Ai Overview

Building a compliant crypto exchange in 2026 requires robust identity verification infrastructure from day one. Biometric matching algorithms then compare the live selfie against the photo on the submitted document, achieving accuracy rates above 98% when properly calibrated. Users can begin exploring the platform immediately, but face strict withdrawal limits typically capped at $1,000-$2,000 equivalent per day.

Building a compliant crypto exchange in 2026 requires robust identity verification infrastructure from day one. Know Your Customer (KYC) systems form the regulatory backbone of any legitimate trading platform, protecting users from fraud while ensuring the exchange meets global Anti-Money Laundering (AML) standards. A well-designed crypto exchange KYC implementation balances regulatory requirements with user experience, enabling rapid onboarding without compromising security or privacy.

Key Takeaways

- Multi-tier KYC verification systems allow exchanges to offer progressive access based on user risk profiles and transaction volumes

- Automated document validation workflows reduce manual review burden by 70-80% while maintaining compliance accuracy

- Real-time AML screening integration with sanctions databases (OFAC, UN, EU) is mandatory for institutional-grade exchanges

- Mobile-first KYC flows with liveness detection can achieve sub-3-minute completion times without sacrificing security

- Ongoing monitoring and periodic re-verification are critical for maintaining compliance as regulatory requirements evolve

- Proper PII encryption and GDPR/CCPA-compliant data architecture protect both users and exchanges from regulatory penalties

