Ai Overview

Valuing a tokenized real estate asset is fundamentally different from appraising a traditional property because the underlying asset is fractional, programmable, and traded on-chain. If a commercial building worth $10 million is tokenized into one million tokens, each token’s intrinsic value starts at $10. Discounted cash flow analysis for a whole property assumes the investor controls 100% of the asset’s cash flows and can make unilateral decisions about capital improvements, refinancing, or sale.

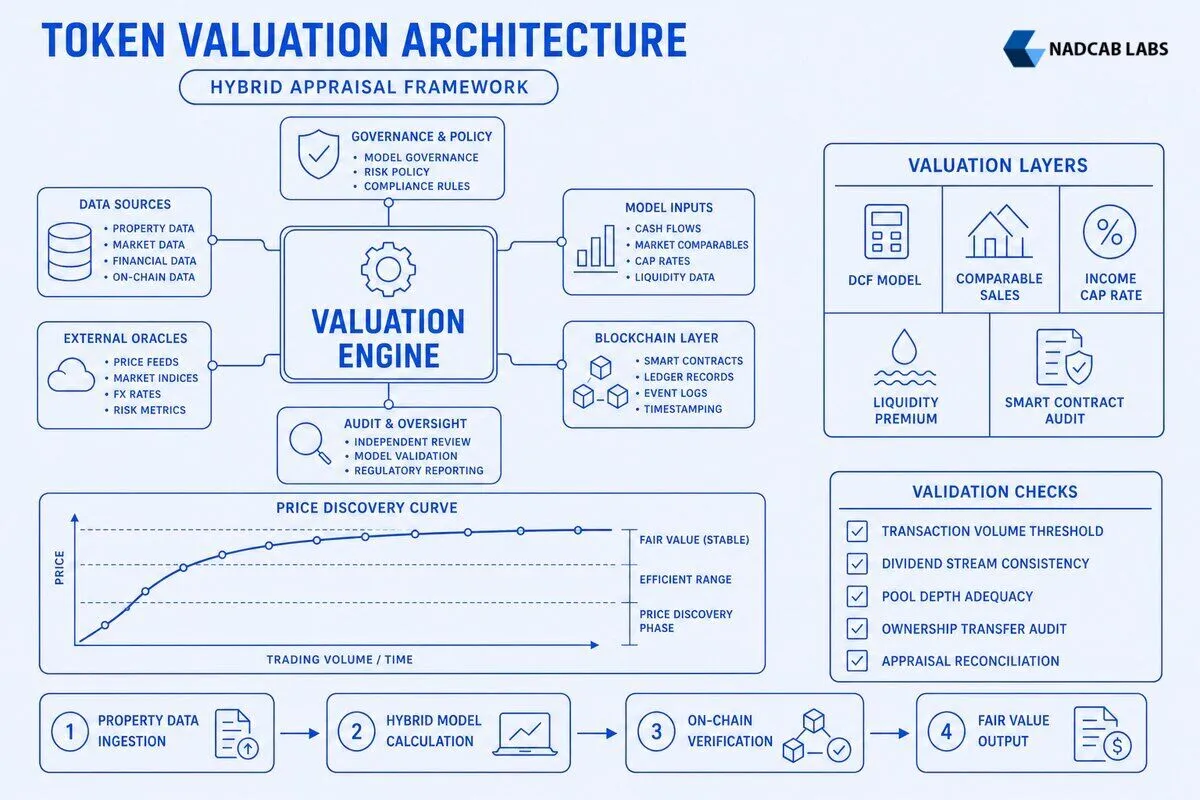

Valuing a tokenized real estate asset is fundamentally different from appraising a traditional property because the underlying asset is fractional, programmable, and traded on-chain. Real estate token valuation methods blend classical appraisal techniques—discounted cash flow, comparable sales, income capitalization—with blockchain-native metrics like on-chain transaction volume, smart contract-enforced dividend streams, and liquidity pool depth. This technical framework explains how investors, auditors, and platforms determine fair market value for property tokens in a transparent, automated environment where every ownership transfer and rental payout is recorded immutably

Key Takeaways

- Traditional valuation methods (DCF, comparable sales, income cap) require adjustment for fractional ownership, liquidity premiums, and smart contract automation.

- On-chain transaction data—secondary trades, rental distributions, ownership transfers—provides real-time pricing signals that off-chain appraisals cannot match.

