profit margin optimization balances the trade-off between capture rate (the percentage of time quotes are at the top of the book) and profit per trade, dynamically adjusting spreads to maximize expected revenue.

| Pricing Component | Input Signals | Adjustment Logic | Typical Range |

|---|---|---|---|

| Fair Value | Mid-price, order book depth, cross-exchange prices | Weighted average with imbalance factor | ±0.01% from mid |

| Base Spread | Volatility estimate, tick size, minimum profit target | Scales with realized volatility | 0.05% to 0.30% |

| Inventory Skew | Current position, target inventory, position limits | Linear or exponential penalty function | ±0.02% per unit |

| Adverse Selection | Recent trade direction, order size distribution | Temporary spread widening on detection | +0.05% to +0.15% |

Machine learning integration enhances traditional pricing models by learning patterns from historical data and adapting to regime changes. Predictive pricing models use supervised learning to forecast short-term price movements based on order book features, recent trades, and external signals like funding rates or social sentiment. Reinforcement learning agents optimize quote placement by treating the market making problem as a sequential decision task, learning policies that maximize cumulative profit while respecting risk constraints. Adaptive parameter tuning uses online learning to adjust spread coefficients, inventory skew factors, and risk thresholds in real time as market conditions shift. These ML components run alongside rule-based logic, providing suggestions that are validated against hard constraints before execution. For teams building Market Making Software, integrating ML pipelines into the pricing framework requires careful attention to training data quality, model versioning, and fallback mechanisms when predictions become unreliable.

How Do You Implement Risk Calculation Modules in Market Making System Design for 2026?

Risk calculation modules provide the safety net that prevents catastrophic losses during extreme market events. These modules continuously monitor positions, calculate exposure metrics, and enforce limits that constrain the system’s behavior. A well-designed risk framework operates in real time, evaluating every proposed action before execution and triggering defensive measures when thresholds are breached.

Real-time risk metrics quantify the market maker’s exposure across multiple dimensions. Value-at-Risk (VaR) estimates the maximum expected loss over a given time horizon at a specified confidence level, typically calculated using historical simulation or parametric methods. For derivatives market making, Greeks calculation—delta, gamma, vega, theta—measures sensitivity to underlying price, volatility, and time decay, enabling hedging strategies that neutralize unwanted exposures. Exposure concentration monitoring tracks the percentage of capital allocated to each asset or correlated asset group, flagging over-concentration that could amplify losses during sector-wide moves. These metrics update continuously as positions change, providing a live dashboard of risk posture.

Circuit breakers and kill switches act as automated safeguards that halt trading when risk metrics exceed predefined thresholds. Position limit enforcement prevents any single asset position from growing beyond a maximum size, automatically rejecting new orders that would breach the limit. Drawdown triggers pause trading if cumulative losses over a rolling window exceed a tolerance level, giving operators time to investigate before resuming. Anomaly detection alerts flag unusual patterns—such as a sudden spike in rejected orders, abnormal latency, or a rapid inventory buildup—that may indicate a system malfunction or market manipulation attempt. The kill switch provides a manual override that instantly cancels all open orders and flattens positions, used as a last resort during critical incidents. These mechanisms integrate with the order management engine to ensure enforcement happens before orders reach exchanges.

Risk Metric Monitoring Distribution

Percentage of CPU cycles allocated to each risk calculation task in a typical market making system

Stress testing framework evaluates how the system would perform under extreme scenarios that lie outside normal market conditions. Scenario simulation replays historical crisis events—such as flash crashes or liquidity dry-ups—against the current strategy to estimate potential losses and identify vulnerabilities. Backtesting infrastructure runs the complete algorithm against historical data, measuring performance metrics like Sharpe ratio, maximum drawdown, and profit factor across different market regimes. Performance degradation monitoring tracks latency percentiles, message queue depths, and CPU utilization, alerting when the system approaches resource limits that could compromise execution quality. Regular stress tests inform adjustments to risk parameters and capacity planning for infrastructure scaling. Teams working on Hybrid LLM Architecture for trading assistants can apply similar testing principles to ensure AI-driven decision support remains reliable under stress.

