Ai Overview

Every financial platform operating today, whether in Mumbai, Bengaluru, Dubai, or Abu Dhabi, faces one fundamental question before it can serve a single customer: who exactly is this person? That question is the heartbeat of know your customer regulations. The difference in cost, time, and legal exposure is enormous. Machine learning models trained on millions of global documents now achieve over 99% accuracy in document verification system checks, far outperforming manual review at a fraction of the cost.

Key Takeaways

- Know your customer compliance is legally mandated in India, UAE, and globally, covering every financial platform onboarding users or processing transactions.

- Customer identity verification and customer due diligence are core pillars that prevent financial fraud and protect company reputation from day one.

- Electronic Know Your Customer (eKYC) dramatically reduces onboarding time from days to minutes while maintaining full anti money laundering compliance standards.

- Skipping know your customer checks exposes financial software companies to regulatory fines, license revocation, and criminal liability for senior management teams.

- Biometric identity verification and document verification systems are now standard tools in modern regulatory compliance software for financial platforms.

- Transaction monitoring software combined with risk assessment in banking creates a continuous compliance loop well beyond the initial onboarding process.

- AML and KYC regulations in India (RBI, SEBI, PMLA) and UAE (CBUAE, DFSA) share common goals but require localized implementation approaches for each market.

- Financial crime detection tools powered by AI are replacing traditional rule-based systems, offering superior fraud detection in fintech at lower false-positive rates.

- Secure customer onboarding processes that integrate know your customer checks early in the product cycle reduce total compliance cost significantly over the software lifecycle.

- A well-designed compliance management platform not only meets regulatory requirements but also builds lasting customer trust in competitive financial markets.

Every financial platform operating today, whether in Mumbai, Bengaluru, Dubai, or Abu Dhabi, faces one fundamental question before it can serve a single customer: who exactly is this person? That question is the heartbeat of know your customer regulations. With financial fraud prevention becoming more complex and regulators across India and the UAE raising enforcement standards in 2026, financial software teams can no longer treat KYC as an afterthought bolted onto a finished product.

Over our eight-plus years of building regulatory compliance software for financial clients across South Asia and the Gulf, we have seen first-hand what happens when compliance is embedded from the architecture stage versus when it is retrofitted. The difference in cost, time, and legal exposure is enormous. This guide walks through everything your team needs to understand about know your customer rules, why they exist, how they work technically, and what the future looks like for customer identity verification in financial software.

What is Know Your Customer in Financial Software?

Know your customer, commonly referred to as KYC, is the mandatory process through which financial institutions and the software platforms that power them verify the identity of every customer before providing services. In the context of financial software, this means the application itself must be architected to collect, process, verify, and store customer identity data in a way that satisfies both local and international regulatory standards.

KYC is not simply scanning a document. It encompasses the full lifecycle of customer identity, from initial digital identity verification at onboarding, through ongoing risk assessment in banking operations, to periodic re-verification as customer risk profiles evolve. For platforms operating in India and the UAE, this process must align with specific national frameworks while also meeting international standards set by bodies like FATF (Financial Action Task Force).

In practical terms, know your customer in software means building identity authentication processes directly into the product’s user journey, integrating with government ID databases, running real-time document verification systems, and feeding verified data into a broader anti money laundering compliance engine that monitors behaviour over time.

The Core Components of a KYC Process

A robust know your customer framework inside financial software rests on three interconnected components. Understanding each one helps engineering and compliance teams build systems that are both user-friendly and legally defensible.

Why Do These Rules Exist in the First Place?

Know your customer rules emerged from a global recognition that anonymous financial transactions are the backbone of organized financial crime. From drug trafficking networks laundering cash through shell companies to terrorist organizations moving funds through informal channels, the common thread has always been exploiting gaps in identity verification. Governments realized that the most effective way to disrupt these networks was to make anonymity in finance structurally impossible.

In India, the Prevention of Money Laundering Act (PMLA) of 2002 and subsequent RBI guidelines formalized know your customer requirements for all regulated entities. The UAE went further with the UAE Cabinet Decision No. 74 of 2020 on AML/CFT, which aligns closely with FATF Recommendations and applies to all financial institutions including fintech platforms operating in the DIFC and ADGM free zones.

Beyond crime prevention, these rules exist to protect ordinary customers. Financial fraud prevention at scale requires a verified customer base. When platforms know who their users are, they can detect anomalous activity faster, limit damage from account takeovers, and provide better fraud detection in fintech products that genuinely protect users rather than just ticking compliance boxes.