- Net Asset Value per token is the preferred baseline for tokenized funds, calculated from underlying property appraisals minus liabilities and fees.

- Hybrid frameworks combine classical property fundamentals with blockchain metrics (trading volume, liquidity depth) to produce more accurate, transparent valuations.

- Accurate valuation underpins investor confidence, regulatory compliance, and the long-term viability of Real Estate Tokenization platforms.

How Do Traditional Real Estate Valuation Methods Translate to Tokenized Assets

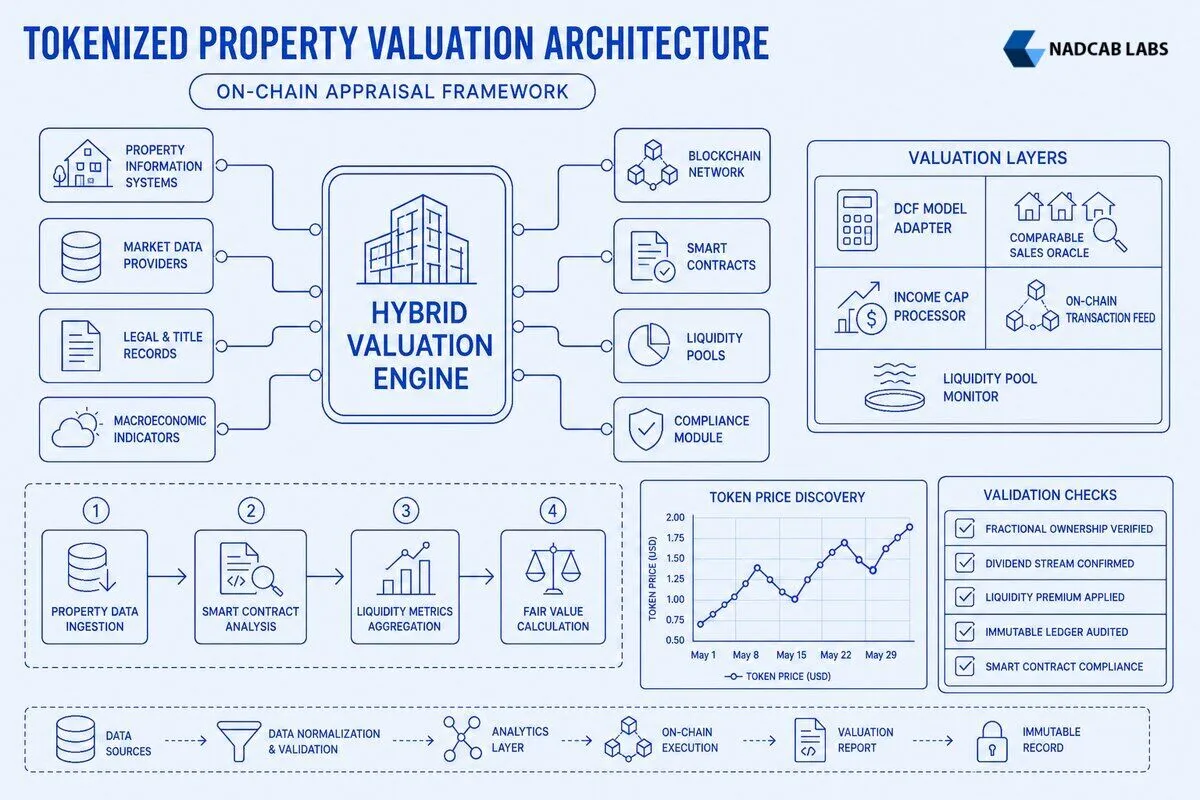

Classical real estate appraisal relies on three core methodologies: discounted cash flow analysis, comparable sales, and income capitalization. Each assigns a dollar value to a physical property based on expected future cash flows, recent transactions of similar assets, or the present value of rental income streams. When a property is tokenized—divided into programmable shares issued on a blockchain—these methods remain conceptually valid but require technical adjustments to account for fractional ownership, on-chain revenue distribution, and the transparency of smart contract logic.