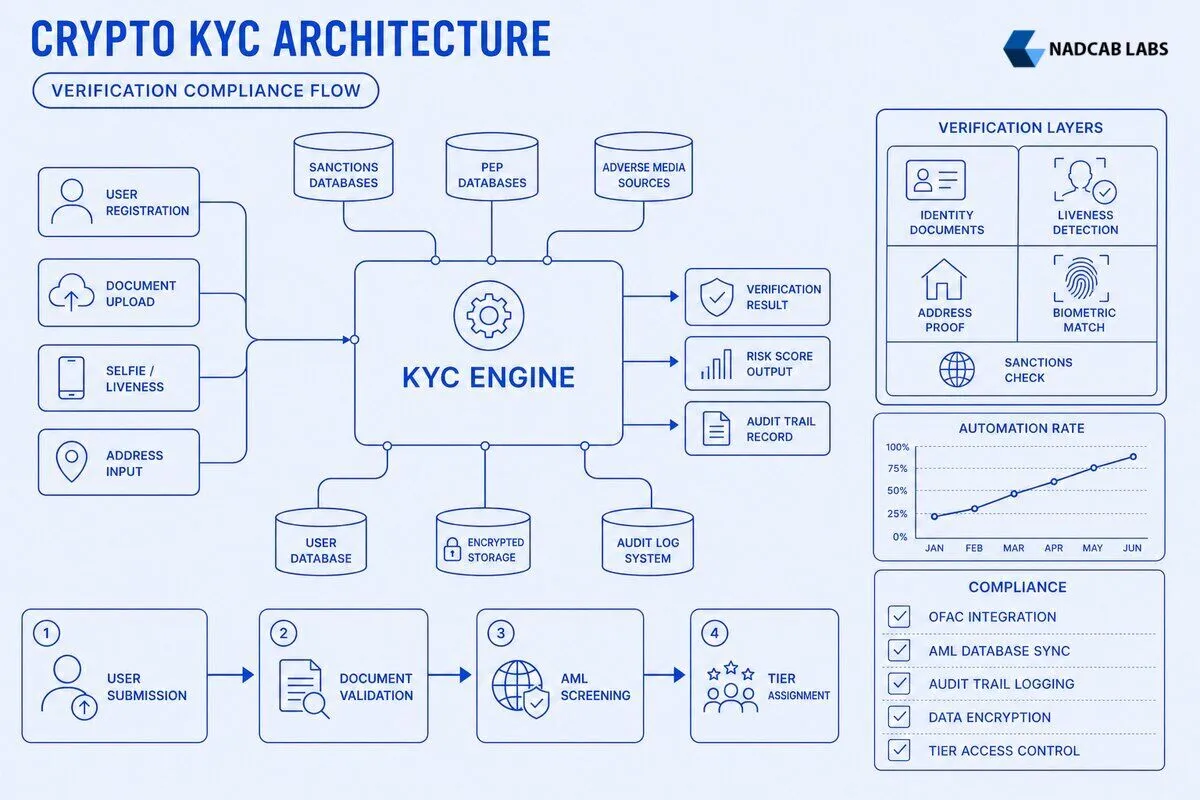

What Are the Core Components of a Crypto Exchange KYC System?

A production-grade KYC verification system comprises three interconnected layers that work together to validate user identity while managing risk. The identity verification layer handles document capture, biometric matching, and liveness detection. Modern systems use AI-powered optical character recognition (OCR) to extract data from government-issued IDs, passports, and driver’s licenses across 200+ countries. Liveness detection prevents spoofing attacks by requiring users to perform real-time actions during selfie capture, such as turning their head or blinking. Biometric matching algorithms then compare the live selfie against the photo on the submitted document, achieving accuracy rates above 98% when properly calibrated.

The risk assessment engine sits at the heart of crypto exchange compliance infrastructure. This component assigns each user to a verification tier based on their transaction history, geographic location, and intended trading volume. The engine continuously evaluates users against AML screening databases, including sanctions lists maintained by the Office of Foreign Assets Control (OFAC), United Nations Security Council, and European Union. Politically Exposed Persons (PEP) lists are checked to identify individuals who may pose higher corruption or money laundering risks. Advanced systems incorporate machine learning models that analyze behavioral patterns to detect suspicious activity before it escalates.

Data storage and encryption architecture must meet stringent regulatory standards while remaining operationally efficient. Personally Identifiable Information (PII) should be encrypted at rest using AES-256 encryption and in transit via TLS 1.3. Many exchanges implement field-level encryption for the most sensitive data points, such as government ID numbers and biometric templates. Geographic data residency requirements under GDPR mandate that EU citizen data be stored within the European Economic Area, while California Consumer Privacy Act (CCPA) imposes specific disclosure and deletion obligations. A Cryptocurrency Exchange Development Company typically implements multi-region database clusters with automated compliance controls to handle these requirements transparently.

The integration layer connects your KYC system to third-party verification providers, blockchain analytics tools, and regulatory reporting systems. Most exchanges use a combination of specialized vendors: document verification providers like Onfido or Jumio, biometric services from providers like iProov, and AML screening from Chainalysis or Elliptic. The architecture must support webhook-based callbacks for asynchronous verification results, maintain audit logs for every verification attempt, and provide compliance officers with a unified dashboard to review flagged cases. Proper API rate limiting and fallback mechanisms ensure the system remains operational even if a vendor experiences downtime.

| Component | Primary Function | Typical Accuracy | Processing Time |

|---|---|---|---|

| Document OCR | Extract text and data from ID documents | 95-99% | 2-5 seconds |

| Liveness Detection | Verify user is physically present during capture | 98-99.5% | 3-8 seconds |

| Biometric Matching | Compare selfie to document photo | 97-99% | 1-3 seconds |

| AML Screening | Check against sanctions and PEP lists | 99.9% | 0.5-2 seconds |

| Address Verification | Validate proof of residence documents | 92-96% | 10-30 seconds |

Compliance reporting modules generate audit trails for regulatory examinations and support Suspicious Activity Report (SAR) filing when required. These systems must capture every verification attempt, document upload, and risk assessment decision with immutable timestamps. Many jurisdictions require exchanges to retain KYC records for five to seven years after account closure. Implementing proper data lifecycle management ensures you can produce required documentation during audits while automatically purging data when legally permitted. The failed crypto exchanges that faced regulatory shutdowns often lacked adequate audit trail infrastructure, making it impossible to demonstrate compliance during investigations.

