Ai Overview

Crypto payment gateway compliance is the set of regulatory, legal, and operational requirements that businesses must meet to lawfully process cryptocurrency transactions, including Anti-Money Laundering (AML) controls, Know Your Customer (KYC) verification, transaction monitoring, and jurisdiction-specific licensing.

Crypto payment gateway compliance is the set of regulatory, legal, and operational requirements that businesses must meet to lawfully process cryptocurrency transactions, including Anti-Money Laundering (AML) controls, Know Your Customer (KYC) verification, transaction monitoring, and jurisdiction-specific licensing. As digital asset payments scale globally, regulators demand the same rigorous standards applied to traditional financial services—making compliance architecture a foundational pillar of any production-ready Payment Gateway.

Key Takeaways

- Core compliance triad: AML transaction monitoring, multi-tier KYC verification, and FATF Travel Rule data exchange are mandatory for regulated crypto payment processing.

- Jurisdiction-specific frameworks: US requires FinCEN MSB registration plus state licenses; EU mandates MiCA and PSD2 compliance; Asia-Pacific varies widely by country.

- Architectural requirements: Real-time risk scoring, immutable audit trails, and automated regulatory reporting must be built into gateway infrastructure from day one.

- Non-compliance costs: Penalties range from six-figure fines to criminal prosecution, banking de-risking, and permanent market exclusion.

- Nadcab Labs approach: Pre-built modular compliance engines with jurisdiction-adaptive rulesets ensure businesses stay current across 50+ regulatory regimes without costly custom development.

- Compliance-by-design: Treating regulatory requirements as core product features—not afterthoughts—reduces risk, accelerates market entry, and builds merchant trust.

What Are the Core Compliance Requirements for Crypto Payment Gateways?

