Ai Overview

Liquidity pool integration for market makers represents a fundamental shift from traditional order book trading to smart contract-based automated market making. For example, if a pool holds 100 ETH and 200,000 USDC (k = 20,000,000), a trader buying 10 ETH would receive fewer USDC per ETH than the current market price, with the exact amount calculated to preserve k after the trade.

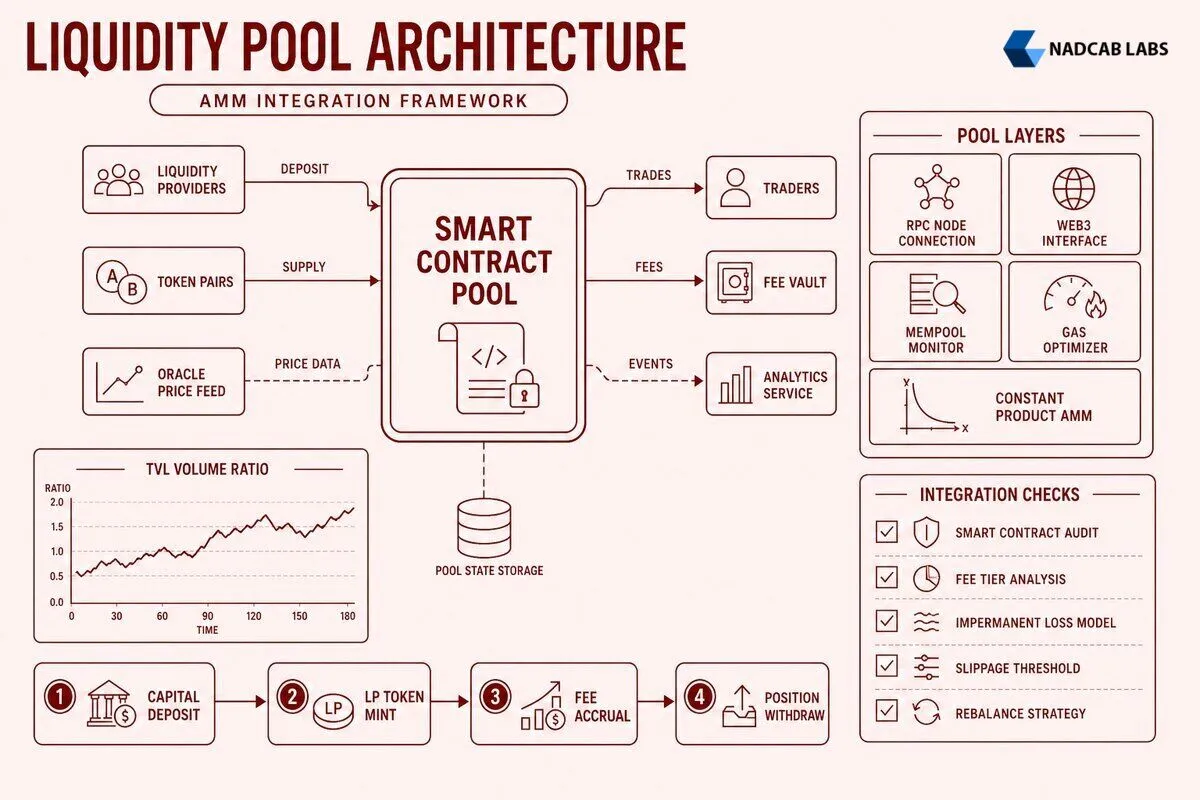

Liquidity pool integration for market makers represents a fundamental shift from traditional order book trading to smart contract-based automated market making. Market makers deploy capital into decentralized liquidity pools to earn fees from trades, reduce slippage for traders, and stabilize token prices across DeFi protocols. This integration requires understanding AMM mechanics, pool selection criteria, technical infrastructure requirements, and capital deployment strategies that differ significantly from centralized exchange approaches.

