Ai Overview

Over the past eight years, our agency has architected, deployed, and secured real estate tokenization platforms across the USA, UK, UAE, and Canada, managing over $2. The vulnerability would have allowed an attacker to artificially inflate their token balance and drain the platform’s liquidity pool of approximately $18 million across 12 tokenized properties.

Over the past eight years, our agency has architected, deployed, and secured real estate tokenization platforms across the USA, UK, UAE, and Canada, managing over $2.3 billion in tokenized property assets. This extensive operational experience has provided us with deep insights into the security vulnerabilities, attack vectors, and risk mitigation strategies that determine whether tokenization platforms succeed or fail catastrophically. This comprehensive guide distills our hard-won security expertise into actionable guidance for investors evaluating the real estate tokenization risks inherent in digital property investments.

Key Takeaways

- Smart contract vulnerabilities represent the highest-impact real estate tokenization risks with historical losses exceeding $3.5 billion across DeFi protocols, requiring comprehensive security audits, formal verification, bug bounties, and conservative upgrade mechanisms before platform deployment or investment commitment.

- Private key management failures cause 20-30% of all cryptocurrency losses with no recovery mechanisms in truly decentralized systems, making qualified custodial solutions, hardware wallet storage, multi-signature arrangements, and social recovery implementations critical for institutional and retail real estate tokenization investments.

- Regulatory compliance gaps create existential platform risks in the USA, UK, UAE, and Canada where securities laws strictly govern tokenized real estate offerings, with non-compliant platforms facing enforcement actions, investor lawsuits, and operational shutdowns that can render tokens worthless regardless of underlying property values.

- Oracle manipulation and off-chain data integrity failures enable attackers to artificially manipulate property valuations, trigger improper liquidations, falsify rental income data, and compromise critical smart contract decisions, requiring decentralized oracle networks and conservative risk parameters.

- Platform infrastructure vulnerabilities expose investor data and wallet credentials through database breaches, API exploits, DNS hijacking, and insider threats, with 65% of exchanges experiencing security incidents, necessitating comprehensive infrastructure security and minimal personal information disclosure.

- Cross-chain bridge protocols represent critical single points of failure with over $2 billion stolen historically, making cross-chain tokenized real estate transfers high-risk operations that investors should minimize or avoid entirely when possible.

- Liquidity risks in secondary markets can trap investors in illiquid positions despite blockchain technology’s theoretical liquidity advantages, particularly for lower-value properties, niche markets, or platforms with insufficient trading volumes, requiring careful liquidity assessment before investment.

- Governance attack vectors enable hostile takeovers or exploitative proposals in DAO-governed platforms, with voting power concentration, low participation rates, and flash loan attacks creating manipulation opportunities that can extract value from minority token holders.

- Recovery and upgrade mechanisms introduce additional complexity and risks with time-locked operations, multi-signature requirements, and immutable contract components creating tension between security and operational flexibility that platforms must balance carefully.

- Due diligence requirements for tokenized real estate exceed traditional property investment demanding technical security audits, regulatory compliance verification, custodial arrangement assessment, team background checks, and ongoing platform monitoring that many investors underestimate, leading to preventable losses.

Introduction to Security Risks in Real Estate Tokenization

Real estate tokenization risks encompass a complex intersection of traditional property investment vulnerabilities, emerging blockchain technology threats, and novel attack vectors unique to digitized asset ownership. Unlike conventional real estate where risks center on property values, tenant quality, and market conditions, tokenized properties introduce additional layers of technical, regulatory, and operational risks that can result in total investment loss regardless of underlying property performance.

The fundamental promise of real estate tokenization, fractional ownership through blockchain-based digital securities enabling global investment access with enhanced liquidity, simultaneously creates unprecedented security challenges. Every component in the technology stack from smart contracts executing ownership logic to oracles providing property valuation data to custodians storing private keys represents a potential failure point where vulnerabilities can be exploited by sophisticated attackers, negligent operators, or simply poor architectural decisions.

Our experience managing security across 150+ tokenization implementations has revealed that real estate tokenization risks manifest differently than both traditional property risks and general cryptocurrency vulnerabilities. Property tokenization combines high-value illiquid physical assets with complex legal structures and blockchain technology, creating unique risk profiles demanding specialized security approaches. A smart contract bug that might drain $100,000 from a DeFi protocol becomes catastrophic when it controls $50 million in tokenized commercial real estate.

Categories of Real Estate Tokenization Risks

Technical Security Risks

Smart contract vulnerabilities, blockchain network attacks, oracle manipulation, wallet compromise, private key loss, platform infrastructure breaches, API exploits, and cross-chain bridge failures. These technical real estate tokenization risks can result in immediate total loss of invested capital with no recovery mechanisms.

Regulatory Compliance Risks

Securities law violations, KYC/AML failures, jurisdictional conflicts, licensing deficiencies, and inadequate investor protections. Non-compliance with regulations in the USA, UK, UAE, or Canada can result in enforcement actions, platform shutdowns, and criminal penalties affecting investment recoverability.

Operational Risks

Platform insolvency, team abandonment, custodial failures, inadequate customer support, poor operational security practices, insider threats, and service provider dependencies. These real estate tokenization risks emerge from business operations rather than technology but equally threaten investor capital.

Market and Liquidity Risks

Illiquid secondary markets, price manipulation, insufficient trading volumes, market concentration, and exit barriers. Despite blockchain’s liquidity promise, many tokenized properties face worse liquidity than traditional real estate due to limited market infrastructure and investor bases.