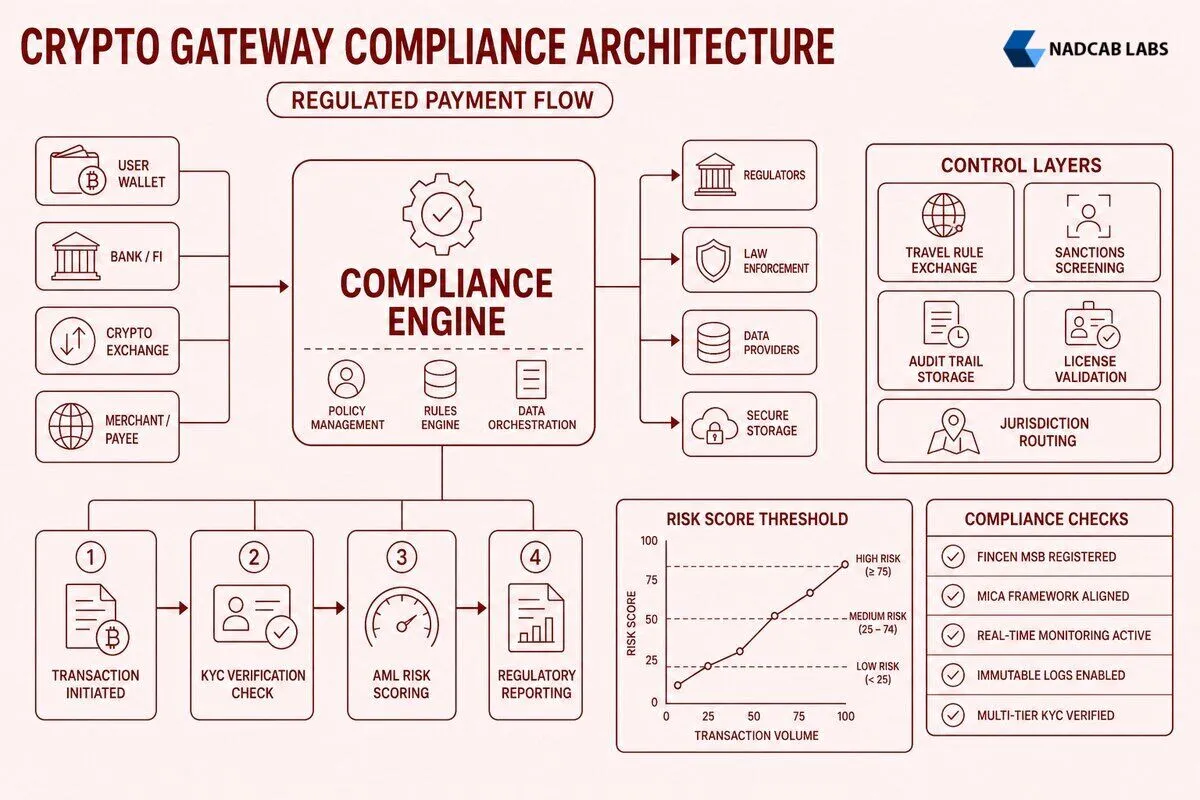

Every crypto payment gateway operating in regulated markets must implement three foundational compliance pillars: Anti-Money Laundering (AML) controls, Know Your Customer (KYC) verification, and cross-border transaction reporting under the Financial Action Task Force (FATF) Travel Rule. These requirements apply whether you process Bitcoin payments for e-commerce merchants or facilitate stablecoin settlements for enterprise clients.

AML obligations begin with transaction monitoring systems that analyze payment flows in real time. Gateways must flag suspicious patterns—rapid transfers between unrelated wallets, structuring below reporting thresholds, or transactions involving sanctioned addresses. When the system detects anomalies, operators file Suspicious Activity Reports (SARs) with national Financial Intelligence Units within mandated timeframes, typically 30 days in the US and EU. Record-keeping mandates require storing transaction metadata, customer due diligence files, and correspondence for five to seven years depending on jurisdiction.

KYC verification operates on a tiered model. Basic identity checks—name, date of birth, residential address—suffice for low-value transactions, often under $1,000 per day. Enhanced due diligence kicks in for high-risk scenarios: large transaction volumes, cross-border payments, or customers from jurisdictions with weak AML frameworks. Enhanced KYC includes source-of-funds documentation, beneficial ownership disclosure for corporate accounts, and ongoing monitoring of customer behavior against their declared business profile. A merchant processing $50,000 monthly in crypto payments faces far stricter verification than a consumer wallet making occasional purchases.

The FATF Travel Rule, implemented in over 60 countries, requires crypto service providers to share originator and beneficiary information for transactions exceeding approximately $1,000 (exact thresholds vary by jurisdiction). When a customer sends Bitcoin from your gateway to an external exchange, you must transmit the sender’s name, account identifier, and physical address to the receiving platform. This data exchange mirrors wire transfer protocols in traditional banking. Non-compliance blocks access to banking partners and regulated exchanges, effectively isolating your gateway from the mainstream financial system.

| Compliance Requirement | Trigger Threshold | Data Collected | Retention Period |

|---|---|---|---|

| Basic KYC | All onboarding | Name, DOB, address, ID document | 5 years post-closure |

| Enhanced Due Diligence | >$10,000/day or high-risk profile | Source of funds, beneficial owners, business model | 7 years post-closure |

| Travel Rule Reporting | >$1,000 (varies by jurisdiction) | Originator/beneficiary name, address, account ID | 5 years from transaction |

| SAR Filing | Suspicious activity detected | Transaction details, customer profile, suspicion rationale | 5 years from filing |

| CTR Filing (US) | >$10,000 cash equivalent/day | Customer identity, transaction amount, date/time | 5 years from filing |

Implementing these controls requires more than policy documents. Your crypto payment gateway security architecture must embed compliance checks into transaction processing flows, customer onboarding workflows, and backend reporting systems. Manual compliance processes cannot scale when processing thousands of transactions daily across multiple cryptocurrencies and fiat corridors.

How Do Regional Regulatory Frameworks Differ Across Major Jurisdictions?

Regulatory approaches to crypto payment gateways vary dramatically by geography, reflecting each region’s financial system maturity, policy priorities, and enforcement capacity. Businesses operating internationally face a complex patchwork of overlapping and sometimes conflicting requirements.

In the United States, crypto payment gateways typically register as Money Service Businesses (MSBs) with the Financial Crimes Enforcement Network (FinCEN), a division of the Treasury Department. MSB registration triggers federal AML obligations: written compliance programs, independent audits, SAR filing, and Currency Transaction Report (CTR) submission for cash-equivalent transactions exceeding $10,000. Beyond federal requirements, most states classify crypto gateways as money transmitters, requiring separate licenses in each operating state. New York’s BitLicense, for example, imposes capital reserve requirements, cybersecurity audits, and consumer protection standards that exceed federal minimums. A gateway serving customers nationwide may need 40+ state licenses, each with distinct application fees, bonding requirements, and ongoing reporting obligations.

The Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) assert jurisdiction when gateways process payments in tokens classified as securities or commodities. If your gateway accepts utility tokens that fail the Howey Test for securities, you may face SEC registration requirements as a broker-dealer or alternative trading system. The regulatory classification of each supported cryptocurrency determines your compliance burden—Bitcoin and Ethereum are generally treated as commodities, while many altcoins occupy legal gray zones.

The European Union has harmonized crypto regulation through the Markets in Crypto-Assets (MiCA) framework, effective across all 27 member states. MiCA establishes licensing categories for crypto-asset service providers (CASPs), including payment processors. Gateways must obtain authorization from a national competent authority in one EU country, then passport services across the bloc. MiCA mandates capital adequacy standards, operational resilience requirements, and consumer disclosure obligations. Payment Service Directive 2 (PSD2) applies when gateways convert crypto to fiat or vice versa, requiring separate payment institution licensing. The General Data Protection Regulation (GDPR) adds strict data handling requirements: pseudonymization of customer records, data portability rights, and breach notification within 72 hours. EU gateways must balance blockchain transparency with privacy rights—a technical and legal challenge when transaction data lives on public ledgers.

Asia-Pacific markets demonstrate the widest regulatory divergence. Singapore’s Monetary Authority (MAS) licenses payment service providers under a risk-based framework, with different tiers for small domestic operators versus large cross-border platforms. Japan’s Payment Services Act requires crypto exchange licensing for any business facilitating crypto-to-fiat conversion, with stringent capital, security, and customer asset segregation rules. Hong Kong’s Securities and Futures Commission (SFC) licenses virtual asset trading platforms but carves out exemptions for pure payment processing. Australia treats crypto gateways as remittance service providers under AUSTRAC oversight, requiring registration and AML/CTF program implementation. India’s regulatory stance remains fluid—while not banned, crypto businesses operate without explicit licensing frameworks, relying on self-regulatory compliance with existing financial sector laws.

Identify all countries where your gateway will serve customers or process transactions, then catalog applicable regulations (AML laws, payment services acts, data protection rules).

Determine required licenses (MSB, money transmitter, CASP, payment institution) and application timelines—some jurisdictions require 12+ months for approval.

Build written AML/KYC policies, appoint a compliance officer, establish transaction monitoring rules, and create SAR/CTR filing procedures tailored to each jurisdiction.

Integrate compliance modules into gateway architecture—KYC verification APIs, transaction screening engines, audit logging, and regulatory reporting automation.

Track regulatory changes, update compliance rules, conduct annual independent audits, and maintain examiner-ready documentation for regulatory inspections.

The crypto payment gateway integration time increases significantly when accounting for multi-jurisdiction compliance. A US-only gateway might launch in 3-4 months; adding EU and Asia-Pacific coverage extends timelines to 9-12 months due to licensing, legal review, and architecture modifications for region-specific rules.