Key Takeaways

- Liquidity pools use smart contracts and constant product formulas to enable decentralized trading without traditional order books

- Market makers evaluate pools based on TVL, trading volume, fee tiers, impermanent loss risk, and smart contract audit status

- Technical integration requires RPC nodes, Web3 libraries, mempool monitoring, gas optimization systems, and real-time data pipelines

- Capital deployment strategies include risk-weighted distribution, correlation-based diversification, and dynamic rebalancing algorithms

- Performance monitoring tracks return on capital, impermanent loss, fee earnings, and comparative pool efficiency metrics

- Concentrated liquidity models like Uniswap V3 demand precise range optimization and active position management

What Are Liquidity Pools and Why Do Market Makers Integrate With Them?

A liquidity pool is a smart contract holding reserves of two or more tokens that enables decentralized trading without a traditional order book. Instead of matching buyers and sellers, traders swap tokens directly against the pool’s reserves, with prices determined algorithmically based on the ratio of tokens in the pool. This model removes the need for centralized intermediaries and enables 24/7 trading on blockchain networks.

Market makers provide continuous liquidity to these pools by depositing token pairs, which reduces slippage for traders and stabilizes pricing across DeFi protocols. When a market maker deposits assets into a pool, they receive liquidity provider (LP) tokens representing their proportional share of the pool. As traders execute swaps and pay fees, the market maker earns a percentage of those fees proportional to their pool share. This passive income stream compensates for the capital locked in the pool and the risks associated with price volatility.

The role of market makers in DeFi differs fundamentally from centralized exchange market making. On centralized platforms, market makers continuously update bid and ask orders, managing inventory and adjusting spreads based on market conditions. In liquidity pools, market makers deposit capital once and the AMM algorithm automatically prices trades. This reduces operational overhead but introduces new risks like impermanent loss, where the value of deposited tokens diverges from simply holding them. Market makers must understand these tradeoffs when deciding between centralized and decentralized liquidity provision strategies.

Professional market makers integrate with liquidity pools to access new markets, diversify revenue streams, and participate in emerging DeFi ecosystems. Many protocols offer additional incentives beyond trading fees, including governance token rewards and liquidity mining programs. These incentives can significantly boost returns but also introduce token price risk and lock-up periods that impact capital efficiency. Market makers must evaluate whether the combined fee earnings and incentives justify the technical complexity and risk exposure of pool integration.

The shift from order book to pool-based market making requires new technical capabilities. Market makers need infrastructure to monitor pool states across multiple chains, detect arbitrage opportunities, optimize gas costs for transactions, and manage positions dynamically as market conditions change. This technical foundation enables market makers to operate efficiently in DeFi while maintaining the risk management and performance standards expected in traditional markets.

How Do Automated Market Maker (AMM) Protocols Work With Liquidity Pools?