The Legal Backbone Behind KYC Requirements

AML and KYC regulations are not suggestions. They are codified legal obligations enforced by regulatory bodies with significant authority to penalize, investigate, and prosecute. Below is a structured view of the key legal frameworks that financial software teams operating in India and the UAE must understand and build compliance into their systems from the ground up.

| Jurisdiction | Key Regulation | Governing Body | Scope |

|---|---|---|---|

| India | PMLA 2002, RBI KYC Master Direction | RBI, SEBI, IRDAI, FIU-IND | Banks, NBFCs, brokers, insurers, fintechs |

| UAE (Mainland) | Federal Decree Law No. 20 of 2018 | CBUAE, MOEC | All licensed financial institutions |

| UAE (DIFC) | DFSA AML Rulebook | DFSA | DIFC-registered financial services firms |

| International | FATF Recommendations (Updated 2025) | FATF Member States | Cross-border financial operations |

| EU | 6th Anti-Money Laundering Directive | AMLA (from 2025), EBA | EU-regulated financial entities |

How It Protects Financial Software Companies?

Know your customer compliance protects financial software companies on multiple fronts simultaneously. It is not simply about avoiding fines, though those alone can be business-ending. From our experience working with fintech clients scaling across India and the UAE, we have seen how a properly implemented compliance management platform becomes a genuine competitive asset.

Legal Protection

Documented banking compliance requirements shield the company and its directors during audits and regulatory investigations, demonstrating good faith and systematic effort.

Fraud Reduction

Strong online customer verification at the entry point dramatically cuts downstream fraud losses, chargebacks, and account takeover incidents, reducing operational costs significantly.

Customer Trust

Transparent secure customer onboarding processes reassure users that their data and funds are being managed responsibly, improving retention rates and long-term platform loyalty.

What Happens When Financial Software Skips Verification?

The consequences of ignoring know your customer requirements are severe and well-documented. In 2026, regulators globally have made clear that failures in customer identity verification will be treated as governance failures, not administrative oversights. The responsibility now sits explicitly with senior management, not just compliance teams.

Real Consequences of Non-Compliance

Regulatory Fines

Fines can reach hundreds of crores in India or millions of AED in the UAE, and are often accompanied by public disclosure requirements that damage brand value.

License Revocation

Repeated or wilful violations can result in complete withdrawal of operating licenses, effectively shutting down the business with no recourse to continue operations.

Criminal Liability

In both India and the UAE, senior officers of companies found to have wilfully avoided KYC obligations can face personal criminal prosecution and imprisonment.

The global regulatory direction in 2026 reinforces this point strongly. According to a January 2026 analysis of KYC regulatory trends, FATF’s updated guidance explicitly states that technical adherence to requirements is insufficient if it does not result in meaningful risk mitigation, and national regulators are intensifying supervisory engagement accordingly.[1]