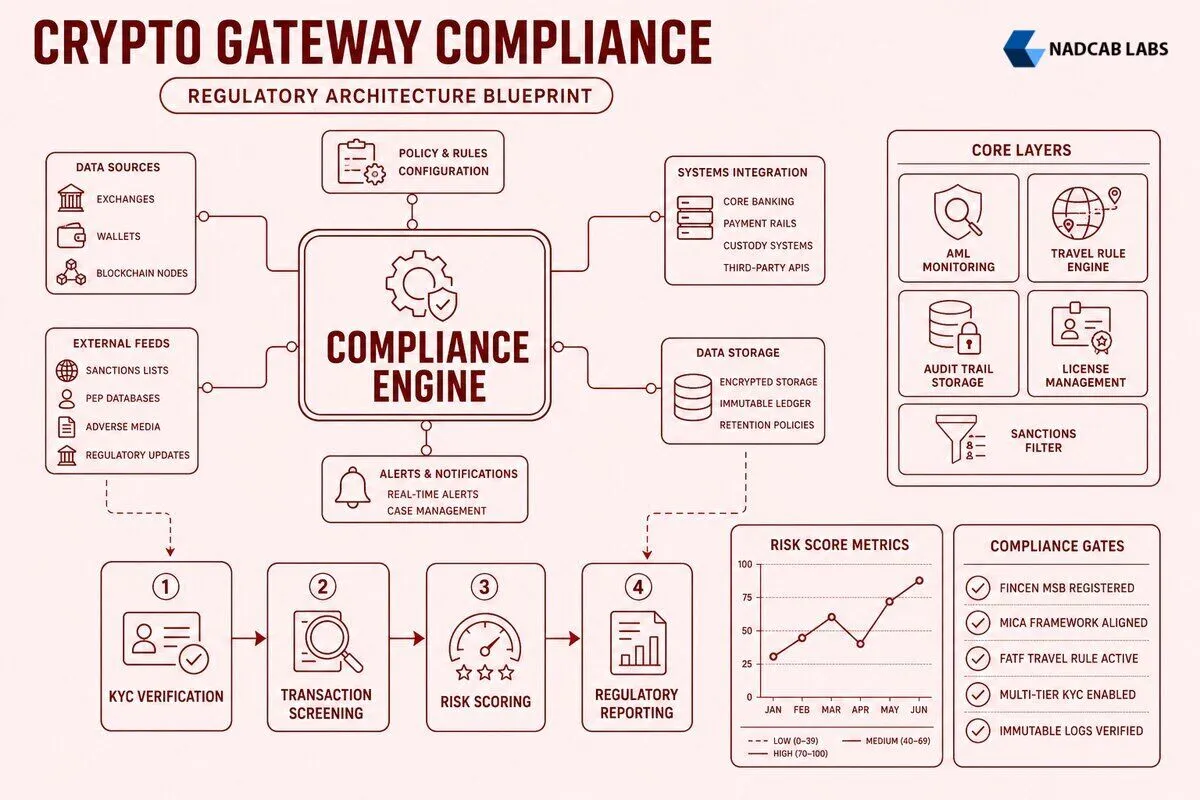

Which Compliance Features Must Be Built Into Gateway Architecture?

Regulatory compliance cannot be bolted onto existing payment infrastructure as an afterthought. Effective crypto payment gateways embed compliance capabilities into core system architecture, treating regulatory requirements as first-class product features rather than operational overhead.

Real-time transaction monitoring forms the backbone of AML compliance. Your gateway must analyze every payment against configurable risk scoring algorithms that evaluate transaction size, frequency, counterparty risk, geographic origin, and behavioral patterns. A typical scoring model assigns numerical risk values across multiple dimensions: a $500 Bitcoin payment from a verified customer to a known merchant scores low; a $15,000 transfer to a newly created wallet in a high-risk jurisdiction scores high. When aggregate risk exceeds predefined thresholds, the system automatically flags transactions for compliance review, temporarily holds funds, or blocks processing entirely.

Effective monitoring requires integrating external data sources. Sanction screening APIs check wallet addresses and customer identities against OFAC, UN, and EU sanctions lists in real time. Blockchain analytics services—Chainalysis, Elliptic, CipherTrace—provide risk intelligence on destination addresses, identifying wallets associated with darknet markets, ransomware operators, or sanctioned entities. Your gateway queries these services before confirming each transaction, rejecting payments to flagged addresses regardless of customer intent.

Multi-tier customer verification workflows support both regulatory compliance and business scalability. Tier 1 verification—email confirmation and basic identity data—enables small transactions up to daily limits, perhaps $500-$1,000. Tier 2 adds government-issued ID verification through document scanning and facial biometric matching, raising limits to $10,000-$25,000 daily. Tier 3 enhanced due diligence includes proof of address, source-of-funds documentation, and video verification calls, removing transaction limits for institutional clients. This tiered approach balances regulatory obligations with user experience—casual consumers complete onboarding in minutes, while high-volume merchants undergo thorough vetting.

Verification workflows integrate with identity verification service providers: Onfido, Jumio, Sumsub, or Persona. These platforms use machine learning to detect forged documents, match selfies to ID photos, and cross-reference customer data against global identity databases. Your gateway API calls these services during onboarding, receiving pass/fail decisions and risk scores that inform account approval. Ongoing screening runs periodically—monthly or quarterly—to catch customers who appear on sanctions lists after initial verification.