How Do You Design Multi-Tier KYC Verification Levels?

Tier-based KYC architecture allows exchanges to balance user acquisition speed with regulatory risk management. Tier 1 verification, often called Basic or Light KYC, requires only email and phone number confirmation. Users can begin exploring the platform immediately, but face strict withdrawal limits typically capped at $1,000-$2,000 equivalent per day. This tier serves as a conversion funnel, allowing curious users to experience the platform before committing to full verification. The friction is minimal: a six-digit code sent via SMS or email, completed in under 60 seconds. Some exchanges implement additional device fingerprinting at this stage to detect fraud patterns without requiring explicit user action.

Tier 2 verification, the Intermediate or Standard level, forms the core of most exchange KYC flows. Users upload a government-issued ID and complete a selfie verification with liveness detection. OCR extracts name, date of birth, document number, and expiration date, cross-referencing these against the user’s registration data. Any discrepancy triggers a manual review flag. Transaction limits increase substantially at this tier, often to $50,000-$100,000 daily for withdrawals and unlimited deposits. The entire flow takes 2-5 minutes for users with clear documents and good lighting. Approval typically occurs within 10-30 minutes for automated cases, though manual reviews may extend to 24-48 hours during peak periods.

Tier 3 verification, reserved for Advanced or Institutional users, demands comprehensive documentation including proof of address and source of funds. Utility bills, bank statements, or government correspondence dated within the past three months serve as address verification. Source of funds documentation varies by jurisdiction but typically includes employment letters, tax returns, or business registration documents for corporate accounts. This tier unlocks unlimited trading volumes and access to over-the-counter (OTC) desks, margin trading, and institutional custody services. The verification process may take 3-7 business days due to manual review requirements, but high-value users accept this friction in exchange for premium features. A Tier-1 exchange typically requires this level of verification for any user conducting transactions above $250,000 monthly.

Email + Phone

$2,000/day limit

60 seconds

ID + Selfie

$50,000/day limit

2-5 minutes

Address + Source of Funds

Unlimited

3-7 days

The tier structure must align with your target market and regulatory environment. US-based exchanges operating under FinCEN regulations often collapse Tier 1 and 2 into a single mandatory KYC flow, as the Bank Secrecy Act requires identity verification before any trading activity. European exchanges under the Markets in Crypto-Assets (MiCA) framework have more flexibility but must implement enhanced due diligence for transactions above €1,000. Indian exchanges following Virtual Digital Asset (VDA) regulations require full KYC before any deposit or trade, eliminating the concept of a basic tier entirely. Your architecture should support jurisdiction-specific configuration without code changes, using feature flags and rule engines to adjust verification requirements dynamically.

Progressive tier upgrades should feel natural rather than punitive. When a Tier 1 user attempts a withdrawal exceeding their limit, the system should present a clear upgrade path with estimated completion time and required documents. Many successful exchanges implement “pre-verification” where users can upload documents before needing higher limits, reducing friction at the critical moment when they want to move funds. Analytics show that users who complete Tier 2 verification within their first session have 3-4x higher lifetime value than those who delay. Smart UX design treats KYC as an enabler of better service rather than a regulatory burden.