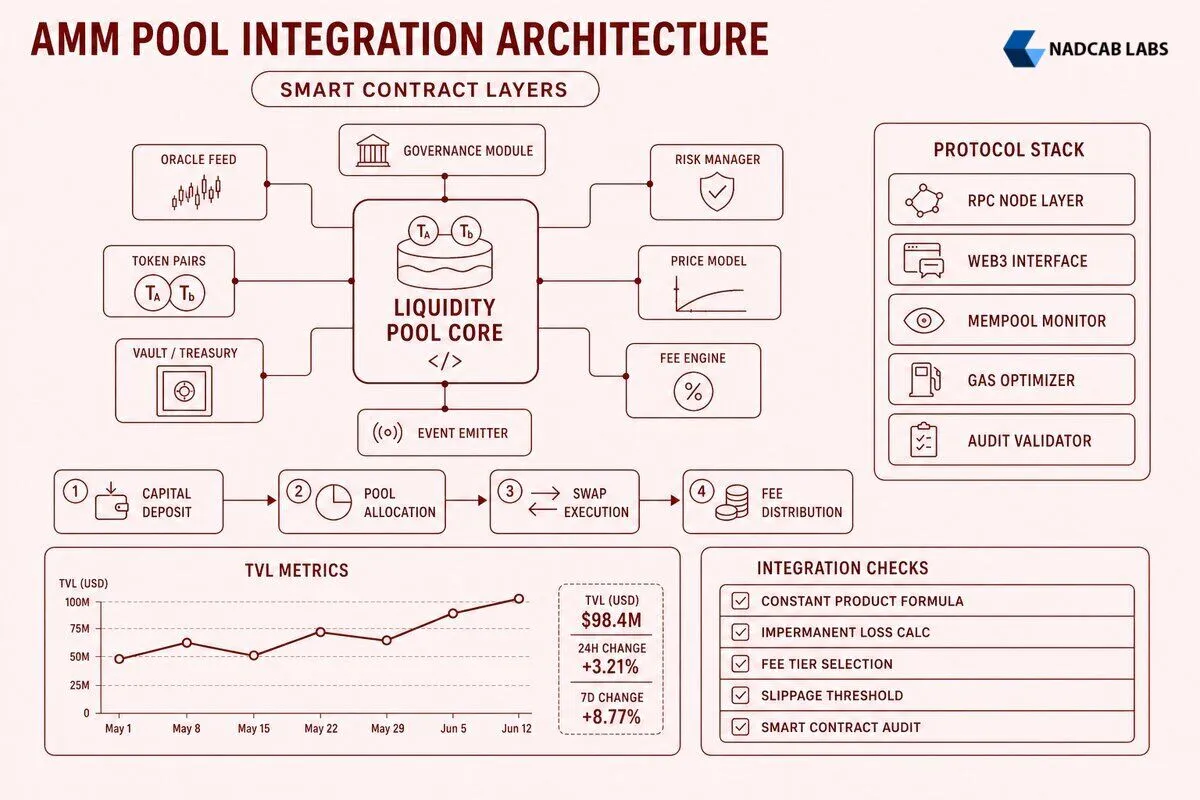

Automated market maker protocols use mathematical formulas to determine token prices based on pool reserves. The most common mechanism is the constant product formula, expressed as x * y = k, where x and y represent the quantities of two tokens in the pool and k is a constant. When a trader swaps token x for token y, the pool adjusts quantities to maintain the constant product, automatically setting a new price. For example, if a pool holds 100 ETH and 200,000 USDC (k = 20,000,000), a trader buying 10 ETH would receive fewer USDC per ETH than the current market price, with the exact amount calculated to preserve k after the trade.

This constant product model, pioneered by Uniswap V2, provides infinite liquidity across all price ranges but spreads capital inefficiently. Newer AMM designs like Uniswap V3 introduced concentrated liquidity, allowing market makers to deposit capital within specific price ranges. If ETH trades between $1,800 and $2,200, a market maker can concentrate their entire position in that range, earning significantly more fees per dollar of capital than spreading liquidity across all possible prices. However, if the price moves outside the specified range, the position stops earning fees and the market maker must manually rebalance.

The technical process of liquidity provision begins when a market maker deposits equal values of both tokens in a pair. The AMM smart contract mints LP tokens representing the market maker’s proportional share of the pool. If a pool contains $1 million in total liquidity and a market maker deposits $10,000, they receive 1% of the LP token supply. As traders execute swaps, the protocol charges a fee (typically 0.05% to 1%) and distributes it proportionally to all LP token holders. The market maker can redeem LP tokens at any time to withdraw their share of the pool, which includes accumulated fees but may differ in token composition from the original deposit due to trading activity.

Dynamic fee structures add another layer of complexity. Some protocols like Curve optimize for stablecoin swaps with low fees (0.04%) because price volatility is minimal, while volatile pairs on Uniswap charge higher fees (0.3% to 1%) to compensate for impermanent loss risk. Balancer pools support up to eight tokens with customizable weights and fees, enabling market makers to create specialized pools that match their risk preferences and market views. Understanding how different AMM designs handle fees, slippage, and capital efficiency is essential for effective pool integration.