Comprehensive audit trails and reporting infrastructure ensure regulatory examiners can reconstruct any transaction’s complete history. Every customer action—login, KYC submission, transaction initiation, compliance review decision—generates an immutable log entry with timestamps, IP addresses, device fingerprints, and user agent data. Storing these logs on blockchain infrastructure provides tamper-proof evidence that satisfies regulatory scrutiny. When a regulator requests transaction records during an investigation, your system generates detailed reports spanning months or years without manual data compilation.

Automated regulatory filing systems reduce operational burden and human error. When transaction monitoring flags suspicious activity, the compliance module generates pre-filled SAR drafts with relevant transaction details, customer profiles, and risk indicators. Compliance officers review and submit these reports to FinCEN or equivalent agencies through secure portals. Similarly, CTR filing for large transactions happens automatically when daily volumes exceed thresholds, with the system aggregating related transactions from the same customer to detect structuring attempts.

| Compliance Feature | Technical Implementation | Data Sources | Performance Impact |

|---|---|---|---|

| Transaction Screening | Pre-confirmation API calls to sanctions/risk databases | OFAC, UN, Chainalysis, Elliptic | +200-500ms latency per transaction |

| KYC Verification | Document OCR, facial biometrics, liveness detection | Onfido, Jumio, government ID databases | 2-5 minute onboarding flow |

| Travel Rule Exchange | Encrypted peer-to-peer messaging protocols (IVMS101) | Counterparty VASPs, TRP networks | +1-3 second settlement delay |

| Behavioral Analytics | Machine learning models on historical transaction patterns | Internal transaction database, fraud indicators | Negligible (offline model training) |

| Audit Logging | Blockchain-anchored immutable event logs | All system events, user actions, admin decisions | +50-100MB storage per 10k transactions |

The HIPAA compliant blockchain architecture principles apply equally to crypto payment compliance: data encryption at rest and in transit, role-based access controls limiting who views sensitive customer information, and comprehensive audit trails documenting every data access event. While HIPAA governs healthcare data, the same architectural patterns ensure financial data protection under GDPR, CCPA, and sector-specific regulations.

What Are the Consequences of Non-Compliance and How Can Businesses Mitigate Risk?

The financial and operational penalties for crypto payment gateway non-compliance range from manageable fines to business-ending enforcement actions. Understanding these risks motivates proper investment in compliance infrastructure rather than treating regulatory requirements as optional overhead.

Financial penalties start with administrative fines from regulatory agencies. FinCEN assesses civil penalties up to $25,000 per violation for MSB non-compliance, with no cap on total fines when violations span thousands of transactions. The Office of the Comptroller of the Currency (OCC) and state banking regulators impose similar penalties for unlicensed money transmission. European data protection authorities levy GDPR fines up to €20 million or 4% of global annual revenue, whichever is higher—a catastrophic sum for mid-sized payment processors. In 2023, a European crypto exchange paid €4.3 million for inadequate KYC controls; in 2022, a US-based payment platform settled FinCEN charges for $100 million related to AML program failures.

Criminal prosecution represents the extreme end of enforcement. Willful violations of the Bank Secrecy Act carry criminal penalties: up to five years imprisonment and $250,000 in fines per count. Operating an unlicensed money transmitting business is a federal felony under 18 U.S.C. § 1960, with similar maximum penalties. While criminal charges typically target egregious cases—operators knowingly facilitating money laundering or terrorist financing—the legal risk exists whenever businesses process payments without required licenses or ignore obvious red flags in transaction monitoring.

Operational shutdowns occur when regulators issue cease-and-desist orders, forcing immediate suspension of payment processing. State banking departments shut down unlicensed money transmitters; the SEC halts unregistered securities offerings; data protection authorities block processing of EU citizen data. These actions freeze merchant revenue, strand customer funds, and destroy business continuity. Recovery requires months of remediation, regulatory negotiation, and often complete platform rebuilds to meet compliance standards.