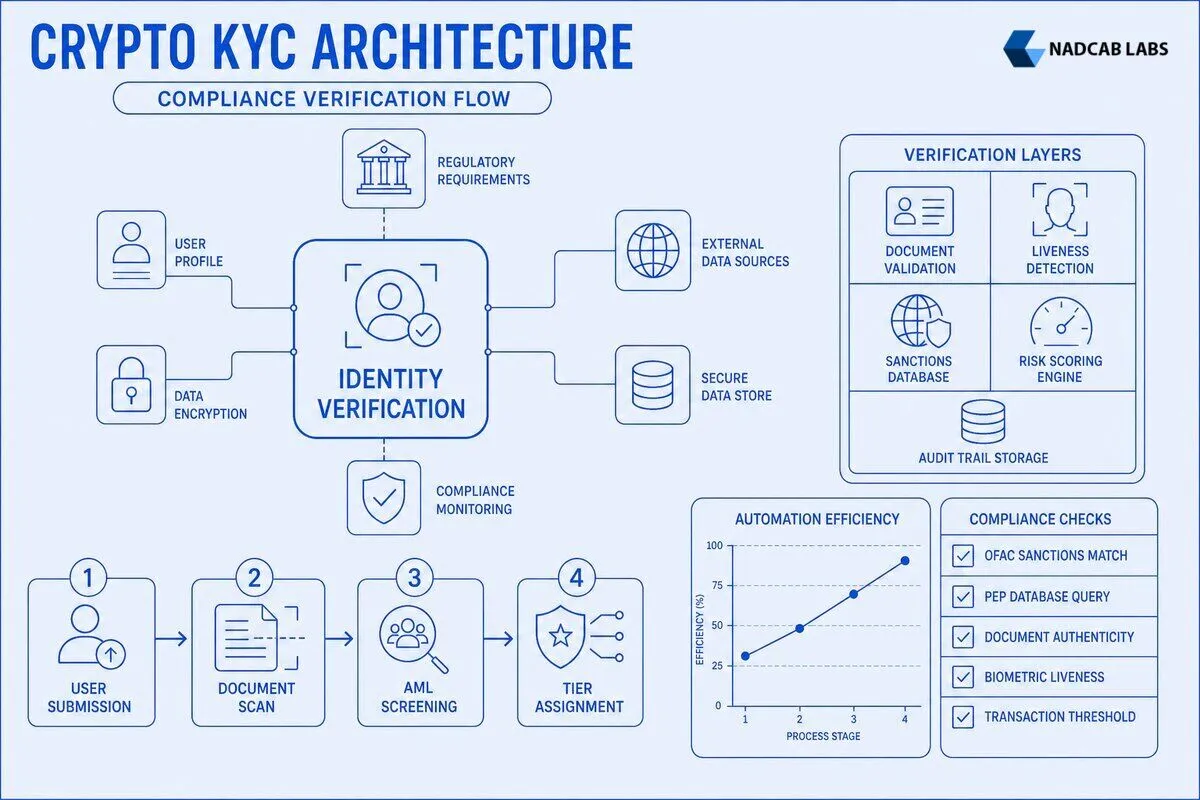

What Is the Step-by-Step Document Validation Workflow?

Document validation begins the moment a user uploads an ID image. The system first performs basic quality checks: sufficient resolution (minimum 300 DPI equivalent), proper orientation, and adequate lighting. Blurry images, screenshots, or photos of screens are automatically rejected with specific feedback guiding the user to recapture. Modern mobile SDKs provide real-time feedback during capture, using edge detection to ensure the document fills the frame and warning users about glare or shadows before they submit. This front-end validation reduces failed submissions by 40-50%, decreasing frustration and support tickets.

Once an image passes quality gates, OCR engines extract structured data from the document. These systems recognize over 10,000 document types across 200+ countries, handling variations in layout, language, and security features. The OCR output includes not just text fields but also confidence scores for each extracted value. A confidence score below 0.85 typically triggers manual review. The system compares extracted data against the user’s registration information, flagging mismatches in name spelling, date of birth, or document number. Minor discrepancies like middle name omission or name order variations are handled via fuzzy matching algorithms, while significant conflicts halt the verification process pending user correction.