What Microservices Patterns Optimize Market Making Algorithm Architecture in 2026?

Microservices architecture decomposes the monolithic market making system into independent, loosely coupled services that communicate through well-defined APIs and message brokers. This pattern improves scalability, resilience, and development velocity by allowing teams to deploy and scale components independently. However, microservices also introduce complexity in orchestration, observability, and latency management that must be carefully addressed.

Service decomposition divides the system into distinct services: a data ingestion service that normalizes market feeds, a pricing service that calculates quotes, an execution service that manages order placement, a risk service that enforces limits, and a reconciliation service that validates positions against exchange balances. Each service owns its data and exposes a REST or gRPC API for synchronous requests and publishes events to message topics for asynchronous notifications. Clear API contracts define inputs, outputs, and error handling, enabling teams to evolve services independently without breaking downstream consumers. For example, the pricing service might expose an endpoint POST /calculate-quote that accepts market data and returns bid/ask prices, while also publishing a QuoteUpdated event whenever quotes change. This separation allows the execution service to consume quote updates without blocking the pricing calculation loop.

Latency optimization is critical for competitive market making, where microseconds matter. In-memory caching stores frequently accessed data—such as current positions, recent trades, and order book snapshots—in Redis or Hazelcast, eliminating database round trips. Co-location strategies place trading servers in the same data center as exchange matching engines, reducing network latency to sub-millisecond levels. Kernel bypass techniques like DPDK (Data Plane Development Kit) allow applications to process network packets directly, bypassing the operating system’s network stack and cutting latency by 50% or more. For the most latency-sensitive components, FPGA acceleration offloads critical path logic—such as order book updates or risk checks—to hardware, achieving nanosecond-scale processing. These optimizations apply selectively to hot paths where latency directly impacts profitability, while less critical services like reporting or analytics run on standard infrastructure. The same principles of low-latency design that apply to market making also inform ai chatbot architecture for real-time conversational systems.

Scalability and resilience ensure the system handles growing trading volumes and recovers gracefully from failures. Horizontal scaling adds more instances of stateless services—such as pricing or execution workers—behind a load balancer, distributing load as traffic increases. Stateful services like the order management engine use sharding or partitioning strategies to divide work across instances, with each instance responsible for a subset of trading pairs or venues. Distributed tracing with tools like Jaeger or Zipkin instruments every request with a trace ID that flows through all services, enabling operators to diagnose performance bottlenecks and failures across the service mesh. Chaos engineering practices deliberately inject failures—such as killing service instances, introducing network delays, or corrupting messages—to validate that the system degrades gracefully and recovers automatically. Health checks and circuit breakers prevent cascading failures by isolating unhealthy services and rerouting traffic to healthy instances.

For blockchain-focused market making, microservices architecture must also account for the unique characteristics of decentralized exchanges and on-chain settlement. A dedicated blockchain connector service manages wallet interactions, transaction signing, and gas price optimization, abstracting these details from the core trading logic. This service monitors pending transactions, handles nonce management to prevent conflicts, and implements retry logic for failed submissions. Integrating Real Estate Tokenization Explained concepts into market making for tokenized assets requires additional services for custody, compliance checks, and fractional ownership tracking. The modular nature of microservices makes it straightforward to add these specialized components without disrupting existing trading operations. Similarly, lessons from Web3 Architecture inform how to design resilient connectors for decentralized protocols, while ICO Platform architecture provides patterns for managing token lifecycle events that affect pricing and liquidity.

Security and compliance considerations permeate the microservices design. Service-to-service authentication uses mutual TLS or JWT tokens to ensure only authorized components can invoke sensitive operations. Function Visibility in Smart Contracts principles guide the design of access control for on-chain interactions, ensuring that only the execution service can submit trades from the market maker’s wallet. Audit logging captures every significant event—order submission, fill, cancellation, risk limit breach—with immutable timestamps and cryptographic signatures, supporting regulatory reporting and forensic analysis. blockchain KYC AML compliance architecture integrates into the onboarding and transaction monitoring flows, screening counterparties and flagging suspicious activity. For firms offering Prediction Market Development services, similar compliance infrastructure ensures that market making activities adhere to jurisdiction-specific regulations.