Market makers integrate with AMM protocols through several technical touchpoints. Pool monitoring systems track reserve balances, trading volumes, fee accrual rates, and price movements in real time. Rebalancing triggers automatically detect when a concentrated liquidity position moves out of range or when impermanent loss exceeds predefined thresholds, prompting the market maker to adjust their position. Arbitrage opportunity detection compares pool prices against centralized exchange prices and other DEXs, identifying profitable trades that also help keep pool prices aligned with broader market rates. These integration points transform passive liquidity provision into an active, algorithmically managed strategy.

| AMM Protocol | Pricing Model | Typical Fee Range | Capital Efficiency | Best Use Case |

|---|---|---|---|---|

| Uniswap V2 | Constant Product (x*y=k) | 0.30% | Low (full range) | General token pairs |

| Uniswap V3 | Concentrated Liquidity | 0.05% to 1.00% | High (custom ranges) | Active market making |

| Curve Finance | StableSwap Invariant | 0.04% | Very High (stable pairs) | Stablecoin and pegged asset swaps |

| Balancer V2 | Weighted Constant Product | 0.01% to 10.00% | Medium (multi-asset) | Index funds and custom ratios |

| PancakeSwap | Constant Product (x*y=k) | 0.25% | Low (full range) | BSC ecosystem tokens |

What Criteria Should Market Makers Use to Select Liquidity Pools?

Pool selection begins with evaluating core metrics that indicate liquidity depth and trading activity. Total value locked (TVL) measures the dollar value of all assets deposited in a pool, with higher TVL generally indicating lower slippage and more stable pricing. A pool with $10 million TVL can absorb larger trades with less price impact than a $100,000 pool. Trading volume reveals how actively the pool is used, with higher volume generating more fee income for liquidity providers. Market makers should calculate the volume-to-TVL ratio to assess capital efficiency: a pool with $5 million TVL and $2 million daily volume (40% ratio) generates more fees per dollar of capital than a pool with $50 million TVL and $5 million daily volume (10% ratio).

Fee tier analysis helps market makers match their strategy to pool characteristics. Uniswap V3 offers multiple fee tiers (0.05%, 0.30%, 1.00%) for the same token pair, with lower fees attracting more volume for stable pairs and higher fees compensating for volatility risk on exotic tokens. Market makers must assess whether the fee premium justifies the additional impermanent loss exposure. For instance, a 1.00% fee pool on a volatile altcoin pair might earn three times the fees of a 0.30% pool, but if impermanent loss exceeds the fee differential, the lower-fee pool could deliver better net returns.

Impermanent loss risk assessment quantifies the potential value divergence between holding tokens versus providing liquidity. If a market maker deposits 1 ETH and 2,000 USDC when ETH is $2,000, and ETH later rises to $3,000, the pool rebalances to approximately 0.816 ETH and 2,449 USDC (maintaining the constant product). The market maker’s position is worth $4,898, but simply holding the original tokens would be worth $5,000 (1 ETH at $3,000 plus 2,000 USDC), resulting in $102 impermanent loss. Market makers use historical volatility data and correlation analysis to estimate impermanent loss probability across different pool options, selecting pairs where fee earnings are likely to exceed losses.

Protocol-specific considerations include smart contract audit status, governance model, upgrade mechanisms, and historical exploit records. Market makers should only integrate with pools that have undergone multiple independent security audits from reputable firms like Trail of Bits, ConsenSys Diligence, or OpenZeppelin. Governance models matter because protocol changes can affect fee structures, liquidity incentives, or pool parameters. Protocols with time-locked upgrades and community governance provide more predictability than those with centralized admin keys. Historical exploit records reveal whether a protocol has suffered hacks, flash loan attacks, or other security incidents that resulted in liquidity provider losses.