Security feature validation runs in parallel with OCR. Modern IDs contain multiple anti-counterfeiting elements: holograms, UV-reactive ink, microprinting, and embedded chips. Document verification providers maintain databases of these features for each document type, checking uploaded images for their presence and correct positioning. Machine learning models trained on millions of genuine and fraudulent documents detect subtle manipulation indicators invisible to human reviewers. The system flags documents with inconsistent shadows, cloned backgrounds, or pixel-level anomalies suggesting digital editing. These checks catch 90-95% of forged documents before they reach human review, though sophisticated forgeries still require expert examination.

Resolution, orientation, lighting validation

Parse name, DOB, document number, expiry

Hologram, UV ink, microprint verification

Compare extracted data vs. registration info

Selfie capture, face comparison, spoof detection

Compliance officer examination, decision logging

Liveness detection and biometric matching form the final automated validation stage. The user captures a selfie using their device camera while the system monitors for signs of presentation attacks: printed photos, digital screens, masks, or deepfake videos. Active liveness checks require the user to perform random actions like turning their head left, smiling, or blinking, making pre-recorded videos ineffective. Passive liveness uses AI to detect subtle cues like micro-expressions, eye movement patterns, and 3D depth information that distinguish live humans from spoofing attempts. Once liveness is confirmed, facial recognition algorithms compare the selfie to the photo on the submitted ID, generating a similarity score. Scores above 0.90 typically result in automatic approval, while scores between 0.75-0.90 may trigger manual review depending on risk tolerance.

The manual review queue handles edge cases that automated systems cannot confidently resolve. Compliance officers see a dashboard displaying the user’s submitted documents, extracted data, confidence scores, and any system flags. They can zoom into high-resolution images, toggle between different lighting filters to examine security features, and access historical data for users with previous verification attempts. Each review decision is logged with a timestamp, officer ID, and written justification for audit purposes. Well-designed review interfaces present information in a standardized format regardless of document type, reducing cognitive load and improving decision consistency. Average review time for flagged cases ranges from 2-5 minutes, with complex cases involving institutional accounts or high-risk jurisdictions taking 15-30 minutes.

Rejection handling requires clear communication and a path to resolution. When a document fails verification, the system should explain why in plain language: “The photo on your ID is not clear enough for us to verify your identity” rather than “Biometric match confidence below threshold.” Users should be able to resubmit immediately with guidance on how to avoid the same issue. Some exchanges implement a “three strikes” policy where repeated failures trigger a temporary lockout and mandatory support contact, preventing automated fraud attempts while allowing genuine users to succeed. The RPA architecture design patterns used in document processing can be adapted to handle high-volume verification workflows efficiently.

How Do You Integrate AML Screening and Sanctions Monitoring?

Real-time AML screening begins at account creation and continues throughout the user lifecycle. When a user submits their identity information, the system immediately queries sanctions databases via API. The primary lists include OFAC’s Specially Designated Nationals (SDN) list covering US sanctions, the UN Security Council Consolidated List, EU Consolidated Financial Sanctions List, and UK HM Treasury sanctions list. Each query returns potential matches based on name, date of birth, and nationality. The matching algorithm must handle name variations, transliterations, and partial matches, as sanctioned individuals often appear in databases with multiple spellings or aliases.

Politically Exposed Persons (PEP) screening adds another risk layer. PEPs include current and former government officials, senior executives of state-owned enterprises, and their immediate family members. While PEP status alone does not prohibit account opening, it triggers enhanced due diligence requirements. The exchange must document the source of the PEP’s wealth, understand their expected transaction patterns, and apply increased monitoring to their activity. Commercial PEP databases like World-Check, Dow Jones Risk & Compliance, or ComplyAdvantage maintain records of millions of individuals globally, updated daily as political appointments change. Integration typically occurs via RESTful APIs with response times under two seconds, allowing real-time screening without degrading user experience.

