Ai Overview

Real estate tokenization in India refers to the process of converting ownership rights in physical property assets into blockchain-based digital tokens that can be issued, transferred, and traded by investors. The VDA framework imposes a 30% flat tax on income from transfer of VDAs with no deduction permitted except the cost of acquisition, and a 1% TDS on transfers exceeding prescribed thresholds.

Key Takeaways

Real estate tokenization in India operates across SEBI, RBI, RERA, and IFSCA jurisdictions, requiring simultaneous multi-regulator compliance for lawful issuance and trading.

SEBI classifies real estate tokens offering returns as securities, triggering the full suite of disclosure, registration, and investor protection obligations under Indian securities law.

GIFT City’s IFSCA framework currently provides India’s clearest regulatory pathway for tokenization platforms serving both domestic and international investors including NRIs.

NRI investors must comply with FEMA investment limits and RBI repatriation rules when accessing tokenized Indian real estate through any platform or structure.

The 30% VDA tax regime introduced in the 2022 Budget continues to apply to real estate token transactions, alongside capital gains, TDS, and GST obligations in 2026.

Smart contract audits from CERT-In empanelled agencies are increasingly expected by SEBI as a condition for platform authorization and token offering approval processes.

India’s SEBI framework for real estate tokens is converging toward principles already established by the SEC in the USA, FCA in the UK, and DFSA in Dubai across key compliance dimensions.

Platform licensing for a SEBI-compliant tokenization marketplace requires registrations spanning stock broker, investment adviser, and potentially alternative investment fund categories.

Investor due diligence for Indian real estate tokens must cover RERA registration, token offering documents, smart contract audits, platform licensing, and clear exit mechanisms.

Secondary market liquidity for Indian real estate tokens remains limited in 2026, making lock-in periods and exit provisions among the most critical factors for investor evaluation.

India’s property market, valued at over $330 billion and growing rapidly across Mumbai, Bengaluru, Delhi NCR, and Hyderabad, is standing at the threshold of a profound structural transformation. Real estate tokenization is no longer a concept discussed only at blockchain conferences; it is actively being evaluated, piloted, and partially implemented by platforms operating under India’s emerging regulatory architecture. With SEBI, RBI, RERA, and IFSCA all holding jurisdictional stakes in how tokenized property instruments are issued, traded, and governed, the compliance landscape in 2026 is both complex and rapidly clarifying.

Having guided tokenization projects across the USA, UK, UAE, Canada, and India for over eight years, our advisory practice brings a ground-level perspective to what SEBI’s evolving stance means for issuers, platforms, and investors. This comprehensive guide is designed to serve every stakeholder: from the Mumbai-based developer seeking to fractionalize a commercial tower, to the NRI investor in Dubai looking to access Indian real estate yield through compliant token instruments.

What is Real Estate Tokenization in India and Why India Is at a Critical Regulatory Inflection Point in 2026

Real estate tokenization in India refers to the process of converting ownership rights in physical property assets into blockchain-based digital tokens that can be issued, transferred, and traded by investors. Each token represents a proportional economic interest in an underlying real estate asset, whether a residential apartment complex in Pune, a commercial office park in Bengaluru, or a hospitality asset in Goa. The technology enables fractional ownership at unprecedented scale, allowing investors to participate in property markets previously accessible only to institutional players or high-net-worth individuals with large capital reserves.

India reaches a critical inflection point in 2026 because multiple converging forces are reshaping the regulatory landscape simultaneously. SEBI has been consulting on a broader securities market framework for digital assets. IFSCA at GIFT City has issued fintech sandbox guidelines that explicitly accommodate tokenization. The Income Tax Department has clarified VDA taxation. And RBI has moved from broad cryptocurrency caution toward differentiated treatment of asset-backed digital instruments. This multi-regulator evolution creates both opportunity and complexity for every stakeholder in the ecosystem.

SEBI’s Evolving Stance on Virtual Digital Assets: From Caution to Structured Oversight

SEBI’s journey with digital assets has been marked by methodical caution followed by increasingly structured engagement. In its early communications between 2018 and 2021, SEBI largely deferred to RBI on cryptocurrency matters while maintaining a watching brief on tokenized securities developments globally. The landmark SEBI consultation papers of 2022 and 2023 signaled a fundamental shift: the regulator began distinguishing between pure cryptocurrencies and asset-backed security tokens, recognizing that the latter share fundamental characteristics with traditional securities instruments already under its jurisdiction.

By 2024 and into 2025, SEBI’s annual reports and working group findings explicitly referenced tokenized securities as a category requiring tailored regulatory treatment. The regulator directed its research division to benchmark India’s approach against frameworks in the USA (SEC), UK (FCA), UAE (DFSA and ADGM), Canada (CSA), and Singapore (MAS). This comparative analysis informed internal draft guidelines that, while not yet fully codified as of early 2026, have established clear directional principles that market participants are expected to follow.

SEBI’s current posture in 2026 can be characterized as permissive-with-structure: it does not prohibit real estate tokenization in India, but it expects any platform or issuer operating in this space to comply with applicable securities laws, maintain full transparency, protect retail investor interests, and engage proactively with regulators rather than attempting to exploit definitional ambiguities in the law.