Strategic factors extend beyond pure metrics to competitive positioning and ecosystem alignment. Token pair correlation analysis identifies pools where both assets tend to move together, reducing impermanent loss. For example, ETH-stETH pools experience minimal impermanent loss because stETH tracks ETH price closely. Market depth requirements depend on the market maker’s capital size: deploying $1 million into a $500,000 pool would dominate the market and increase slippage, while the same capital in a $100 million pool has negligible impact. Competitor positioning reveals whether other sophisticated market makers are active in a pool, which can indicate attractive returns but also increased competition for fees. Cross-chain bridge compatibility matters for market makers operating across multiple networks, as pools that support LayerZero or Axelar enable more efficient capital deployment strategies.

Market makers should also consider liquidity mining incentives and governance token rewards when selecting pools. Many protocols distribute additional tokens to liquidity providers, sometimes doubling or tripling effective APY. However, these incentives often decline over time as protocols reduce emissions, and the governance tokens themselves carry price risk. A pool offering 50% APY from fees plus 100% APY from token rewards might look attractive, but if the reward token loses 80% of its value, the effective return becomes negative. Market makers must model different scenarios for token price trajectories and incentive decay when evaluating pools with additional rewards.

What Are the Technical Requirements for Seamless Pool Integration?

Infrastructure components form the foundation of liquidity pool integration, starting with reliable RPC node access to blockchain networks. Market makers need low-latency connections to submit transactions quickly and query pool states in real time. Running dedicated nodes provides the fastest access and eliminates third-party dependencies, but requires significant DevOps resources to maintain. Managed node services like Infura, Alchemy, or QuickNode offer easier setup with rate limits that may constrain high-frequency strategies. Market makers typically use a hybrid approach: dedicated nodes for critical operations and managed services as failover backups.

Blockchain indexers aggregate and organize on-chain data for efficient querying. The Graph protocol indexes smart contract events, allowing market makers to retrieve historical pool data, transaction histories, and liquidity changes without scanning every block. Dune Analytics and similar platforms provide pre-built dashboards for pool metrics, but custom indexers offer more flexibility for proprietary strategies. Market makers build indexing pipelines that track pool creations, liquidity additions/removals, swaps, and fee distributions across multiple DEXs, storing the data in time-series databases optimized for analytics.

Mempool monitoring tools detect pending transactions before they are confirmed on-chain, enabling market makers to anticipate large swaps that might move pool prices. By analyzing mempool data, market makers can front-run or back-run trades to capture arbitrage opportunities or adjust their positions before price impacts materialize. Tools like Blocknative, Eden Network, or custom mempool listeners connect to multiple network nodes to maximize transaction visibility. However, mempool monitoring is less effective on chains with private transaction pools or encrypted mempools, requiring alternative strategies for those networks.

Gas optimization systems minimize transaction costs, which can significantly impact profitability on high-fee networks like Ethereum mainnet. Market makers use dynamic gas pricing algorithms that analyze network congestion and adjust gas fees to balance confirmation speed and cost. Flashbots and other MEV (maximal extractable value) infrastructure allow market makers to submit transactions directly to block builders, bypassing the public mempool and reducing the risk of being front-run while potentially lowering gas costs. For chains with low transaction fees like Polygon or Arbitrum, gas optimization is less critical but still improves capital efficiency.

The smart contract interaction layer translates market maker strategies into blockchain transactions. Web3 libraries like ethers.js, web3.py, or viem provide interfaces to read pool states, encode function calls, and submit transactions. Market makers build abstraction layers on top of these libraries to standardize interactions across different AMM protocols, handling variations in function signatures, parameter formats, and return values. For example, adding liquidity to Uniswap V2 requires calling addLiquidity() with token addresses and amounts, while Uniswap V3 uses mint() with additional parameters for price ranges and tick spacing.

Transaction signing mechanisms secure private keys while enabling automated trading. Hardware security modules (HSMs) or cloud-based key management services like AWS KMS store private keys in tamper-resistant environments, requiring multi-signature approval for high-value transactions. Market makers implement nonce management systems to prevent transaction conflicts when submitting multiple operations simultaneously. Each Ethereum transaction includes a nonce (sequential number), and submitting two transactions with the same nonce causes one to fail. Robust nonce management tracks pending transactions, adjusts nonces for replacements or cancellations, and handles network reorgs that might invalidate transaction sequences.