Adverse media screening searches news sources, regulatory announcements, and court records for negative information about users. This catches individuals involved in financial crimes, corruption, or fraud who may not yet appear on official sanctions lists. Natural language processing algorithms scan millions of articles daily, identifying mentions of money laundering, terrorist financing, bribery, or other financial crimes. The system assigns risk scores based on the severity and recency of adverse media hits. A single mention in a local news article from five years ago carries less weight than multiple recent reports in major financial publications. Compliance officers review high-risk hits to determine if they warrant account restrictions or additional investigation.

AML Screening Coverage by Database Type

Transaction monitoring rules detect suspicious patterns in real-time trading activity. Velocity checks flag users who suddenly increase their transaction volume or frequency beyond established baselines. A user who typically trades $5,000 weekly but suddenly withdraws $50,000 triggers an alert for manual review. Structuring detection identifies users splitting large transactions into smaller amounts to avoid reporting thresholds, a classic money laundering technique. Geographic risk rules monitor for transactions involving high-risk jurisdictions identified by the Financial Action Task Force (FATF) as having strategic AML deficiencies. The crypto derivatives risk management system architecture shares similar pattern detection logic, adapted for compliance rather than market risk.

Ongoing screening ensures compliance as circumstances change. Sanctions lists update daily, with new individuals and entities added as geopolitical situations evolve. Your system must re-screen all active users against updated lists automatically, typically running batch processes during low-traffic hours. When a match is found, the account is immediately frozen pending investigation. Users who become PEPs after account opening must be identified and subjected to enhanced monitoring. Some exchanges implement annual re-verification, requiring users to resubmit identity documents and update their information. This catches expired documents, changed addresses, and evolved risk profiles that initial screening missed.

The integration architecture must support multiple vendor APIs while maintaining system resilience. Implement circuit breakers that prevent cascade failures if a screening provider experiences downtime. Cache negative screening results for a short period (typically 24 hours) to reduce API costs and improve response times for repeat queries. Use asynchronous processing for non-critical screenings, allowing user onboarding to proceed while background checks complete. Maintain detailed logs of every screening query, result, and subsequent action for regulatory reporting. Many jurisdictions require exchanges to demonstrate they screened users before allowing transactions, making audit trails essential for proving compliance during examinations.

How Can You Optimize KYC User Experience Without Compromising Compliance?

Progressive disclosure collects information incrementally based on actual user needs rather than front-loading every possible data point. A new user exploring the platform does not need to provide their home address until they attempt a withdrawal exceeding basic tier limits. This approach reduces initial friction while maintaining the ability to collect required information when regulatory triggers occur. The system tracks which data points are missing for each user and prompts collection at contextually appropriate moments. A user viewing margin trading features might see a banner explaining that Tier 3 verification is required to access those tools, with a one-click path to begin the upgrade process.

Mobile-first design recognizes that 60-70% of new exchange users register via smartphone. Native mobile SDKs provide superior camera access, real-time image quality feedback, and guided capture experiences compared to mobile web implementations. The SDK can automatically detect document edges, adjust focus and exposure, and capture images at optimal resolution without user intervention. Liveness detection works more reliably with native camera access, enabling passive checks that do not require explicit user actions. Push notifications inform users when their verification is complete, eliminating the need to repeatedly check status. The entire flow from document capture to approval should complete in under three minutes for straightforward cases, with 80%+ of submissions approved automatically.

Clear communication throughout the KYC process reduces abandonment and support burden. Explain why verification is required in plain language: “To protect you and comply with financial regulations, we need to verify your identity before you can withdraw funds.” Provide estimated completion times at each stage: “Most verifications complete within 10 minutes, though some may take up to 24 hours.” Display real-time progress indicators showing which steps are complete and what remains. When documents are rejected, give specific, actionable feedback rather than generic error messages. “Your ID photo was too blurry. Please retake the photo in good lighting, making sure all text is clearly readable” helps users succeed on the next attempt.