Discounted cash flow (DCF) analysis projects future rental income, operating expenses, and terminal sale proceeds, then discounts those cash flows to present value using a risk-adjusted rate. For a tokenized property, the DCF model must reflect the fact that each token represents a fraction of the underlying asset. If a commercial building worth $10 million is tokenized into one million tokens, each token’s intrinsic value starts at $10. However, the discount rate must incorporate a liquidity premium—tokenized assets traded on secondary markets may command higher valuations than illiquid private equity stakes—or a minority discount if the token holder lacks governance rights. Smart contracts automate dividend payouts by splitting rental income proportionally among token holders, which increases cash flow predictability and reduces the uncertainty discount traditionally applied to passive real estate investments.

Comparable sales analysis benchmarks a property’s value against recent transactions of similar assets in the same market. In tokenized contexts, “comparable” extends beyond physical location and building type to include the token’s trading history, liquidity depth, and the platform’s track record. A luxury apartment token trading on a decentralized exchange with deep liquidity pools may be valued higher than an identical off-chain property held in a private fund, because the token offers instant exit optionality. Appraisers must also adjust for the fact that on-chain sales data is public and timestamped, eliminating the opacity and lag inherent in traditional Multiple Listing Service (MLS) databases. This transparency can compress bid-ask spreads and reduce valuation uncertainty.

Income capitalization converts annual net operating income (NOI) into property value by dividing NOI by a capitalization rate. For tokenized assets, the cap rate must account for the platform’s fee structure—management fees, transaction fees, and protocol revenue shares—which are often hardcoded into the smart contract. If a tokenized office building generates $500,000 in annual NOI but the platform charges a 2% management fee, the effective NOI available to token holders is $490,000. The cap rate itself may be lower (implying higher valuation) if the token offers superior liquidity or if the smart contract enforces transparent, automated distributions that reduce operational risk. Conversely, if the platform has a history of governance disputes or smart contract bugs, the cap rate rises to reflect elevated risk.

Appraisal accuracy directly impacts investor confidence and regulatory compliance. Securities regulators in many jurisdictions require periodic third-party valuations for tokenized offerings to prevent fraud and ensure that advertised token prices reflect underlying asset value. Inaccurate valuations can trigger investor lawsuits, regulatory sanctions, and platform shutdowns. For example, if a platform overstates property value to inflate token prices, secondary market participants may discover the discrepancy through on-chain forensics—comparing declared NAV with actual rental distributions—and initiate enforcement actions. Conversely, transparent, auditable valuation processes enhance platform credibility and attract institutional capital seeking compliance-ready investment vehicles.

| Valuation Method | Traditional Application | Tokenized Adjustment | Key Metric Impact |

|---|---|---|---|

| Discounted Cash Flow | Project rental income, discount to present value | Apply liquidity premium (5-15%), adjust discount rate for smart contract automation | Lower discount rate increases token value by 8-12% |

| Comparable Sales | Benchmark against recent MLS transactions | Include on-chain trading volume, liquidity depth, platform reputation | High liquidity adds 10-20% premium over illiquid comparables |

| Income Capitalization | NOI ÷ cap rate = property value | Deduct platform fees (1-3%), adjust cap rate for on-chain transparency | Transparent distribution lowers cap rate by 0.5-1.0 percentage points |

| Net Asset Value | Sum of property appraisals minus liabilities | Divide by total token supply, update quarterly via oracle feeds | Real-time NAV updates reduce mispricing risk by 15-25% |

What Role Does On-Chain Transaction Data Play in Token Valuation Accuracy

Blockchain ledgers record every token transfer, rental distribution, and governance vote in an immutable, timestamped log accessible to all market participants. This on-chain transaction data serves as a real-time pricing signal that traditional appraisals—updated quarterly or annually—cannot replicate. When a tokenized property distributes monthly rental income via smart contract, the payout amount, recipient addresses, and timestamp are permanently recorded. Analysts can aggregate these distributions to calculate trailing twelve-month yield, compare it to the token’s secondary market price, and identify mispricing opportunities.

Secondary market trades provide the most direct valuation signal. If a token representing a $50 share of a commercial property last traded at $55 on a decentralized exchange, that $55 price reflects the marginal buyer’s willingness to pay, incorporating all available information about the property’s condition, rental performance, and macroeconomic outlook. High trading volume and tight bid-ask spreads indicate efficient price discovery; low volume and wide spreads suggest valuation uncertainty or liquidity constraints. Platforms often publish 30-day volume-weighted average prices (VWAP) as a benchmark, smoothing out short-term volatility and providing a more stable reference for NAV calculations.