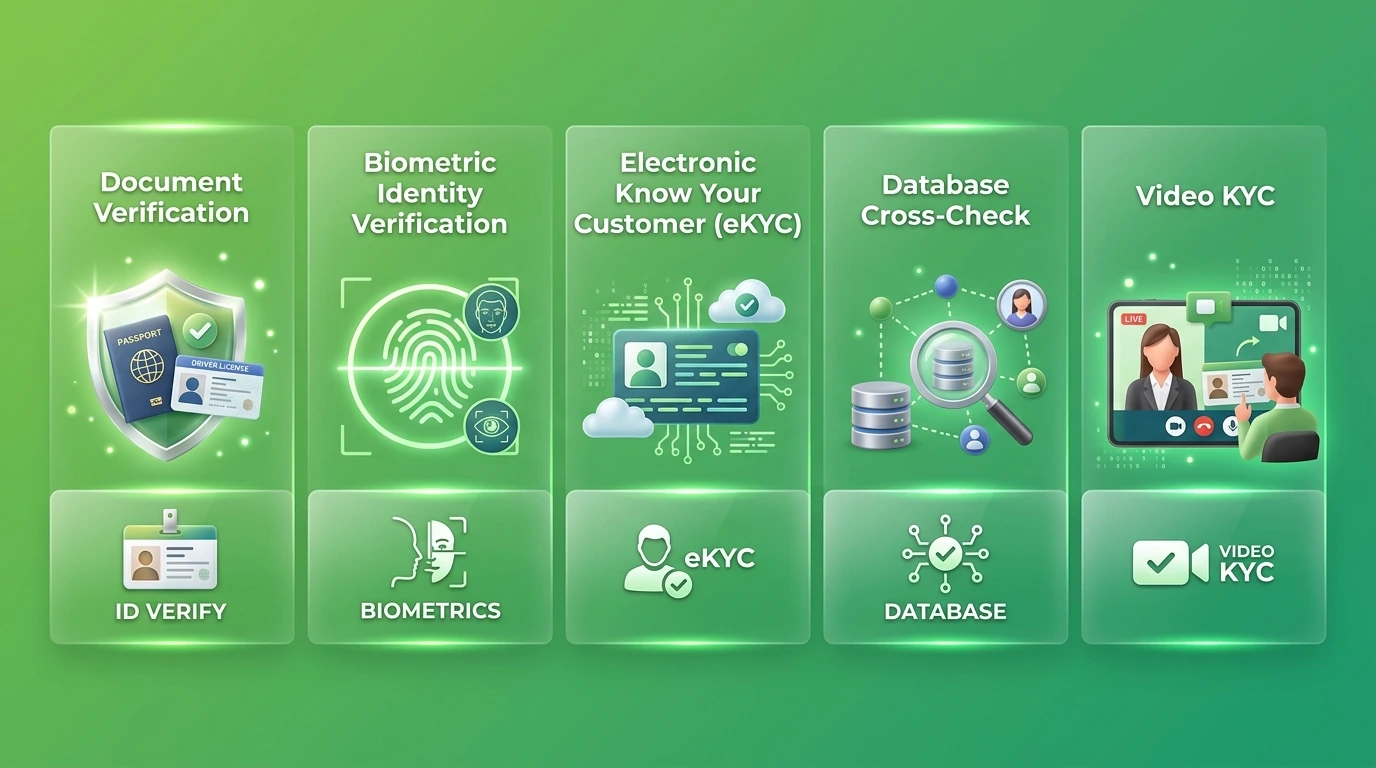

Types of Customer Verification Used in Financial Software

Modern financial software uses a layered approach to customer identity verification. Each type serves a specific purpose and a specific risk level, and they are often combined to create a robust, redundant verification architecture.

| Verification Type | Method | Best For | Risk Coverage |

|---|---|---|---|

| Document Verification | OCR, NFC chip reading, liveness check | All customer types | Low to Medium |

| Biometric Identity Verification | Facial recognition, fingerprint, iris scan | High-value transactions | High |

| Electronic Know Your Customer (eKYC) | Aadhaar OTP, Digi Locker, UAE Pass | Mass digital onboarding | Medium |

| Database Cross-Check | PEP lists, sanctions screening, adverse media | All customers, mandatory | High |

| Video KYC | Live agent or AI-assisted video interview | High-risk or high-value customers | Very High |

How the Verification Process Works Step by Step?

Understanding how know your customer verification flows inside a financial software platform helps teams build processes that are both compliant and frictionless for customers. Here is the end-to-end flow we typically implement for clients requiring secure customer onboarding.

Customer Data Collection

The user provides their name, date of birth, residential address, and a valid government ID. The system stores this in an encrypted format compliant with financial data security standards before any verification begins.

Document Verification System Check

Submitted documents are analysed using OCR and machine learning to detect tampering, expiry, and authenticity markers. For India, this connects to UIDAI for Aadhaar verification; for UAE, it connects to the ICA database through approved channels.

Biometric Liveness and Face Match

Biometric identity verification compares the live selfie or video capture to the photo on the submitted document. Liveness detection algorithms confirm the person is physically present, eliminating spoofing attempts using printed photos or pre-recorded videos.

Sanctions and PEP Screening

The customer’s name and identity data are run against global sanctions lists, Politically Exposed Person (PEP) databases, and adverse media feeds. This is a non-negotiable requirement under AML and KYC regulations for all financial platforms regardless of customer volume.

Risk Assessment and Classification

Risk assessment in banking assigns a risk score to each verified customer based on factors including geography, profession, transaction patterns, and PEP status. High-risk customers are routed to Enhanced Due Diligence workflows; low-risk customers proceed to standard onboarding.