How SEBI Classifies Real Estate Tokens: Security Token vs Utility Token vs Hybrid Instrument

Token classification is the foundational regulatory question for any real estate tokenization in India project, and SEBI’s approach draws heavily from the Howey Test principles applied by the SEC in the USA while incorporating Indian securities law definitions. The classification determines which regulatory regime applies, what disclosures are mandatory, and what investor protections must be built into the offering structure.

Security Token

Represents ownership, profit sharing, rental income rights, or investment returns tied to a real estate asset. SEBI treats these as securities under SCRA, requiring registration and full prospectus-level disclosure to all investors.

Provides access to platform services, property amenities, or governance rights without direct financial return expectations. Lower regulatory burden but SEBI scrutinizes utility claims carefully to prevent misclassification as a compliance avoidance tactic.

Hybrid Instrument

Combines utility features with economic return characteristics. SEBI applies a substance-over-form analysis: if the dominant purpose is investment return, the token is classified as a security regardless of the utility wrapper applied around it.

The Legal Architecture Behind a SEBI-Compliant Real Estate Token Offering in India

Building a legally sound real estate token offering in India requires constructing a multi-layered legal architecture that satisfies SEBI requirements while integrating seamlessly with property law, contract law, and company law frameworks. The typical compliant structure involves a Special Purpose Vehicle (SPV) registered under the Companies Act 2013, which holds the legal title to the underlying real estate asset. The SPV issues securities representing economic interests, which are then tokenized on a blockchain and offered to investors through a licensed platform or intermediary.

The SPV structure is preferred because it creates a clean separation between the tokenization platform and the underlying asset, providing investor protection in the event of platform insolvency. Title documents, lease agreements, and property revenue arrangements are held within the SPV, while the token represents a beneficial or economic interest in the SPV’s assets. This mirrors structures used successfully in the UK and UAE for property-backed securities and provides a precedent SEBI can reference in its oversight.

The offering documents, analogous to a prospectus for traditional securities, must disclose the property’s RERA registration details, financial projections, risk factors, token rights, redemption mechanisms, and governance structure. Legal opinions confirming the securities classification of the token and the validity of the SPV structure are increasingly considered mandatory by legal counsel experienced in this space across India and internationally.

RERA, FEMA and RBI Alignment: How Real Estate Tokenization in India Sits Across Three Regulatory Frameworks

Real estate tokenization in India is uniquely complex because it sits at the intersection of three distinct regulatory domains: RERA governs the underlying real estate asset and its developer obligations; FEMA and RBI govern cross-border capital flows, foreign investment, and currency regulations; and SEBI governs the securities aspects of token issuance and trading. A platform or issuer that satisfies SEBI requirements but ignores RERA compliance or violates FEMA capital account restrictions faces significant legal exposure regardless of its token structure.

RERA compliance means the underlying property must be registered with the relevant state RERA authority, all disclosures mandated by the Real Estate (Regulation and Development) Act must be current, and the developer must have fulfilled statutory obligations to purchasers and regulatory bodies. Tokenizing a RERA non-compliant property creates fundamental legal defects in the token offering that no blockchain architecture can remedy.

FEMA implications become critical when foreign investors, including NRIs from the USA, UK, UAE, and Canada, participate in token offerings for Indian real estate. Under Schedule I and Schedule IV of FEMA, foreign investment in Indian real estate (other than permitted categories) carries restrictions. Platforms must structure their SPVs and token instruments to fit within FDI-permitted categories or obtain RBI approvals where required, making FEMA counsel an essential component of any compliant token offering architecture.

Platform Licensing Requirements Under SEBI: What a Tokenization Marketplace Must Obtain Before Launch

Launching a Real Estate Tokenization in India that operates as a marketplace for issuing and trading tokens requires navigating a layered licensing matrix under SEBI’s existing frameworks, given that a specific tokenization marketplace license does not yet exist as a standalone category. Platforms must map their activities to existing regulatory categories and obtain the appropriate registrations before conducting any investor-facing operations.

Based on the platform’s functional scope, required registrations typically include one or more of the following categories.

Stock Broker or Sub-Broker Registration

Required if the platform facilitates secondary market trading of security tokens. Registration with a recognized stock exchange is required, along with adherence to SEBI’s broker conduct regulations and net worth requirements applicable to intermediaries.

Investment Adviser Registration

If the platform provides investment recommendations or portfolio guidance on token selection, SEBI’s Investment Adviser regulations under the Securities and Exchange Board of India (Investment Advisers) Regulations 2013 apply, requiring qualified personnel and fiduciary compliance.

Alternative Investment Fund (AIF) Registration

For pooled token offerings structured as collective investment vehicles, Category II AIF registration under SEBI’s AIF Regulations 2012 is applicable. This path offers a more structured framework with defined investor eligibility, minimum corpus, and reporting requirements.

IFSCA Fintech Entity Registration at GIFT City

For platforms targeting international investors or structuring cross-border token offerings, registration as a Fintech Entity under IFSCA’s regulatory framework provides access to GIFT City’s international financial services environment with distinct rules from mainland India.