Privacy assurances address user concerns about sharing sensitive documents. Clearly state how data will be used, who has access, and how long it will be retained. “Your documents are encrypted and stored securely. Only authorized compliance staff can view them, and they will be deleted seven years after you close your account.” Link to your detailed privacy policy and data protection practices. Display security badges from recognized auditors like SOC 2 or ISO 27001. Some exchanges allow users to download a copy of all data held about them, demonstrating transparency and building trust. The Fiat & Crypto infrastructure integration guide covers data handling best practices across payment systems.

Pre-verification options let users complete KYC before they need higher limits, smoothing the upgrade path. When a new user registers, offer an optional “Verify Now” flow that unlocks full platform features immediately. Users who choose to skip can still explore with basic tier access, but those who verify upfront avoid friction later when they want to make their first withdrawal. Analytics show that users who verify within their first session have 40% higher conversion rates to active traders. The key is making verification feel like unlocking value rather than jumping through hoops.

Smart defaults and autofill reduce manual data entry. When OCR extracts data from an ID, pre-populate form fields with that information rather than making users type it again. Use address autocomplete APIs to help users enter their residence quickly and accurately. Remember device information so returning users do not need to re-verify on the same phone or computer. Implement single sign-on (SSO) for users who have completed KYC on related platforms, allowing identity portability where regulations permit. Every second saved in the verification flow increases completion rates by 1-2%.

A/B testing reveals which UX patterns drive highest completion rates. Test different onboarding sequences: some users respond better to verification-first flows, while others prefer exploring the platform before committing to KYC. Experiment with incentives like reduced trading fees or bonus rewards for users who complete verification within 24 hours of registration. Monitor drop-off points in the funnel and iterate on the most problematic steps. The best crypto exchange platforms continuously optimize their KYC flows based on data, achieving completion rates above 85% for users who begin the process.

Support infrastructure must handle verification issues quickly. Implement live chat or chatbot assistance during the KYC flow, answering common questions without requiring users to leave the process. Train support staff on document requirements for different countries, common rejection reasons, and how to guide users to successful submission. Create a self-service knowledge base with country-specific guides, example photos of properly captured documents, and troubleshooting tips. Fast, helpful support during verification builds user confidence and reduces abandonment, especially for users in regions with less common document types.

Compliance and UX need not be opposing forces. The most successful exchanges treat KYC as a trust-building opportunity rather than a necessary evil. Users who complete verification feel more confident depositing significant funds, knowing the platform takes security seriously. Clear communication about why KYC exists and how it protects users transforms a regulatory requirement into a competitive advantage. Working with a p2p cryptocurrency exchange development team experienced in compliance can help you design flows that satisfy both regulators and users, avoiding the painful redesigns that plague exchanges built without compliance expertise.

Final Thoughts

Implementing a robust KYC verification system requires balancing regulatory compliance, security, and user experience across multiple dimensions. Multi-tier architectures allow exchanges to serve different user segments while maintaining appropriate risk controls. Automated document validation workflows handle the majority of verifications without manual intervention, but human review remains essential for edge cases and high-risk scenarios. Real-time AML screening and ongoing monitoring protect your platform from financial crime while demonstrating regulatory compliance. Mobile-first design and progressive disclosure optimize conversion rates without compromising the thoroughness of identity verification. The technical architecture must support multiple verification vendors, handle high volumes, and maintain detailed audit trails for regulatory examinations. As regulations continue to evolve globally, building flexible KYC infrastructure from the start enables your exchange to adapt quickly to new requirements. Partnering with experienced Crypto Derivatives Exchange Development teams ensures your compliance systems meet institutional standards while providing the seamless experience retail users expect. The exchanges that succeed long-term treat KYC not as a barrier but as foundational infrastructure that enables trust, security, and sustainable growth in an increasingly regulated market.

Frequently Asked Questions

Q1.What documents are required for crypto exchange KYC verification?