Ongoing Transaction Monitoring

Post-onboarding, transaction monitoring software watches every financial activity for patterns consistent with financial crime detection triggers, such as structuring, sudden large transfers, or activity inconsistent with the declared risk profile. Alerts are reviewed by compliance officers and suspicious activities are reported to FIU or equivalent authorities.

Know Your Customer Rules Every Financial Software Team Must Follow

Across our eight-plus years of building compliance-first financial platforms, we have distilled the non-negotiable know your customer rules that every engineering and product team must bake into their systems from the start, not retrofit later.

Rule 1: Collect Only What Is Legally Required

Banking compliance requirements specify exactly what data must be collected. Over-collection increases financial data security risks and creates liability. Every field in your onboarding form should have a clear legal basis under applicable regulations.

Rule 2: Verify Before Access, Not After

Identity authentication process must be completed before any financial service access is granted. Post-onboarding verification creates windows of unverified access that can be exploited for fraud and create regulatory exposure if discovered during audit.

Rule 3: Risk-Rate Every Customer

Risk assessment in banking must be applied uniformly to all customers. Your compliance management platform should assign and store risk scores at onboarding, update them dynamically as behaviour evolves, and trigger re-verification when thresholds are crossed.

Rule 4: Maintain Complete Audit Trails

Every know your customer action, whether a document check, a PEP scan, or a risk score update, must be logged immutably with timestamps, user IDs, and outcomes. This audit trail is your primary defence during regulatory examination.

Rule 5: Screen Against Sanctions Lists Continuously

Anti money laundering compliance requires not just one-time screening at onboarding, but continuous or periodic rescreening as sanctions lists update. A customer who was clean at onboarding may appear on a sanctions list six months later, requiring immediate action.

Rule 6: Report Suspicious Activity Promptly

Transaction monitoring software must connect directly to a workflow that files Suspicious Transaction Reports (STRs) with FIU-IND in India or the UAE’s Financial Intelligence Unit within mandated timeframes. Delayed reporting is itself a compliance violation.

Common Challenges Financial Software Teams Face

Know your customer implementation in financial software is rarely straightforward. The teams we partner with face a consistent set of obstacles regardless of whether they are building for the Indian market or for UAE financial institutions.

Onboarding Friction vs Compliance Depth

Teams constantly battle between thorough online customer verification and minimizing drop-off rates. Users abandon onboarding if it takes too long, but regulators penalize incomplete customer due diligence. The solution lies in risk-based smart routing, not a one-size-fits-all flow.

Multi-Jurisdiction Regulatory Complexity

A platform serving customers in both India and the UAE must satisfy RBI guidelines, PMLA requirements, CBUAE rules, and DFSA standards simultaneously. Each has different document requirements, data retention rules, and reporting obligations that a single regulatory compliance software layer must reconcile.

Legacy System Integration

Many established financial institutions still operate core banking systems built a decade or more ago. Retrofitting modern digital identity verification and eKYC capabilities onto legacy architecture is technically complex and expensive, often requiring middleware API layers and significant data migration effort.

How Modern Financial Software Makes Compliance Easier?

The right regulatory compliance software transforms know your customer from a burden into a streamlined, automated workflow. Modern platforms now offer capabilities that were technically out of reach even three years ago, fundamentally changing what is possible for teams of any size.

Modern KYC Technology Stack

AI-Powered Document Review

Machine learning models trained on millions of global documents now achieve over 99% accuracy in document verification system checks, far outperforming manual review at a fraction of the cost.

Real-Time eKYC APIs

Electronic Know Your Customer (eKYC) APIs connect in real time to Aadhaar, CKYC registry in India, and UAE Pass in the UAE, enabling sub-30-second customer identity verification without manual document submission.

Behavioral Analytics for AML

Modern transaction monitoring software uses graph analytics and behavioral AI to detect complex financial crime detection patterns across multiple accounts and entities, going far beyond simple rule-based flagging.

Best Practices for Financial Software Building

After working with financial clients ranging from early-stage fintechs to regulated NBFCs and payment gateways across India and the UAE, our team has identified the practices that most reliably lead to know your customer compliance being both effective and operationally efficient.

Design Compliance Into the Architecture From Day One

Regulatory compliance software modules should be part of the initial system design, not added after the product is built. This ensures financial data security, proper data flows, and audit trail generation are structurally embedded rather than surface-level additions that break under load or audit scrutiny.