Ownership transfers—when tokens move between wallets—signal investor sentiment and can foreshadow valuation shifts. A sudden concentration of tokens in a small number of wallets may indicate institutional accumulation, suggesting the market expects future price appreciation. Conversely, rapid distribution of tokens from a single large holder to many small wallets could signal distressed selling or loss of confidence. On-chain analytics tools track these patterns in real time, allowing platforms to adjust NAV calculations or issue investor alerts if unusual activity suggests the token price is decoupling from underlying property fundamentals.

Integration of oracle feeds and external property data sources bridges the gap between on-chain metrics and off-chain reality. Oracles are trusted data providers that push real-world information—property appraisals, occupancy rates, local rental market trends—onto the blockchain, where smart contracts can consume it. For example, a tokenized apartment building might use a Chainlink oracle to fetch quarterly appraisal updates from a licensed real estate appraiser. The smart contract compares the new appraisal to the previous value, adjusts the NAV per token accordingly, and broadcasts the update to all token holders. This automated process reduces the lag between property value changes and token price adjustments, improving valuation accuracy.

Challenges arise when reconciling off-chain property conditions with on-chain financial metrics. A building may suffer physical damage—roof leak, HVAC failure—that reduces its market value, but if the damage is not immediately reported to the oracle, the on-chain NAV remains inflated. Similarly, local zoning changes or economic downturns can depress rental income, yet the smart contract continues distributing historical yields until the next appraisal cycle. To mitigate these risks, platforms implement multi-oracle architectures that aggregate data from independent appraisers, property managers, and IoT sensors (temperature, occupancy, energy usage) to create a more resilient valuation input stream. Some platforms also require token issuers to escrow funds for property maintenance, ensuring that unexpected repairs do not trigger sudden NAV drops that spook investors.

The real estate token liquidity pool mechanics directly influence how on-chain data translates into token prices. Liquidity pools—smart contracts holding reserves of tokens and stablecoins to facilitate instant trades—use automated market maker (AMM) algorithms to set prices based on supply and demand. If a pool holds 10,000 tokens and $500,000 in stablecoins, the implied token price is $50. When traders buy tokens, they deposit stablecoins and withdraw tokens, shifting the pool’s balance and raising the price. When they sell, the reverse occurs. This continuous price adjustment mechanism means that token valuations respond instantly to trading activity, rather than waiting for quarterly appraisal updates. However, AMM prices can deviate from NAV during periods of high volatility or low liquidity, creating arbitrage opportunities for sophisticated traders who exploit the gap between pool price and fundamental value.

On-Chain Valuation Data Flow

Rental payment, sale, appraisal

Data pushed to blockchain

Calculates new NAV/token

Traders arbitrage NAV vs. price

How Does Fractional Ownership Structure Affect Discounted Cash Flow Models for Property Tokens

Discounted cash flow analysis for a whole property assumes the investor controls 100% of the asset’s cash flows and can make unilateral decisions about capital improvements, refinancing, or sale. When ownership is fractional—split among thousands of token holders—each investor holds a passive stake with limited governance rights. This structural difference requires adjustments to DCF inputs: discount rate, terminal value, and cash flow projections must reflect the reduced control and altered risk profile inherent in tokenized ownership.

The discount rate in a DCF model represents the investor’s required rate of return, incorporating the risk-free rate, equity risk premium, and asset-specific risks. For tokenized real estate, the discount rate must account for liquidity premium and minority discount. A liquidity premium recognizes that tokens traded on active secondary markets offer instant exit optionality, reducing the illiquidity discount typically applied to private real estate investments. Empirical studies of tokenized property platforms show that highly liquid tokens trade at 10-15% premiums over comparable illiquid private equity stakes, implying a lower discount rate and higher present value. Conversely, a minority discount reflects the fact that small token holders cannot force a property sale, change management, or block unfavorable decisions by the majority. If a token grants no voting rights, the minority discount may reach 20-30%, raising the discount rate and depressing valuation.