KYC, AML and Investor Accreditation Standards for Indian Real Estate Token Platforms in 2026

Know Your Customer and Anti-Money Laundering compliance is non-negotiable for any Real Estate Tokenization in India platform operating in India, regardless of whether it is licensed under SEBI, IFSCA, or both. The Prevention of Money Laundering Act 2002 (PMLA) designates securities market intermediaries as reporting entities with mandatory obligations to maintain investor identification records, conduct transaction monitoring, report suspicious transactions to the Financial Intelligence Unit, and retain documentation for a minimum of five years.

For real estate tokenization in India platforms, KYC must follow SEBI’s master circular guidelines, which require identity verification using officially valid documents (OVDs), PAN verification for all Indian investors, Aadhaar-based eKYC where permissible, and enhanced due diligence for politically exposed persons (PEPs) and high-risk geographies. NRI investors from the USA, UK, UAE, and Canada require additional documentation including foreign address proof, NRE or NRO account details, and FEMA declaration forms.

Investor accreditation standards are particularly relevant for token offerings structured as private placements. SEBI’s framework distinguishes between qualified institutional buyers (QIBs), non-institutional investors, and retail investors, with different disclosure and suitability requirements for each category. Platforms targeting retail participation must apply stricter suitability assessments and provide simplified risk disclosures in languages accessible to their target audience across India’s diverse investor base.

Smart Contract Audit and Technical Compliance Standards Expected by SEBI for Token Issuance

The technical dimension of regulatory compliance for real estate tokenization in India has become increasingly rigorous, with SEBI and IFSCA both signaling that smart contract quality and security are material considerations in platform authorization. A defective or exploitable smart contract governing token issuance, distribution, and transfer can compromise investor funds and expose the platform to both regulatory sanction and civil liability, making independent technical audits an operational necessity rather than an optional enhancement.

Tax Treatment of Real Estate Tokens in India 2026: Capital Gains, TDS, GST and Income Reporting

The tax landscape for real estate tokenization in India in 2026 involves multiple intersecting provisions of the Income Tax Act, GST legislation, and the specific Virtual Digital Asset (VDA) tax framework introduced in the Finance Act 2022. Understanding the applicable tax treatment is critical for investors evaluating post-tax returns, and for platforms designing compliant income distribution and reporting systems. The VDA framework imposes a 30% flat tax on income from transfer of VDAs with no deduction permitted except the cost of acquisition, and a 1% TDS on transfers exceeding prescribed thresholds.

The classification of a real estate token as a VDA versus a traditional security determines which tax regime applies. If SEBI classifies the token as a security, capital gains provisions under Section 45 and 112A of the Income Tax Act apply, with long-term capital gains (for holdings over 36 months) taxed at 20% with indexation or 10% without. Short-term gains are taxed at the applicable income slab rate. Rental income distributions from the underlying property received by token holders are taxed as income from other sources unless structured as debenture interest.

GST implications arise at the platform services level. Platform fees charged for token issuance, trading, or management services attract 18% GST under the services category. And platforms must ensure proper compliance with the applicable gst filing procedure while reporting such service transactions. The underlying real estate transaction itself may carry GST obligations depending on whether the property is under construction or completed. NRI investors from the USA, UK, UAE, and Canada must also consider double taxation avoidance agreement (DTAA) provisions with India when computing their effective tax obligations on Indian real estate token income. [1]