Banking relationship termination may be the most insidious consequence. Commercial banks practice “de-risking”—terminating accounts for businesses in high-risk sectors to avoid regulatory scrutiny. Crypto payment gateways without robust compliance programs lose bank accounts, making fiat settlement impossible. Once blacklisted by major banks, businesses struggle to find banking partners willing to accept them, even after implementing compliance improvements. This effectively excludes non-compliant gateways from regulated markets.

Reputational damage compounds financial losses. Merchants abandon payment gateways associated with regulatory violations, fearing their own compliance exposure. Investors withdraw funding from non-compliant startups. Partnership opportunities with established financial institutions evaporate when due diligence reveals regulatory deficiencies. Rebuilding trust takes years and requires transparent demonstration of compliance improvements.

Compliance Risk Severity by Violation Type

Compliance-by-design strategies mitigate these risks by treating regulatory requirements as core product features from the earliest development stages. Rather than building a payment gateway and retrofitting compliance, businesses architect systems with modular regulatory components that can be configured for different jurisdictions without core code modifications. A well-designed gateway allows merchants to toggle between US, EU, and Asia-Pacific compliance rulesets through configuration files, automatically applying appropriate KYC thresholds, transaction limits, and reporting protocols based on customer location.

Jurisdiction-specific configuration templates accelerate market entry. When expanding to a new country, compliance teams load pre-built rule templates covering that jurisdiction’s AML thresholds, KYC verification levels, and reporting formats. The gateway automatically adapts transaction monitoring algorithms, customer verification workflows, and regulatory filing procedures without custom development. This approach reduces compliance integration time from months to weeks.

Continuous monitoring updates ensure gateway features align with evolving regulations. Regulatory requirements change frequently—new sanctions lists, revised Travel Rule thresholds, updated licensing requirements. Businesses that treat compliance as a one-time implementation project fall out of alignment within months. Effective gateways subscribe to regulatory intelligence services that track changes across dozens of jurisdictions, automatically updating screening databases, transaction limits, and reporting templates as regulations evolve.

The Crypto Wallet Compliance considerations extend to payment gateways: both must implement similar AML/KYC controls, Travel Rule protocols, and sanctions screening. However, gateways face additional merchant onboarding requirements, settlement account monitoring, and payment service provider licensing that pure wallet providers may avoid.

How Does Nadcab Labs Implement Regulatory Compliance in Payment Gateway Solutions?

Nadcab Labs approaches crypto payment gateway compliance as a core engineering discipline rather than a legal checkbox, building regulatory capabilities into every layer of gateway architecture. Our compliance-first methodology ensures businesses launch with production-ready systems that satisfy regulators in 50+ jurisdictions without costly post-launch remediation.

Pre-built compliance modules form the foundation of our gateway solutions. Rather than building AML/KYC systems from scratch, clients deploy battle-tested components covering transaction monitoring, customer verification, Travel Rule data exchange, and automated regulatory reporting. These modules integrate with leading third-party services—Chainalysis for blockchain analytics, Onfido for identity verification, SEON for fraud detection—through standardized APIs that reduce integration complexity. A typical deployment connects 8-12 compliance service providers through our unified interface layer, eliminating the need for merchants to negotiate separate contracts and manage multiple vendor relationships.

Our transaction monitoring engine implements configurable risk scoring algorithms that evaluate payments across 20+ dimensions: transaction size, frequency, velocity, counterparty risk, geographic origin, time-of-day patterns, and behavioral deviations from customer history. Compliance officers define risk thresholds through an administrative dashboard, adjusting sensitivity based on business risk appetite and regulatory requirements. When the system flags high-risk transactions, it automatically generates case files with all relevant data—customer profile, transaction history, blockchain forensics, external risk intelligence—enabling rapid compliance review without manual data gathering.

Multi-tier KYC workflows support both consumer convenience and regulatory rigor. Tier 1 verification—email and phone confirmation—enables small transactions within minutes of signup. Tier 2 adds government ID verification through document scanning, facial biometrics, and liveness detection, completing in 2-5 minutes for most customers. Tier 3 enhanced due diligence incorporates proof of address, source-of-funds documentation, and manual compliance review for high-value or high-risk accounts. This tiered approach balances user experience with regulatory obligations, allowing Businesses Need a Crypto Payment Gateway to onboard customers efficiently while maintaining compliance.