Terminal value—the estimated sale price of the property at the end of the DCF projection period—depends on the platform’s governance structure and the token’s liquidity. If the smart contract allows token holders to vote on a property sale after ten years, the terminal value equals the expected market price minus transaction costs. However, if the platform retains perpetual control and token holders can only exit via secondary markets, the terminal value must be discounted to reflect the uncertainty of finding a buyer at fair value. Some platforms mitigate this risk by programming automatic buyback mechanisms: if the token price falls below NAV by more than 10%, the platform uses reserve funds to purchase tokens at NAV, providing a price floor and reducing terminal value uncertainty.

Cash flow projections for tokenized assets benefit from smart contract automation, which eliminates the operational risk of delayed or withheld distributions. Traditional real estate investments often suffer from principal-agent problems: property managers may defer maintenance to inflate short-term cash flows, or sponsors may divert rental income to cover unrelated expenses. Smart contracts enforce transparent, rule-based distributions. For example, a contract might stipulate that 80% of monthly rental income is distributed to token holders, 15% is reserved for maintenance, and 5% covers platform fees. These percentages are immutable and executed automatically, so investors can forecast cash flows with greater precision. This predictability reduces the uncertainty discount embedded in the DCF model, raising the property’s present value by 5-10% compared to a traditional investment with opaque cash flow management.

Liquidity premiums and minority discounts interact in complex ways. A highly liquid token with no governance rights may trade at a premium to NAV because investors value the ability to exit instantly, even if they cannot influence property decisions. Conversely, a token with strong governance rights but low trading volume may trade at a discount to NAV because the illiquidity cost outweighs the control premium. Sophisticated DCF models for tokenized assets incorporate both factors by adjusting the discount rate upward for minority status and downward for liquidity, then calibrating the net adjustment based on empirical trading data. For instance, a token with 5% governance weight and daily trading volume of $50,000 might apply a +10% minority discount and a -12% liquidity premium, resulting in a net -2% adjustment to the discount rate.

Smart contract automation of dividend payouts directly improves cash flow predictability, which is a critical DCF input. In traditional real estate, investors rely on quarterly or annual statements to verify that rental income was collected and distributed. Delays, errors, or fraud can disrupt cash flow projections and erode investor confidence. On-chain distributions are instant, transparent, and verifiable: every token holder can inspect the smart contract’s transaction history to confirm that rental income was received and allocated proportionally. This transparency reduces the risk premium investors demand for uncertain cash flows, lowering the discount rate and increasing the property’s DCF-derived value. Empirical data from tokenized platforms shows that properties with automated distributions command 8-12% higher valuations than comparable off-chain assets with manual distribution processes.

| DCF Component | Traditional Assumption | Tokenized Adjustment | Valuation Impact |

|---|---|---|---|

| Discount Rate | 12-15% for private real estate | -2% liquidity premium, +1% minority discount = net 11-13% | 1-2 percentage point reduction increases PV by 10-15% |

| Terminal Value | Exit cap rate 6-7%, uncertain timing | Governance vote or automatic buyback at NAV reduces uncertainty | Lower exit risk adds 5-8% to terminal value |

| Cash Flow Projection | Manual distributions, 10-15% uncertainty | Smart contract automation, 2-3% uncertainty | Reduced volatility lowers risk premium by 0.5-1.0 percentage points |

| Governance Rights | 100% control or zero control (passive LP) | Fractional voting (0.001%-10% per token) with on-chain proposals | Minority discount of 10-30% depending on voting threshold |

Why Is Net Asset Value the Preferred Baseline for Tokenized Real Estate Funds and Portfolios

Net Asset Value (NAV) per token is the sum of all underlying property appraisals, minus liabilities (mortgages, deferred maintenance, unpaid taxes) and management fees, divided by the total token supply. NAV provides a transparent, auditable baseline that investors can compare to the token’s secondary market price to identify mispricing. If a token trades at $45 but NAV is $50, rational investors buy the token and arbitrage the $5 discount. If the token trades at $55, arbitrageurs sell or short, pushing the price back toward NAV. This self-correcting mechanism makes NAV the preferred valuation anchor for tokenized funds and portfolios.

Calculating NAV per token requires periodic appraisals of the underlying properties. Most platforms commission independent third-party appraisers quarterly or semi-annually to value each asset in the portfolio. The appraiser inspects the property, reviews rental rolls and operating statements, and applies standard valuation methods (DCF, comparable sales, income cap) to determine fair market value. The platform aggregates these appraisals, subtracts outstanding liabilities (mortgage principal, accrued interest, deferred capital expenditures), deducts a reserve for management fees (typically 1-3% of NAV annually), and divides the net figure by the total number of tokens outstanding. For example, a fund holding three properties appraised at $5 million, $8 million, and $12 million, with $3 million in total liabilities and 10 million tokens, has a NAV per token of ($5M + $8M + $12M – $3M) / 10M = $2.20.