Crypto exchanges typically require government-issued photo ID (passport, driver’s license, or national ID card), proof of address (utility bill or bank statement dated within 90 days), and a selfie for liveness verification. Institutional accounts need additional corporate documents including business registration, beneficial ownership declarations, and authorized signatory lists. Enhanced due diligence may require source of funds documentation and tax identification numbers depending on jurisdiction and transaction volumes.

Q2.How long does KYC approval take on a crypto exchange?

Automated KYC verification typically completes within 5-15 minutes using AI-powered document verification and facial recognition systems. Manual review cases requiring human intervention take 24-72 hours. Complex institutional KYC or enhanced due diligence can extend to 5-10 business days. Processing time depends on document quality, jurisdiction-specific checks, sanctions screening complexity, and current verification queue volume. Nadcab Labs implements tiered verification systems optimizing approval speed while maintaining compliance.

Q3.Can I trade on a crypto exchange without completing KYC?

Most regulated exchanges require basic KYC before any trading. Some platforms offer limited functionality without KYC—typically allowing deposits and small withdrawals (under $1,000-$2,000 daily) but restricting fiat operations and advanced features. Decentralized exchanges (DEXs) operate without KYC but lack fiat on-ramps. Regulatory frameworks like MiCA in Europe and FinCEN guidance in the US increasingly mandate KYC for all centralized platforms, making non-KYC trading options scarce on compliant exchanges.

Q4.What is the difference between KYC and AML in crypto exchanges?

KYC (Know Your Customer) is the identity verification process collecting and validating user information—name, address, ID documents. AML (Anti-Money Laundering) is the broader compliance framework monitoring transactions for suspicious patterns, conducting ongoing due diligence, and reporting to financial authorities. KYC is a component of AML. While KYC happens at onboarding, AML includes continuous transaction monitoring, sanctions screening, risk scoring, and suspicious activity reporting throughout the customer relationship.

Q5.How do crypto exchanges verify identity documents?

Exchanges use multi-layer verification: OCR technology extracts data from document images, AI algorithms detect forgeries by analyzing security features (holograms, microprinting, UV elements), and database checks validate document authenticity against government registries. Liveness detection prevents photo spoofing through random movement prompts. Biometric facial matching compares selfies to ID photos. Advanced systems cross-reference data against sanctions lists, PEP databases, and adverse media. Nadcab Labs integrates third-party verification APIs with proprietary risk engines.

Q6.Are my personal documents safe during KYC verification on exchanges?

Reputable exchanges implement bank-grade security: end-to-end encryption for data transmission, AES-256 encryption for storage, and segregated databases with role-based access controls. Documents are stored in SOC 2 Type II certified infrastructure with regular security audits. Leading platforms use tokenization, storing hashed references rather than raw documents. GDPR and data protection regulations mandate secure handling and right-to-deletion. However, exchange breaches have occurred—verify platform security certifications, insurance coverage, and compliance track record before submitting sensitive information.

Explore Services

Related Services

Reviewed by

Naman Singh

Co-Founder & CEO, Nadcab Labs

Naman Singh is the Co-Founder and CEO of Nadcab Labs, where he drives the company’s vision, global growth, and strategic expansion in blockchain, fintech, and digital transformation. A serial entrepreneur, Naman brings deep hands-on experience in building, scaling, and commercializing technology-driven businesses. At Nadcab Labs, Naman works closely with enterprises, governments, and startups to design and implement secure, scalable, and business-ready Web3 and blockchain solutions. He specializes in transforming complex ideas into high-impact digital products aligned with real business objectives. Naman has led the development of end-to-end blockchain ecosystems, including token creation, smart contracts, DeFi and NFT platforms, payment infrastructures, and decentralized applications. His expertise extends to tokenomics design, regulatory alignment, compliance strategy, and go-to-market planning—helping projects become investor-ready and built for long-term sustainability. With a strong focus on real-world adoption, Naman believes in building blockchain solutions that deliver measurable value, solve practical problems, and unlock new growth opportunities for organizations worldwide.