Use Risk-Based Verification Tiers

Not every customer poses the same risk. Implement tiered know your customer workflows: fast eKYC for low-risk standard users, enhanced biometric identity verification and source-of-funds documentation for higher-risk profiles. This keeps conversion high while maintaining full compliance depth.

Partner With Certified Verification Providers

Use accredited identity authentication process partners that are approved by RBI, UIDAI, or relevant UAE authorities. Building custom verification tools from scratch without regulatory approval creates legal risk, even if the technology works perfectly from a technical standpoint.

Train Your Entire Team, Not Just Compliance Officers

Product managers, engineers, and customer support teams all make decisions that affect anti money laundering compliance and fraud detection in fintech operations. Regular training on what know your customer rules require in practice, not just in theory, dramatically reduces the chance of inadvertent violations.

Conduct Regular Internal KYC Audits

Do not wait for regulators to find gaps. Quarterly internal audits of your know your customer processes, data completeness, and audit trail integrity allow teams to remediate issues before they become regulatory findings. Simulation exercises that mimic regulator review processes are particularly valuable.

The Future of Customer Verification in Financial Software

The evolution of know your customer technology is accelerating. Several forces are reshaping what customer identity verification will look like inside financial platforms over the next three to five years, and teams that understand these shifts now will be far better positioned to adapt their compliance management platform before these changes become regulatory requirements.

The direction of travel is clear. Know your customer will become more intelligent, more integrated, and more automated. Financial software that treats compliance as a first-class architectural concern today will be structurally ready for these changes, while platforms that have bolted on verification as an afterthought will face costly rebuilds to keep pace with both regulatory expectations and customer expectations for seamless, fast secure customer onboarding.

Build KYC-Compliant Financial Software With Confidence

We help fintech teams in India and UAE build AML-ready, know your customer compliant platforms from the ground up. Let us show you how.

Frequently Asked Questions

Q1.1. What does know your customer actually mean in simple terms?

Know your customer (KYC) is the process where financial companies verify who their customers are before offering services. It involves checking identity documents, addresses, and financial backgrounds to prevent fraud, money laundering, and illegal transactions.

Q2.2. Is KYC mandatory for all financial apps and software?

Yes, any software handling financial transactions, lending, payments, or investments must comply with know your customer regulations. Regulators in India, UAE, the US, and the EU require this by law, and ignoring it can lead to heavy fines and operational shutdowns.

Q3.3. How long does the KYC verification process take for a customer?

With modern digital identity verification and eKYC tools, the process can be completed in minutes. Traditional document-based verification may take one to three business days depending on the complexity of the customer’s risk profile and the software used.

Q4.4. What documents are usually needed for KYC in India or UAE?

In India, Aadhaar, PAN card, and passport are commonly accepted. In the UAE, Emirates ID and passport copies are standard. The document verification system matches these against government databases for quick and accurate identity authentication.

Q5.5. Can a fintech startup skip KYC if they are small?

No. Even early-stage fintech companies are required to follow AML and KYC regulations from the day they start onboarding customers. Regulators do not make size-based exceptions, and non-compliance exposes founders and companies to criminal liability.

Q6.6. What is the difference between KYC and AML compliance?

Know your customer is the identity verification step, while anti money laundering compliance is the ongoing monitoring of customer transactions for suspicious activity. KYC feeds into AML, and both are required together under most financial regulations globally.

Q7.7. How does biometric identity verification improve KYC?

Biometric identity verification uses facial recognition, fingerprints, or iris scans to confirm that the person onboarding is genuinely who they claim to be. It reduces document fraud, speeds up secure customer onboarding, and meets the growing requirements of digital-first compliance programs.

Q8.8. What happens if a company fails a KYC audit?

Failures in know your customer audits can result in regulatory fines, license suspension, reputational damage, and in severe cases, criminal charges against company officers. In 2026, regulators in both India and the UAE have increased enforcement activity significantly.

Q9.9. What is eKYC and how is it different from regular KYC?

Electronic Know Your Customer (eKYC) uses digital tools, APIs, and real-time database checks to verify customer identity without physical paperwork. It is faster, scalable, and cost-effective compared to manual verification, and is now preferred by most modern financial platforms.

Q10.10. How often should financial software update its KYC data on customers?

KYC data should be reviewed periodically based on customer risk classification. High-risk customers may require annual reviews while low-risk customers can be reviewed every three to five years. Ongoing transaction monitoring software helps flag changes that trigger early re-verification.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.