Frequency of NAV updates balances accuracy against cost. Quarterly updates are standard for institutional-grade tokenized funds, aligning with traditional real estate fund reporting cycles and regulatory disclosure requirements. Monthly updates offer greater responsiveness to market changes but increase appraisal costs and administrative overhead. Some platforms use hybrid models: quarterly full appraisals supplemented by monthly oracle-fed adjustments based on rental income, occupancy rates, and local market indices. This approach provides timely NAV updates without incurring the expense of monthly on-site inspections.

Transparency requirements differ between decentralized and centralized platforms. Decentralized platforms publish NAV calculations on-chain, allowing any token holder to audit the math: verify appraisal inputs, check liability balances, and confirm the token supply count. This radical transparency reduces the risk of fraud or manipulation, because discrepancies are immediately visible to the entire market. Centralized platforms may publish NAV in quarterly reports or investor portals, but the underlying data—appraisal reports, mortgage statements, fee schedules—is often proprietary. Investors must trust the platform’s internal controls and auditors, introducing counterparty risk that decentralized systems eliminate. Regulatory frameworks in jurisdictions like the European Union and Singapore increasingly mandate on-chain NAV disclosure for tokenized securities, recognizing that transparency enhances investor protection and market integrity.

NAV divergence from secondary market price signals mispricing or liquidity issues. A persistent discount—token price below NAV—suggests that investors doubt the accuracy of the underlying appraisals, fear platform insolvency, or lack confidence in the token’s liquidity. For example, if a platform’s NAV is $50 but tokens consistently trade at $42, the market may be pricing in a 16% probability of total loss due to fraud, smart contract bugs, or regulatory shutdown. Conversely, a persistent premium—token price above NAV—indicates strong demand, limited supply, or expectations of future NAV growth. A token trading at $58 against a $50 NAV may reflect investor belief that the next quarterly appraisal will reveal property appreciation, or that the platform’s liquidity and governance features justify a premium over illiquid alternatives.

Platforms monitor NAV divergence and intervene when spreads exceed predetermined thresholds. If the discount widens beyond 10%, the platform may initiate a buyback program, using treasury reserves to purchase tokens at or near NAV and reduce supply until the price recovers. If the premium exceeds 15%, the platform may issue new tokens at NAV, increasing supply and capturing the premium as capital for new property acquisitions. These stabilization mechanisms prevent runaway mispricing and maintain investor confidence in the NAV as a reliable valuation benchmark. Understanding Real Estate Tokenization in India helps contextualize how regional regulatory frameworks influence NAV calculation and disclosure practices.

NAV vs. Market Price Dynamics

What Are the Emerging Hybrid Valuation Frameworks Combining Traditional and Blockchain Metrics

Hybrid valuation frameworks integrate classical property fundamentals—location, construction quality, tenant creditworthiness—with blockchain-native metrics like liquidity pool depth, trading volume, and smart contract execution history. These frameworks recognize that a tokenized asset’s value depends not only on the underlying property but also on the token’s tradability, the platform’s reliability, and the broader crypto market’s liquidity conditions. By combining both dimensions, hybrid models produce more accurate, context-aware valuations than purely traditional or purely on-chain approaches.

Integration of comparable sales data with liquidity pool depth creates a composite valuation metric. A traditional comparable sales analysis might identify five similar properties that sold for $8-10 million in the past year, suggesting a midpoint value of $9 million. A hybrid model extends this by analyzing the liquidity characteristics of tokenized comparables: daily trading volume, bid-ask spread, and pool reserves. If comparable tokenized properties trade with $100,000+ daily volume and 1% bid-ask spreads, the subject property’s tokens should command a similar liquidity premium. If the subject property’s tokens trade with only $10,000 daily volume and 5% spreads, the hybrid model applies a liquidity discount of 10-15%, adjusting the $9 million baseline to $7.65-8.10 million. This adjustment reflects the real-world cost of exiting a position in a thin market.