Travel Rule data exchange protocols integrate with major Travel Rule Protocol (TRP) networks—Sygna Bridge, Notabene, CipherTrace Traveler—enabling seamless originator/beneficiary information exchange with counterparty VASPs. When a customer initiates a cross-border payment exceeding jurisdiction thresholds, our gateway automatically queries the TRP network for the receiving VASP’s compliance endpoint, transmits required data through encrypted channels, and awaits confirmation before releasing funds. This automated process adds only 1-3 seconds to settlement time while ensuring full Travel Rule compliance.

Jurisdiction-adaptive architecture allows merchants to operate across multiple regulatory regimes without maintaining separate gateway instances. Our configuration engine stores jurisdiction-specific rulesets covering KYC thresholds, transaction limits, reporting requirements, and data localization mandates for 50+ countries. When a customer from Germany initiates a payment, the gateway automatically applies EU MiCA rules, GDPR data handling protocols, and PSD2 payment service requirements. A customer from Singapore triggers MAS Payment Services Act compliance rules. This multi-jurisdiction capability is essential for businesses serving international markets, eliminating the need to deploy separate infrastructure in each country.

Ongoing regulatory intelligence updates ensure gateway features remain current as regulations evolve. Our compliance team monitors regulatory developments across major jurisdictions, tracking proposed legislation, agency guidance, and enforcement actions. When regulations change—new Travel Rule thresholds, updated sanctions lists, revised licensing requirements—we push configuration updates to client gateways, automatically adjusting transaction monitoring rules, verification workflows, and reporting templates. This continuous update model prevents compliance drift that occurs when businesses treat regulatory implementation as a one-time project.

Comprehensive audit trails leverage blockchain infrastructure for tamper-proof record-keeping. Every system event—customer login, KYC submission, transaction initiation, compliance review decision, admin action—generates a log entry that we hash and anchor to a public blockchain. This creates an immutable audit trail that satisfies regulatory scrutiny during examinations or investigations. When regulators request transaction records, our reporting module generates detailed chronological reports spanning months or years, with blockchain proof that records have not been altered.

Automated regulatory filing systems reduce operational burden for compliance teams. When transaction monitoring flags suspicious activity, the system generates pre-filled SAR drafts with relevant transaction details, customer profiles, and risk indicators. Compliance officers review these drafts and submit them to FinCEN or equivalent agencies through secure API connections. Similarly, CTR filing for large transactions happens automatically when daily volumes exceed thresholds, with the system aggregating related transactions to detect structuring attempts. This automation reduces compliance staffing requirements while improving filing accuracy and timeliness.

Our modular architecture supports both turnkey deployments and custom integrations. Businesses seeking rapid market entry deploy our complete compliance stack—transaction monitoring, KYC verification, Travel Rule exchange, audit logging, and regulatory reporting—as a unified solution. Enterprises with existing compliance infrastructure integrate specific modules into their systems, perhaps adding our Travel Rule engine to an existing gateway or deploying our transaction monitoring system alongside proprietary KYC workflows. This flexibility accommodates diverse business models and technical architectures.

The same compliance-by-design principles that power our payment gateways extend to related products. Our Crypto Derivatives Exchange Development services implement similar AML/KYC controls, position monitoring, and margin call compliance systems. Our p2p cryptocurrency exchange solutions embed escrow compliance, dispute resolution protocols, and seller verification workflows. Across all products, regulatory compliance is a foundational engineering requirement rather than an afterthought.

Businesses evaluating crypto payment gateway solutions should prioritize compliance capabilities alongside technical performance and feature richness. A gateway that processes transactions quickly but lacks robust AML controls exposes merchants to regulatory risk that can destroy business value overnight. Nadcab Labs’ compliance-first approach ensures businesses launch with production-ready systems that satisfy regulators today while adapting to regulatory changes tomorrow.