Error handling protocols ensure resilience when transactions fail due to slippage, insufficient gas, or reverted smart contract calls. Market makers implement retry logic with exponential backoff, automatically resubmitting failed transactions with adjusted parameters. Slippage tolerance settings prevent trades from executing at unfavorable prices: if a market maker expects to receive 1,000 USDC for 1 ETH but sets 1% slippage tolerance, the transaction reverts if the actual output is less than 990 USDC. Circuit breakers halt trading when error rates exceed thresholds, preventing cascading failures during network congestion or smart contract bugs.

Data pipeline architecture ties all components together, ingesting real-time price feeds from oracles like Chainlink, Pyth, or Uniswap’s own TWAP (time-weighted average price) mechanisms. Pool state synchronization ensures the market maker’s internal models match on-chain reality, querying reserve balances, fee tiers, and liquidity distributions every block or using WebSocket subscriptions for instant updates. Event listeners monitor smart contract events like Swap, Mint, and Burn to track trading activity and liquidity changes as they occur. Historical data aggregation builds datasets for backtesting strategies, analyzing seasonal patterns, and training machine learning models that predict optimal entry and exit points.

Market makers often integrate Crypto Wallet API solutions to streamline transaction signing and asset management across multiple pools and chains. These APIs abstract the complexity of interacting with different wallet types, support multi-signature workflows for enhanced security, and provide unified interfaces for querying balances and transaction histories. By leveraging wallet APIs, market makers reduce development time and minimize the risk of security vulnerabilities in custom wallet implementations.

How Do Market Makers Deploy and Manage Capital Across Multiple Pools?

Capital allocation strategies determine how market makers distribute funds across different liquidity pools to optimize risk-adjusted returns. Risk-weighted distribution models assign capital based on each pool’s volatility, impermanent loss probability, and historical performance. A market maker might allocate 40% of capital to low-risk stablecoin pools, 35% to established token pairs like ETH-USDC, and 25% to higher-risk but potentially higher-reward altcoin pools. This approach balances stable base returns with upside potential from riskier positions.

Correlation-based diversification reduces portfolio-level impermanent loss by selecting pools with uncorrelated or negatively correlated token pairs. If a market maker provides liquidity to both ETH-USDC and BTC-USDC pools, and ETH and BTC prices tend to move together, the portfolio experiences similar impermanent loss patterns in both pools. Adding a pool like MATIC-USDC, where MATIC has lower correlation to ETH and BTC, diversifies the risk profile. Market makers calculate correlation matrices from historical price data and construct portfolios that minimize overall impermanent loss exposure while maintaining target return levels.

Dynamic rebalancing algorithms automatically adjust capital allocation as market conditions change. If a pool’s trading volume drops or impermanent loss exceeds thresholds, the algorithm reduces exposure by withdrawing liquidity and reallocating capital to better-performing pools. Rebalancing triggers include volume-to-TVL ratio falling below 10%, impermanent loss exceeding 5% of position value, or fee APY dropping below a minimum acceptable rate. These algorithms run continuously, analyzing pool metrics every hour or every block depending on the market maker’s strategy and infrastructure capabilities.

Position management workflows govern entry and exit timing to maximize fee earnings while minimizing impermanent loss. Market makers often enter pools during low-volatility periods when impermanent loss risk is minimal, and exit before major market events like protocol upgrades, token unlocks, or macroeconomic announcements that could trigger sharp price movements. For concentrated liquidity pools like Uniswap V3, liquidity range optimization is critical: setting ranges too narrow increases fee earnings but risks the position going out of range, while ranges too wide spread capital inefficiently. Market makers use volatility forecasts and historical price distributions to select optimal ranges that balance capital efficiency and active management overhead.