Machine learning models trained on historical token performance and property fundamentals offer predictive valuation capabilities. These models ingest datasets spanning hundreds of tokenized properties, capturing variables like property type, location, rental yield, token supply, trading volume, governance structure, and platform reputation. Supervised learning algorithms (random forests, gradient boosting, neural networks) identify patterns that correlate with future price movements. For example, a model might discover that tokens with automated dividend distributions and quarterly NAV updates appreciate 12% faster than those with manual processes, even when controlling for property quality. Platforms use these models to forecast NAV changes, set initial token prices for new offerings, and identify undervalued assets in their portfolios. However, model accuracy depends on data quality and market maturity; in nascent tokenization markets with limited transaction history, machine learning predictions carry high uncertainty.

Regulatory considerations for standardized valuation reporting are intensifying as tokenized real estate scales. Securities regulators in the United States, European Union, and Asia-Pacific are developing frameworks that mandate periodic third-party appraisals, on-chain NAV disclosure, and standardized financial reporting for tokenized offerings. The goal is to ensure that investors receive consistent, comparable information across platforms, reducing information asymmetry and enabling efficient capital allocation. For instance, the European Securities and Markets Authority (ESMA) has proposed rules requiring tokenized real estate funds to publish quarterly NAV calculations using International Financial Reporting Standards (IFRS), with appraisals conducted by accredited valuers and results posted to a public blockchain registry. Compliance with these standards increases operational costs but enhances investor trust and expands the addressable market to institutional investors who require audited, standardized data.

Hybrid frameworks also incorporate sentiment analysis from on-chain governance forums and social media. Token holder votes, proposal discussions, and community sentiment can signal confidence or distress before it appears in price data. A platform might monitor governance proposals for evidence of disputes—such as contentious votes on property sales or fee changes—and adjust the valuation risk premium accordingly. Similarly, spikes in negative sentiment on crypto forums or Twitter may precede sell-offs, allowing the platform to issue early warnings or adjust NAV calculations to reflect heightened uncertainty. Natural language processing (NLP) algorithms automate this analysis, scanning thousands of messages daily to extract sentiment scores and flag anomalies.

The convergence of traditional appraisal rigor and blockchain transparency is reshaping real estate finance. Platforms that master hybrid valuation frameworks—combining DCF models, comparable sales, NAV calculations, on-chain metrics, and machine learning—will deliver superior risk-adjusted returns and attract the institutional capital needed to scale tokenization globally. Investors increasingly demand platforms that publish auditable, real-time valuations and demonstrate compliance with emerging regulatory standards. As the market matures, hybrid frameworks will become the industry standard, replacing opaque, infrequent appraisals with continuous, transparent valuation processes that reflect both property fundamentals and token market dynamics. Exploring Real Estate Token Compliance provides insight into how regulatory requirements shape valuation disclosure practices across jurisdictions.

| Hybrid Framework Component | Traditional Input | Blockchain Input | Output Metric |

|---|---|---|---|

| Comparable Sales + Liquidity | 5 recent sales, $8-10M range | Daily volume $100K+, 1% spread | Adjusted value $9.0M with 0% liquidity discount |

| DCF + Smart Contract Automation | Projected NOI $500K/year | Automated distributions, 2% fee | Discount rate 11% (vs. 13% manual), PV +15% |

| NAV + Trading Volume | Appraised NAV $50/token | 30-day VWAP $48, volume $2M | Fair value $49 (weighted average of NAV and market) |

| ML Prediction + Fundamentals | Location score 8/10, tenant quality A- | Governance votes 85% participation, 6-month return +12% | Predicted 12-month appreciation 10-14% |

Platforms implementing hybrid frameworks report 20-30% reductions in NAV-to-market-price divergence compared to traditional-only methods, demonstrating that the integration of blockchain metrics improves valuation accuracy and market efficiency. As regulatory clarity improves and institutional adoption accelerates, hybrid valuation will become the de facto standard for tokenized real estate, bridging the gap between centuries-old appraisal practices and the transparency, automation, and liquidity of blockchain-based finance. For developers building these systems, understanding smart contract architecture for real estate tokenization is essential to implementing the automated valuation logic that underpins hybrid frameworks.