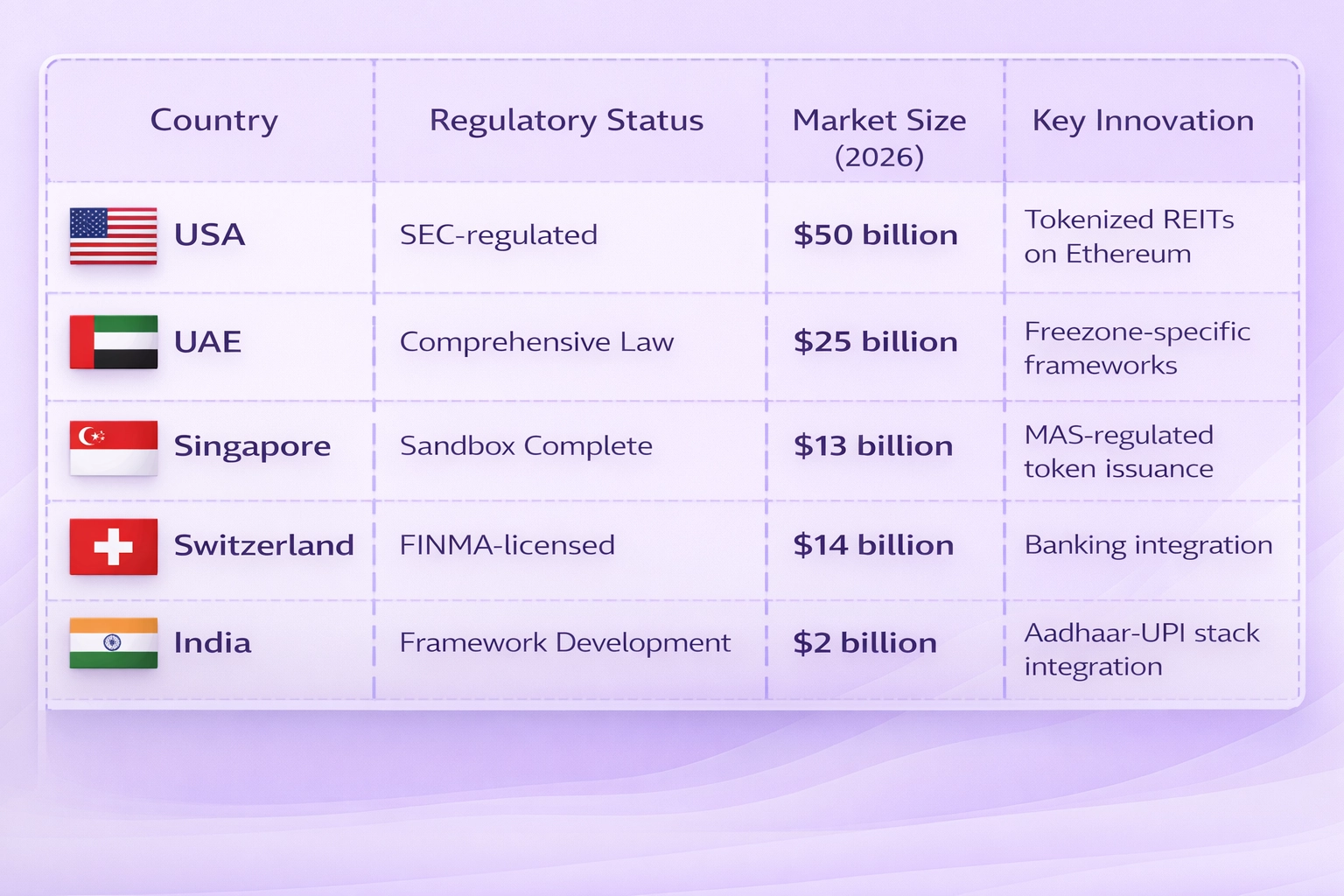

Adoption Metrics Across Jurisdictions and India’s Competitive Advantage

Among all emerging markets pursuing real estate tokenization, India holds a structurally unique position that no other jurisdiction can replicate. The convergence of digital public infrastructure, unmatched investor scale, cost-efficient talent, and a common law judicial framework positions India to become the world’s largest Real Estate Tokenization in India market by transaction volume before 2030.