Frequently Asked Questions

Q1.What algorithms do market makers use in 2026?

In 2026, market makers deploy statistical arbitrage, mean reversion, order book imbalance detection, and reinforcement learning algorithms. These strategies optimize bid-ask spreads, predict short-term price movements, and dynamically adjust inventory. Machine learning models analyze order flow patterns, while high-frequency trading algorithms execute microsecond-level trades. Nadcab Labs integrates adaptive algorithms that respond to real-time volatility and liquidity conditions across decentralized and centralized exchanges.

Q2.How do you design a low-latency order management engine for market making in 2026?

In 2026, low-latency order management engines use in-memory databases, kernel bypass networking (DPDK), and FPGA acceleration to minimize execution delays. Asynchronous event-driven architecture handles thousands of orders per second. Co-location with exchange servers reduces network latency. Nadcab Labs designs engines with sub-millisecond order routing, real-time position tracking, and failover mechanisms to ensure continuous operation and rapid response to market changes.

Q3.What are the key components of a market making algorithm architecture in 2026?

In 2026, key components include order management systems, pricing engines, risk management modules, market data feeds, inventory control, and execution gateways. Real-time analytics, machine learning models, and backtesting frameworks support strategy optimization. Nadcab Labs structures architectures with modular design, enabling independent scaling of components. APIs integrate multiple exchanges, while monitoring dashboards provide visibility into performance, latency, and profitability metrics.

Q4.How does microservices architecture improve market making system scalability in 2026?

In 2026, microservices architecture decouples pricing, execution, risk management, and data ingestion into independent services. Each microservice scales horizontally based on demand, improving fault tolerance and deployment flexibility. Containerization (Docker, Kubernetes) enables rapid updates without system downtime. Nadcab Labs uses microservices to isolate critical functions, optimize resource allocation, and maintain high availability. This modularity accelerates development cycles and supports multi-exchange connectivity.

Q5.What risk management modules are essential in market making algorithm design for 2026?

In 2026, essential modules include position limit controls, real-time P&L tracking, volatility monitors, exposure alerts, and circuit breakers. Automated stop-loss mechanisms prevent excessive losses during market shocks. Stress testing and scenario analysis evaluate portfolio resilience. Nadcab Labs integrates compliance checks, margin monitoring, and liquidity risk assessments. These modules ensure market makers operate within regulatory boundaries while protecting capital and maintaining stable spreads.

Q6.How do you integrate machine learning into market making pricing frameworks in 2026?

In 2026, machine learning models predict optimal bid-ask spreads, forecast order flow imbalances, and detect market regime changes. Supervised learning trains on historical tick data; reinforcement learning optimizes dynamic pricing strategies. Feature engineering incorporates volatility, volume, and order book depth. Nadcab Labs deploys ML pipelines with real-time inference engines, continuous model retraining, and A/B testing. Integration via APIs ensures pricing frameworks adapt instantly to evolving market conditions.

Explore Services

Related Services

Reviewed by

Naman Singh

Co-Founder & CEO, Nadcab Labs

Naman Singh is the Co-Founder and CEO of Nadcab Labs, where he drives the company’s vision, global growth, and strategic expansion in blockchain, fintech, and digital transformation. A serial entrepreneur, Naman brings deep hands-on experience in building, scaling, and commercializing technology-driven businesses. At Nadcab Labs, Naman works closely with enterprises, governments, and startups to design and implement secure, scalable, and business-ready Web3 and blockchain solutions. He specializes in transforming complex ideas into high-impact digital products aligned with real business objectives. Naman has led the development of end-to-end blockchain ecosystems, including token creation, smart contracts, DeFi and NFT platforms, payment infrastructures, and decentralized applications. His expertise extends to tokenomics design, regulatory alignment, compliance strategy, and go-to-market planning—helping projects become investor-ready and built for long-term sustainability. With a strong focus on real-world adoption, Naman believes in building blockchain solutions that deliver measurable value, solve practical problems, and unlock new growth opportunities for organizations worldwide.