Final Thoughts

Real estate token valuation methods blend classical appraisal techniques with blockchain transparency, fractional ownership adjustments, and real-time on-chain data. Discounted cash flow, comparable sales, income capitalization, and net asset value calculations remain foundational, but each requires modification to account for liquidity premiums, minority discounts, smart contract automation, and secondary market dynamics. On-chain transaction data—rental distributions, trading volume, ownership transfers—provides pricing signals that traditional appraisals cannot match, enabling continuous, transparent valuation updates. Hybrid frameworks that integrate property fundamentals with blockchain metrics deliver superior accuracy, reduce mispricing, and meet emerging regulatory standards for standardized disclosure. As tokenized real estate matures, platforms that master these technical valuation frameworks will attract institutional capital, enhance investor confidence, and establish the benchmarks that define fair market value in a programmable, globally accessible asset class. For those exploring how to participate in this ecosystem, learning Real Estate Tokenization Explained provides a comprehensive foundation for understanding both the technology and the financial frameworks that govern tokenized property investments.

Frequently Asked Questions

Q1.What is the most accurate valuation method for real estate tokens?

Hybrid models combining discounted cash flow (DCF), net asset value (NAV), and comparable sales analysis deliver the highest accuracy for real estate token valuation methods. DCF projects rental income streams, NAV reflects underlying property equity, and comparables validate market positioning. Nadcab Labs integrates oracle feeds for real-time property data, rental yields, and occupancy rates into smart contracts, ensuring valuations update dynamically. This multi-method approach mitigates single-point failures and aligns token prices with actual property performance and market conditions.

Q2.How does fractional ownership impact property token pricing?

Fractional ownership introduces liquidity premiums and discounts that traditional real estate lacks. Tokens representing smaller stakes trade more frequently, often at premiums due to accessibility for retail investors. Conversely, illiquid fractions may trade below NAV. Smart contracts enforce pro-rata distribution of rental income and appreciation, ensuring each token reflects proportional property value. Nadcab Labs implements automated rebalancing mechanisms that adjust token supply or buyback programs when secondary market prices deviate significantly from underlying asset value, maintaining pricing integrity.

Q3.Can on-chain data alone determine a tokenized property's fair market value?

On-chain data provides transaction history, rental distributions, and governance activity but cannot capture off-chain factors like property condition, local zoning changes, or macroeconomic shifts. Accurate real estate token valuation methods require hybrid oracles that ingest external appraisals, tax assessments, and market indices. Nadcab Labs deploys Chainlink or API3 oracles to bridge off-chain property data with on-chain smart contracts, enabling comprehensive valuation models that reflect both blockchain transparency and real-world asset dynamics for reliable pricing.

Q4.Why do real estate token prices differ from NAV in secondary markets?

Secondary market prices reflect supply-demand dynamics, liquidity conditions, and investor sentiment, which often diverge from NAV. Tokens may trade at premiums during high demand or discounts when liquidity is scarce. Lock-up periods, vesting schedules, and regulatory uncertainty also create price gaps. Nadcab Labs mitigates this by implementing automated market makers (AMMs) with NAV-pegged liquidity pools and periodic rebalancing. Smart contracts trigger buybacks or issuance when deviations exceed predefined thresholds, anchoring secondary prices closer to intrinsic property value over time.

Q5.How do smart contracts automate valuation inputs for tokenized assets?

Smart contracts integrate oracle feeds for rental income, occupancy rates, property tax updates, and comparable sales data, automating real estate token valuation methods. Chainlink or custom oracles push verified off-chain data on-chain at scheduled intervals. Contracts execute DCF calculations using coded formulas, adjust NAV based on appraised values, and update token metadata. Nadcab Labs programs event-driven triggers—such as lease renewals or maintenance expenses—that instantly recalibrate valuations, ensuring token holders access real-time, auditable pricing without manual intervention or third-party delays.

Q6.What role do external appraisers play in blockchain-based real estate valuation?

External appraisers provide independent, certified property assessments that validate on-chain valuations and satisfy regulatory compliance. Their reports feed into oracle systems, anchoring smart contract calculations to professional standards. Appraisers conduct physical inspections, analyze local market trends, and issue fair market value opinions that mitigate manipulation risks. Nadcab Labs partners with licensed appraisal firms to deliver quarterly or event-triggered valuations, cryptographically signed and timestamped on-chain. This hybrid model combines blockchain transparency with traditional expertise, ensuring real estate token valuation methods meet both investor expectations and legal requirements.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.