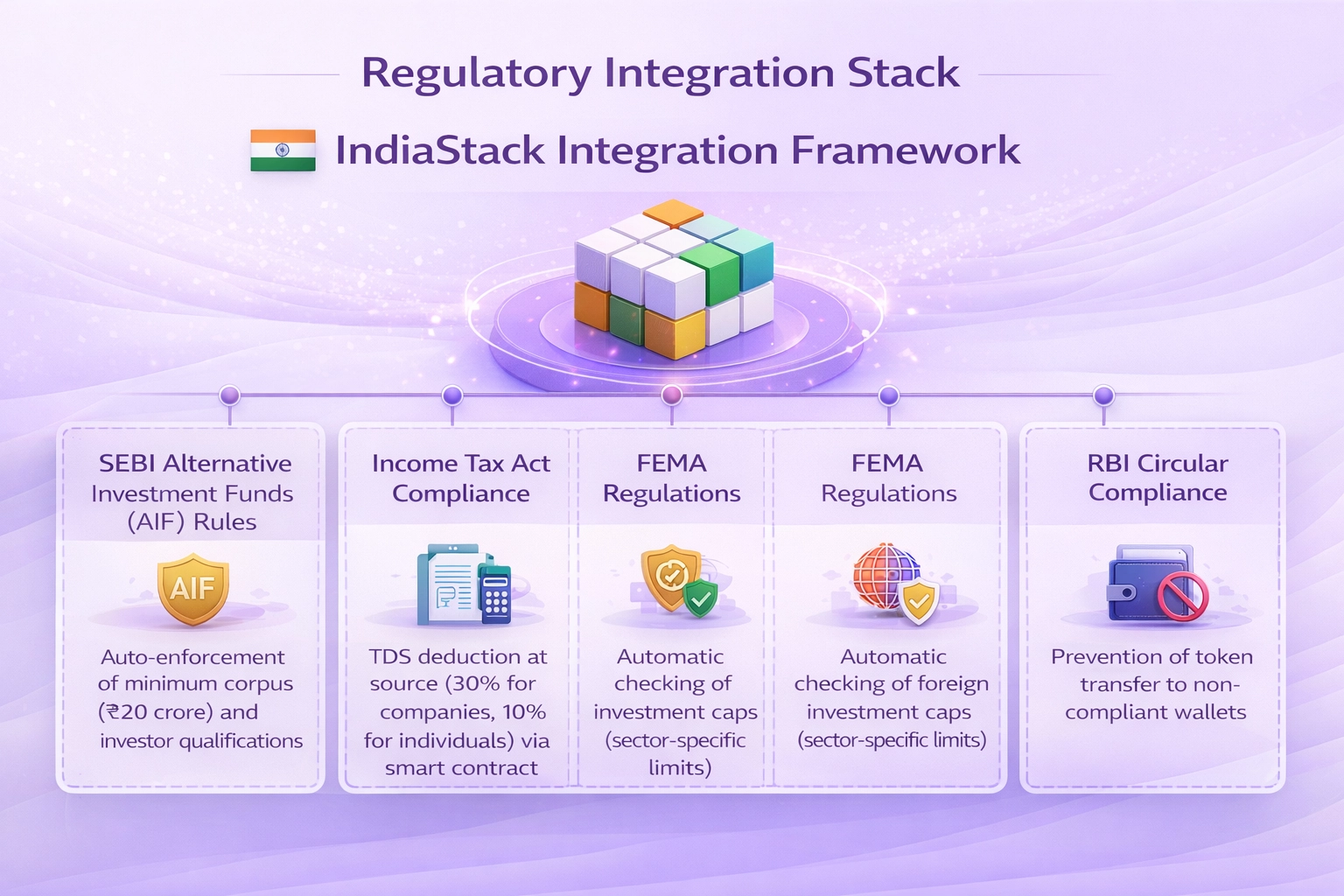

Regulatory Integration Stack for Tokenized Real Estate in India

Technical Implementation Roadmap for Real Estate Tokenization in India 2026 to 2030

Real Estate Tokenization in India infrastructure is being constructed in three deliberate phases, each building on the regulatory, technical, and market foundations of the prior period. This roadmap reflects the convergence of SEBI oversight, RBI digital currency initiatives, and IFSCA international frameworks into a unified national tokenization ecosystem.

GIFT City and IFSCA as Real Estate Tokenization in India Sandbox: Current Status and Investor Access

Gujarat International Finance Tec-City, known globally as GIFT City, has emerged as the most advanced regulatory environment for real estate tokenization in India in 2026. The International Financial Services Centres Authority (IFSCA), which governs all financial activities within GIFT City’s International Financial Services Centre (IFSC), has established a Fintech Regulatory Sandbox that explicitly accommodates tokenized asset experiments, making it the preferred launchpad for platforms seeking structured regulatory clarity before potential national scale-up.

IFSCA’s framework is designed to attract international capital by offering a regulatory environment comparable to leading global financial centers. For Real Estate Tokenization in India specifically, IFSCA has issued draft frameworks covering tokenized securities, digital custody, and cross-border fund management that provide actionable compliance pathways. Platforms registered under IFSCA can offer tokens to investors globally, including high-net-worth individuals and institutional investors from the USA, UK, UAE, and Canada, subject to each investor’s home country regulations.

For domestic Indian investors, access to GIFT City-based token offerings is currently structured through mechanisms that maintain compliance with both IFSCA rules and RBI’s liberalized remittance scheme (LRS) or FEMA framework. Resident Indians investing through GIFT City structures must count such investments within their LRS annual limit of $250,000. This creates a practical constraint for high-volume retail participation but leaves significant room for HNI and institutional investors to access GIFT City-listed real estate tokens representing premium Indian and international assets.

NRI Real Estate Tokenization in India Under SEBI and FEMA: Investment Limits, Repatriation Rules and Permitted Asset Classes

The NRI investor segment represents one of the most strategically important target markets for real estate tokenization in India, given that the Indian diaspora across the USA, UK, UAE, and Canada represents over 30 million individuals with strong cultural and economic ties to Indian property markets. NRIs have historically faced practical barriers to participating in Indian real estate beyond direct property purchase: complex paperwork, high transaction costs, management challenges, and illiquidity. Tokenization, if properly structured, addresses each of these friction points simultaneously.

Under FEMA, NRIs can invest in Indian real estate through NRE (Non-Resident External) or NRO (Non-Resident Ordinary) accounts, with distinct repatriation rules for each. Investments through NRE accounts are fully repatriable, meaning income and principal can be remitted abroad without limit. NRO account investments carry more restrictive repatriation rules, capped at $1 million per financial year including sale proceeds. Tokenization platforms onboarding NRI investors must build account type verification and repatriation eligibility checking into their KYC and distribution workflows.

Permitted asset classes for NRI investment in tokenized form generally align with asset classes where direct NRI investment is already permitted under FEMA’s Schedule IV: completed residential properties, commercial real estate, and certain industrial properties. Tokenized investments in agricultural land, plantation property, or farmhouses remain restricted for NRIs as they are for direct ownership, and no tokenization structure can legally circumvent this FEMA restriction regardless of its technical architecture.

Real-World Examples: Real Estate Tokenization in India Platforms Operating in 2025-2026 and Their Compliance Approach

Real Estate Tokenization in India ecosystem has produced a number of pioneering platforms that are actively navigating the regulatory environment in 2025-2026, providing valuable case studies in compliance approach and market strategy. These platforms have taken materially different approaches to regulatory positioning, reflecting the genuine ambiguity that still exists within India’s evolving framework for tokenized assets.

GIFT City-First Platform Model

Several platforms have chosen to establish their primary entity within GIFT City under IFSCA oversight, offering tokens to both NRI and international investors while maintaining a separate domestic entity for Indian resident operations. This bifurcated structure allows the platform to benefit from IFSCA’s more developed tokenization framework while planning for eventual SEBI national framework alignment.