Automated withdrawal triggers protect capital during adverse conditions. If a pool experiences a security incident, a sudden liquidity exodus, or abnormal trading patterns suggesting manipulation, automated systems can withdraw liquidity within minutes to limit losses. Market makers set up monitoring alerts for smart contract events like Pause or EmergencyWithdraw, unusual spikes in swap sizes, or rapid TVL declines that might indicate a bank run. These triggers connect to emergency withdrawal functions that prioritize transaction speed over gas costs, ensuring the market maker exits before conditions deteriorate further.

Performance monitoring frameworks provide real-time visibility into portfolio health and individual pool contributions. Return on capital metrics calculate the annualized percentage yield from fee earnings, adjusting for impermanent loss to show net returns. A pool generating 30% APY from fees but experiencing 15% impermanent loss delivers 15% net APY, which market makers compare against alternative opportunities. Impermanent loss tracking shows cumulative divergence over time, helping market makers identify which pools consistently underperform due to volatility. Fee earnings analysis breaks down revenue by pool, protocol, and time period, revealing seasonal patterns or protocol-specific trends that inform future allocation decisions.

Comparative pool efficiency dashboards aggregate metrics across all positions, ranking pools by risk-adjusted returns and highlighting underperformers. Market makers use these dashboards to make data-driven reallocation decisions, shifting capital from pools with declining efficiency to emerging opportunities. The dashboards also track gas costs as a percentage of returns, ensuring that frequent rebalancing on high-fee networks does not erode profitability. On Ethereum mainnet, gas costs can consume 5-10% of returns for small positions, making larger, less frequent adjustments more economical than continuous micro-optimizations.

Integration with Market Making Software platforms automates much of this capital deployment and management workflow. Enterprise solutions provide pre-built connectors to major DEXs, risk management modules that enforce allocation limits, and backtesting environments where market makers can simulate strategies before deploying real capital. These platforms reduce the technical burden of multi-pool management and enable market makers to scale operations across dozens or hundreds of pools simultaneously.

Cross-chain capital deployment adds another dimension to portfolio management. Market makers operating on Ethereum, Polygon, Arbitrum, and other networks must bridge assets between chains, manage gas tokens for each network, and track positions across fragmented liquidity. Tools like LayerZero and Omnichain DeFi protocols simplify cross-chain operations by providing unified interfaces for asset transfers and liquidity management. Market makers can deploy capital to the most attractive pools regardless of which chain they reside on, optimizing global portfolio returns rather than being constrained by single-chain liquidity.

Understanding Liquidity Pool Architecture helps market makers design more efficient capital deployment strategies. Different pool architectures have varying gas costs, capital efficiency characteristics, and rebalancing requirements. Market makers who understand these architectural differences can select pools that align with their operational capabilities and risk tolerance, avoiding pools that require constant manual intervention or have hidden costs that erode returns.

The concepts discussed here also apply to specialized use cases like real estate token liquidity pool mechanics, where market makers provide liquidity for tokenized real estate assets. These pools often have lower trading volumes but higher fee tiers to compensate for illiquidity risk. Market makers must adapt their strategies to account for longer holding periods, regulatory considerations, and the unique characteristics of real estate-backed tokens when deploying capital in these emerging markets.

For market makers expanding into prediction markets, Prediction Market Development platforms offer opportunities to provide liquidity for binary outcome tokens. These markets have different risk profiles than standard token pairs, with liquidity needs that spike before event resolutions and collapse afterward. Market makers must time their entries and exits carefully, providing liquidity when premiums are high and withdrawing before market closure to avoid being locked into positions with known outcomes.

Finally, market makers should consider how liquidity pool integration fits into broader business operations. Tools like CRM Features help manage relationships with protocol teams, track incentive programs, and coordinate multi-party liquidity provision agreements. While CRM systems are not directly involved in trading operations, they support the strategic partnerships and business development activities that unlock access to exclusive pools, preferential fee structures, and early participation in new protocol launches.