Final Thoughts

Crypto payment gateway compliance represents a complex, evolving challenge that demands technical sophistication, legal expertise, and operational discipline. Businesses cannot treat regulatory requirements as optional overhead or afterthoughts bolted onto existing systems. The financial penalties, operational shutdowns, and reputational damage from non-compliance far exceed the cost of building proper compliance infrastructure from the start. By embedding AML transaction monitoring, multi-tier KYC verification, Travel Rule data exchange, and automated regulatory reporting into core gateway architecture, businesses create systems that satisfy regulators across dozens of jurisdictions while delivering seamless user experiences. Nadcab Labs’ compliance-first methodology, pre-built regulatory modules, and jurisdiction-adaptive architecture enable businesses to launch production-ready payment gateways that balance regulatory obligations with commercial objectives. As digital asset adoption accelerates and regulatory frameworks mature, compliance capabilities will increasingly differentiate market leaders from businesses forced to exit regulated markets. Investing in robust compliance infrastructure today positions businesses for sustainable growth in the evolving global crypto payments landscape.

Frequently Asked Questions

Q1.What is the FATF Travel Rule and how does it apply to crypto payment gateways?

The FATF Travel Rule requires Virtual Asset Service Providers (VASPs), including crypto payment gateways, to collect and transmit originator and beneficiary information for transactions exceeding USD/EUR 1,000. Gateways must implement technical solutions to exchange customer data with counterparty institutions, maintain transaction records for five years, and screen parties against sanctions lists. Non-compliance risks regulatory penalties and loss of banking relationships across jurisdictions.

Q2.Do all crypto payment gateways need to register as Money Service Businesses in the US?

Yes, most crypto payment gateways operating in the US must register with FinCEN as Money Service Businesses (MSBs) under federal law. Additionally, they typically require state-level money transmitter licenses in each operational state, with exceptions like Montana and South Carolina. Registration mandates include appointing a compliance officer, implementing AML programs, filing Suspicious Activity Reports (SARs), and maintaining comprehensive transaction monitoring systems.

Q3.How does MiCA regulation affect crypto payment gateway operations in Europe?

The Markets in Crypto-Assets Regulation (MiCA), effective 2024-2025, requires crypto payment gateways to obtain authorization as Crypto-Asset Service Providers (CASPs) from national competent authorities. Gateways must maintain minimum capital reserves, implement robust custody arrangements, provide transparent fee disclosures, and comply with strict consumer protection standards. MiCA enables EU-wide passporting, allowing authorized gateways to operate across all member states with single-country approval.

Q4.What KYC verification level is required for different transaction sizes in crypto payments?

KYC requirements typically follow tiered structures: Basic verification (name, email, phone) for transactions under $1,000-$2,000; Enhanced KYC (government ID, address proof, selfie verification) for $2,000-$10,000; Full due diligence (source of funds, business documentation, beneficial ownership) above $10,000. Thresholds vary by jurisdiction—EU MiCA mandates KYC at €1,000, while some Asian jurisdictions require verification from the first transaction regardless of amount.

Q5.Can a crypto payment gateway operate globally with a single compliance framework?

No, global operation requires jurisdiction-specific compliance frameworks due to divergent regulatory requirements. While core AML/KYC principles overlap, licensing requirements, data residency rules, capital adequacy standards, and consumer protection laws vary significantly. Gateways must implement modular compliance architectures with jurisdiction-specific modules, maintain separate legal entities in major markets, and continuously monitor regulatory changes across 50+ jurisdictions for comprehensive global coverage.

Q6.What are the penalties for AML violations in crypto payment processing?

AML violations carry severe penalties: US FinCEN can impose fines up to $250,000 per violation or twice the transaction value, plus criminal penalties of 5-10 years imprisonment for willful violations. EU authorities levy fines reaching €5 million or 10% of annual turnover under MiCA. Additional consequences include license revocation, operational shutdowns, director disqualification, and reputational damage. Recent enforcement actions have resulted in settlements exceeding $100 million for major platforms.

Explore Services

Related Services

Reviewed by

Wazid Khan

Director & Co-Founder

Wazid Khan is the Director & Co-Founder of Nadcab Labs, a forward-thinking digital engineering company specializing in Blockchain, Web3, AI, and enterprise software solutions. With a strong vision for innovation and scalable technology, Wazid has played a key role in building Nadcab Labs into a trusted global technology partner. His expertise lies in strategic planning, business development, and delivering client-centric solutions that drive real-world impact. Under his leadership, the company has successfully delivered numerous projects across industries such as fintech, healthcare, gaming, and logistics. Wazid is passionate about leveraging emerging technologies to create secure, efficient, and future-ready digital ecosystems for businesses worldwide.