AIF-Wrapped Tokenization Model

Other platforms have structured their offerings as Category II Alternative Investment Funds with blockchain-based unit tracking, effectively using tokenization as a record-keeping and transfer mechanism within an already-regulated AIF structure. This approach provides the clearest immediate legal standing under SEBI’s existing framework while awaiting specific tokenization regulations.

Private Placement to Accredited Investors

A number of early-stage platforms have limited their token offerings to accredited and qualified institutional investors under private placement exemptions, avoiding the full public offer registration requirements while building a compliance track record that positions them for broader retail offerings once the regulatory framework firms up in late 2026 or 2027.

Investor Protection Mechanisms Under SEBI’s Framework: Grievance Redressal, Audit Rights and Dispute Resolution

SEBI’s fundamental mandate is investor protection, and this obligation extends fully to investors participating in real estate tokenization in India. Any platform operating under SEBI’s framework must implement robust investor protection mechanisms as a condition of authorization, not as an optional addition. The architecture of these protections mirrors requirements applied to traditional securities intermediaries while incorporating specific adaptations for the digital nature of token-based investments.

The SEBI SCORES platform (Securities and Exchange Board of India Complaints Redress System) serves as the primary formal grievance mechanism for investors in SEBI-regulated entities. Token platforms must register on SCORES, maintain a dedicated investor grievance officer, and resolve all complaints within SEBI’s mandated timelines. Failure to resolve complaints through the platform escalates to SEBI’s direct intervention, potentially triggering formal investigations and licensing consequences for non-compliant platforms.

Audit rights represent another critical investor protection element. Token holders in properly structured offerings should have contractual rights to inspect the SPV’s financial statements, property management accounts, and occupancy data on a periodic basis. These audit rights are typically codified in the token’s underlying trust deed or subscription agreement and enforced through the SPV’s governance structure. Dispute resolution provisions should specify mandatory arbitration under the Arbitration and Conciliation Act 1996, with seat of arbitration in a major Indian city and SEBI’s power of intervention preserved for systemic regulatory breaches.

How India Compares Globally: SEBI Framework vs SEC, FCA, DFSA and MAS Regulatory Approaches to Real Estate Tokenization in India

Understanding how India’s regulatory approach to Real Estate Tokenization in India compares with leading global frameworks helps issuers, platforms, and investors calibrate expectations and structure cross-border offerings effectively. Our eight-plus years of experience working across these jurisdictions reveals both meaningful convergence and important divergences in approach.

| Dimension | India (SEBI/IFSCA) | USA (SEC) | UK (FCA) | UAE (DFSA) |

|---|---|---|---|---|

| Token Classification | Evolving; SCRA-based for securities tokens | Howey Test; Reg D / Reg A+ paths | FCA Perimeter Guidance; Specified Investment | DFSA Investment Token regime |

| Sandbox Availability | IFSCA Fintech Sandbox active | Limited federal sandbox; state-level options | FCA Regulatory Sandbox active | DFSA Innovation Testing License |

| Retail Investor Access | Limited; accredited investor preference | Reg CF allows retail participation | Restricted; FCA promotion rules apply | Professional investors primarily |

| Secondary Market | Nascent; no dedicated exchange | tZERO and regulated ATS platforms | FCA-authorized trading venues | DIFC-based exchange infrastructure |

| Tax Clarity | VDA 30% rate; classification-dependent | IRS guidance; property tax rules apply | HMRC guidance; CGT applicable | Zero income/capital gains tax in DIFC |

6-Step Model Selection Criteria for Real Estate Tokenization in India

Define the Asset Category and FEMA Eligibility

Before selecting a tokenization model, confirm whether the underlying asset qualifies for foreign investment under FEMA. Only FEMA-permitted asset classes can support NRI or foreign investor participation. Residential and commercial completed properties are generally eligible; agricultural land is not under any tokenization structure.

Determine Token Classification and Regulatory Trigger

Obtain a formal legal opinion on whether the proposed token is a security under SCRA. If yes, the full SEBI securities framework applies. If utility classification can be legitimately sustained, a lighter regime may apply. Proceed only on the basis of qualified legal counsel, not internal assumption.

Select Jurisdiction: Mainland India vs GIFT City

Evaluate whether the target investor profile (domestic retail vs NRI vs international institutional) and asset type are better served by a mainland SEBI structure or a GIFT City IFSCA entity. GIFT City offers faster framework clarity today but involves currency and capital account considerations for domestic Indian investors.

Construct the SPV Legal Structure and RERA Compliance Layer

Establish a Companies Act SPV to hold the property asset. Verify current RERA registration status of the property. Draft the trust deed, subscription agreement, and token rights document with full alignment between legal rights and smart contract logic. Engage RERA legal specialists for state-specific compliance review.

Build the Technology Stack and Commission Smart Contract Audit

Select a blockchain infrastructure appropriate for the offering scale and regulatory reporting requirements. Commission a full smart contract audit from a CERT-In empanelled firm before any investor interactions. Build KYC-gated transfer restrictions directly into the smart contract to enforce investor eligibility compliance programmatically.