Successful capital deployment across multiple pools requires combining quantitative analysis, technical infrastructure, and strategic positioning. Market makers who master these elements can generate consistent returns from DeFi liquidity provision while managing the unique risks of automated market maker protocols. As the DeFi ecosystem matures and new AMM designs emerge, the ability to rapidly evaluate, integrate, and optimize across diverse pool architectures will become an increasingly valuable competitive advantage.

Liquidity pool integration represents a fundamental component of modern market making strategies, bridging traditional finance expertise with decentralized protocol mechanics. Market makers who invest in robust technical infrastructure, develop sophisticated capital allocation algorithms, and maintain rigorous risk management practices can capture significant value from the growing DeFi ecosystem. The technical fundamentals covered in this guide provide the foundation for building scalable, profitable liquidity provision operations across multiple protocols and blockchain networks.

Frequently Asked Questions

Q1.How do market makers create liquidity in DeFi pools?

Market makers deposit paired assets into automated market maker (AMM) smart contracts at algorithmically determined ratios. They receive LP tokens representing their pool share and earn trading fees proportional to their contribution. Professional market makers deploy capital across multiple pools, monitor price ranges in concentrated liquidity protocols, and rebalance positions to optimize fee capture while managing impermanent loss exposure through hedging strategies and dynamic position sizing.

Q2.What is the best strategy for liquidity pool capital deployment?

Optimal deployment combines diversification across uncorrelated pairs, concentration in high-volume pools with sustainable fee structures, and active position management. Market makers analyze historical volatility, trading volume patterns, and fee tier performance. Concentrated liquidity strategies focus capital within tight price ranges for correlated pairs, while full-range positions suit volatile assets. Continuous monitoring, automated rebalancing, and hedging derivative positions mitigate impermanent loss while maximizing fee revenue.

Q3.How much does it cost to integrate with a liquidity pool as a market maker?

Integration costs include initial development ($15,000-$50,000 for custom infrastructure), gas fees for deposits/withdrawals ($20-$500 per transaction depending on network), ongoing monitoring systems ($5,000-$20,000 monthly), and API infrastructure. Ethereum mainnet operations incur higher costs; Layer 2 solutions reduce gas expenses by 90-95%. Professional setups require dedicated servers, real-time analytics, automated rebalancing tools, and risk management systems totaling $100,000-$300,000 annually for institutional operations.

Q4.What technical infrastructure is needed for AMM protocol integration?

Market makers require Web3 nodes (Infura, Alchemy, or self-hosted), smart contract interaction libraries (ethers.js, web3.py), secure wallet management systems with multi-signature support, real-time price feed aggregation, and automated position monitoring. Infrastructure includes database systems for transaction tracking, API connections to multiple DEXs, gas optimization tools, MEV protection mechanisms, and alerting systems. Professional operations deploy redundant systems, load balancers, and failover protocols ensuring 99.9% uptime.

Q5.How do market makers select which liquidity pools to provide capital to?

Selection criteria include trading volume consistency, fee tier analysis, historical impermanent loss metrics, token pair correlation, and protocol security audits. Market makers evaluate pool depth, competitor positioning, smart contract risk, and potential APY versus impermanent loss exposure. They prioritize pools with sustainable volume, established tokens, adequate liquidity depth, and favorable fee structures. Risk assessment includes protocol audit history, TVL stability, and governance token economics before capital deployment.

Q6.What are the key differences between providing liquidity on Uniswap v2 versus v3?

Uniswap v2 distributes liquidity uniformly across all price ranges with passive management, while v3 enables concentrated liquidity within custom price ranges for capital efficiency. V3 providers earn higher fees per dollar but face increased impermanent loss risk and require active rebalancing. V2 offers simplicity with set-and-forget positions; v3 demands sophisticated position management, frequent rebalancing, and technical expertise. V3 supports multiple fee tiers and NFT-based position tokens versus v2’s fungible LP tokens.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.