Implement Investor Protection and Reporting Infrastructure

Register with SEBI SCORES for grievance management. Build periodic reporting dashboards for token holders covering property occupancy, rental income distribution, and NAV calculations. Establish an independent trustee to oversee SPV governance and protect investor interests independent of the platform operator and property manager.

Authoritative Compliance Principles and Risk Warnings: 8 Essential Standards

Principle 1: Substance Over Form

SEBI and Indian courts apply substance-over-form analysis to financial instruments. A token labeled as “utility” that economically functions as a security will be treated as a security. Regulatory classification cannot be engineered through nomenclature; it must reflect the actual economic rights conveyed to token holders.

Risk Warning: Unlicensed Platform Operations

Operating a tokenization marketplace in India without applicable SEBI registrations constitutes a violation of SEBI Act 1992 and can attract criminal prosecution, civil penalties, and platform closure orders. SEBI has demonstrated willingness to take enforcement action against unlicensed digital asset intermediaries operating in Indian markets.

Principle 2: RERA Non-Compliance is Non-Transferable

A property developer’s RERA violations cannot be insulated from investors by interposing a tokenization structure. Token holders in a RERA non-compliant project retain full legal exposure to the consequences of that non-compliance. RERA due diligence must precede and condition any tokenization decision, without exception.

Risk Warning: Misleading Return Projections

SEBI’s advertising and communications standards prohibit misleading or unsubstantiated return projections for investment products. Token offering documents or marketing materials that overstate projected yields or minimize risk disclosures expose issuers to SEBI enforcement and potential fraudulent misrepresentation liability under Indian law.

Principle 3: Investor Funds Must Be Segregated

Investor funds collected during token subscription must be held in escrow or trust accounts fully segregated from platform operating funds. Commingling investor capital with platform funds is a fundamental regulatory violation that SEBI treats with maximum severity, reflecting the hard lessons learned from past financial industry misconduct in India.

Risk Warning: Cross-Border Token Marketing Without Local Approvals

Marketing Indian real estate tokens to investors in the USA, UK, UAE, or Canada without complying with each jurisdiction’s securities marketing and registration requirements creates multi-jurisdictional legal exposure. Offshore distribution must be structured through locally-compliant distribution arrangements in each target market.

Principle 4: Continuous Regulatory Engagement

In a rapidly evolving regulatory environment like India’s tokenization space, proactive regulatory engagement is not just good practice but a competitive advantage. Platforms that engage early with SEBI and IFSCA through no-action letter requests, sandbox applications, and consultation paper responses shape the framework rather than being shaped by it.

Risk Warning: Liquidity Misrepresentation

Representing tokenized real estate as a liquid investment without a functioning SEBI-recognized secondary market is a material misrepresentation. In 2026, true secondary market liquidity for Indian real estate tokens remains limited. Platforms must disclose lock-in periods, transfer restrictions, and realistic exit timeline expectations to all prospective investors before subscription.

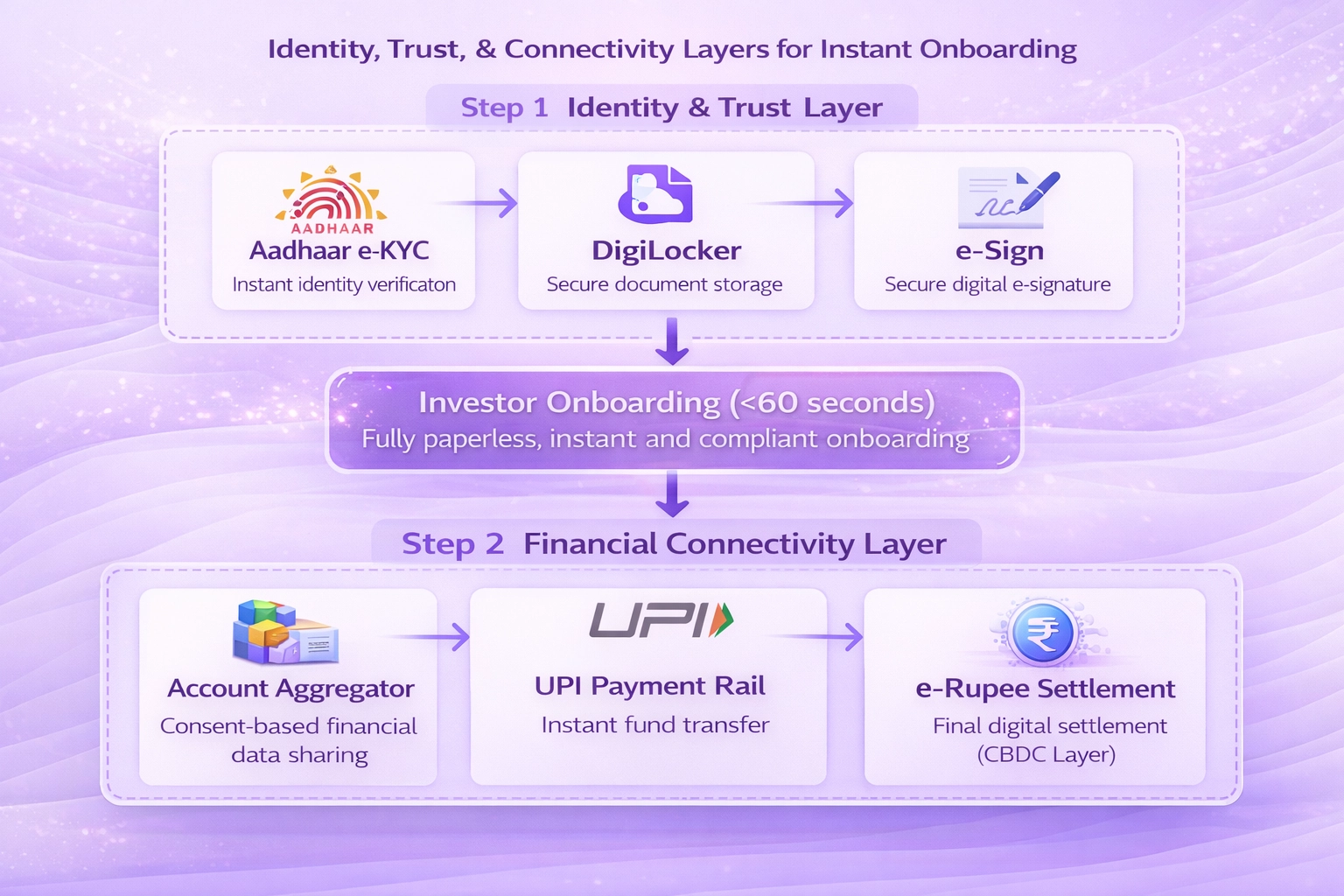

Integrated Identity and Financial Stack for Tokenized Asset Platforms

What Investors Must Verify Before Buying Real Estate Tokens Under SEBI’s 2026 Framework: A Practical Due Diligence Checklist

Every investor considering real estate tokenization in India must conduct rigorous independent due diligence before committing capital. The checklist below reflects the verification standards our advisory practice recommends based on consistent experience across markets in India, the USA, UK, UAE, and Canada.

People Also Ask

Q1.1. Is real estate tokenization legal in India?

Real estate tokenization in India exists in a regulatory grey zone in 2026. SEBI is actively developing frameworks, and platforms operating through GIFT City under IFSCA oversight have clearer legal standing. Always verify platform licensing before investing.

Q2.2. How does SEBI regulate real estate tokens?

SEBI classifies Real Estate Tokenization in India tokens based on their economic function. Tokens offering returns or profit sharing are treated as securities and fall under SEBI’s securities regulations, requiring full compliance with disclosure, registration, and investor protection norms before any public offering.

Q3.3. Can NRIs invest in tokenized real estate in India?

Yes, NRIs can invest in tokenized Real Estate Tokenization in India subject to FEMA regulations and RBI guidelines. Permitted asset classes, repatriation rules, and investment limits apply. Platforms must ensure NRI onboarding follows both SEBI KYC norms and FEMA compliance requirements simultaneously.

Q4.4. What taxes apply to real estate tokens in India?

Real Estate Tokenization in India attract capital gains tax on sale, TDS on income distributions, and GST on platform service fees. The 30% Virtual Digital Asset tax rate may also apply depending on token classification. Always consult a qualified tax advisor.

Q5.5. What is GIFT City's role in real estate tokenization?

GIFT City’s IFSCA provides a regulatory sandbox where tokenization platforms can operate with clearer oversight. It allows international investors including those from the USA, UK, UAE, and Canada to access Real Estate Tokenization in India offerings under a structured and more transparent compliance framework.

Q6.6. How do I verify if a real estate token platform is SEBI compliant?

Check the platform’s registration status on the SEBI website, confirm IFSCA licensing if operating from GIFT City, verify RERA registration of underlying properties, and review the token offering documents for mandatory disclosures. Never invest without confirmed regulatory standing.

Q7.7. What is the minimum investment in tokenized real estate in India?

Minimum investment thresholds vary by platform and token structure. SEBI-aligned platforms targeting retail investors typically set minimums between INR 10,000 and INR 1 lakh. Platforms under IFSCA may have different thresholds based on investor accreditation categories and asset class.

Q8.8. Is my investment safe in a real estate token platform?

Safety depends on regulatory compliance, underlying asset quality, and platform governance. SEBI-regulated platforms must maintain investor grievance mechanisms, audit trails, and escrow arrangements. Always review the smart contract audit report and legal offering documents before committing capital.

Q9.9. Can I sell my real estate tokens anytime?

Liquidity depends on whether the platform operates a secondary marketplace. Not all Indian tokenization platforms currently offer liquid secondary trading. Check the token’s lock-in period, transfer restrictions, and whether a SEBI-recognized trading venue is available for your specific token.

Q10.10. What documents should I check before buying a real estate token?

Review the token offering memorandum, underlying property RERA registration, smart contract audit report, platform SEBI or IFSCA license, KYC policy, and investor grievance process. Also check the legal opinion on token classification and the exit or redemption mechanism available to investors.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.