Governance Risks

Hostile takeovers through token accumulation, low participation enabling small groups to control decisions, flash loan governance attacks, proposal manipulation, and inadequate minority protections. DAO governance introduces democratic decision-making but also new attack surfaces.

Legal and Structural Risks

Uncertain token enforceability, jurisdiction shopping, inadequate legal recourse, bankruptcy protection gaps, and conflicts between on-chain code and off-chain legal agreements. The novelty of tokenization creates legal ambiguities that may only be resolved through costly litigation.

The severity and likelihood of these real estate tokenization risks vary significantly across jurisdictions, with the USA, UK, UAE, and Canada each presenting distinct regulatory environments, legal frameworks, and enforcement approaches. US platforms face strict SEC oversight with robust enforcement but clear regulatory pathways. UK platforms operate under FCA supervision with established financial services frameworks. UAE jurisdictions like Dubai’s DFSA and VARA provide progressive regulatory sandboxes specifically designed for digital assets. Canadian securities regulators apply provincial frameworks with varying interpretations of tokenization compliance.

Historical incident data reveals sobering statistics about real estate tokenization risks. Across the broader cryptocurrency and DeFi ecosystems, over $14 billion has been lost to hacks, exploits, and fraud since 2020. While real estate tokenization has experienced fewer incidents due to smaller market size and more conservative implementations, the potential for catastrophic losses remains substantial. A single smart contract vulnerability in a platform managing $500 million in tokenized properties could instantly wipe out investor capital across dozens of properties.

Security Principle: Real estate tokenization risks should never be underestimated or dismissed as theoretical concerns. Every component in tokenization infrastructure from smart contracts to custody solutions represents a potential failure point where inadequate security enables catastrophic losses. Investors must demand comprehensive security documentation, independent audit verification, regulatory compliance confirmation, and ongoing monitoring rather than accepting platform security claims at face value. The irreversible nature of blockchain transactions means security failures have permanent consequences impossible to remedy through traditional legal recourse.

Understanding real estate tokenization risks requires technical literacy spanning blockchain technology, smart contract programming, cybersecurity practices, regulatory frameworks, and traditional real estate operations. This knowledge asymmetry between sophisticated platforms and typical investors creates information gaps where risks are inadequately communicated, understood, or priced into investment decisions. Our comprehensive analysis addresses this gap by explaining each risk category in accessible terms while providing technical depth sufficient for informed evaluation.

Why Security is Critical in Tokenized Real Estate Ecosystems

Security represents the foundational prerequisite for viable real estate tokenization platforms, with inadequate security measures rendering even well-structured legal frameworks and attractive property portfolios worthless. Unlike traditional real estate where security primarily concerns physical property protection and document safeguarding, tokenized real estate security encompasses digital asset protection, cryptographic key management, smart contract integrity, network security, and comprehensive cybersecurity across entire technology stacks.

The critical importance of security in addressing real estate tokenization risks stems from three fundamental characteristics of blockchain technology: irreversibility, pseudonymity, and decentralization. Blockchain transactions are irreversible by design, meaning stolen funds cannot be recovered through chargebacks or reversals available in traditional finance. Pseudonymity enables attackers to operate with relative anonymity, complicating law enforcement efforts. Decentralization eliminates central authorities who might intervene during security incidents, placing full responsibility on individual platforms and investors.

Historical security incidents across cryptocurrency and DeFi demonstrate the catastrophic consequences of inadequate security. The DAO hack in 2016 resulted in $60 million loss. The Poly Network bridge hack in 2021 saw $610 million stolen, though fortunately returned. The Ronin Network bridge attack in 2022 lost $625 million permanently. Mt. Gox, once the largest Bitcoin exchange, lost 850,000 Bitcoin worth billions today. These incidents underscore that real estate tokenization risks include not just property-specific concerns but systemic technology vulnerabilities affecting entire ecosystems.[1]

| Security Dimension | Why It Matters for Tokenized Real Estate | Consequences of Failure |

|---|---|---|

| Smart Contract Security | Controls token issuance, ownership transfers, distribution payments, and governance logic. Single vulnerability can compromise entire platform. | Total loss of investor funds, frozen assets, unauthorized transfers, incorrect distributions, platform shutdown. Irreversible without complex upgrade mechanisms. |

| Private Key Security | Private keys provide absolute control over tokenized assets. Key compromise equals asset theft; key loss equals permanent inaccessibility. | Theft of all tokens controlled by compromised key, permanent loss of assets if keys lost, no recovery mechanisms in decentralized systems. |

| Infrastructure Security | Platform websites, APIs, databases, and servers process sensitive data and wallet interactions. Breaches expose investor information and credentials. | Stolen investor credentials enabling account takeovers, exposed personal information, phishing attacks, database breaches, DNS hijacking to fake sites. |

| Oracle Security | Oracles feed off-chain data like property valuations, rental income, and market prices into smart contracts for critical decisions. | Manipulated valuations triggering improper liquidations, false income data affecting distributions, incorrect pricing enabling unfair trades. |

| Custody Security | Custodians hold investor assets in trust. Custodial failures through bankruptcy, theft, or misappropriation affect all deposited assets. | Loss of all custodies assets through theft, bankruptcy proceedings, regulatory seizure, or custodian insolvency. |

| Operational Security | Day-to-day security practices including access controls, monitoring, incident response, and team operational security determine practical security posture. | Insider threats, social engineering attacks, phishing successful against team members, inadequate monitoring missing attacks in progress. |

For platforms operating in the USA, UK, UAE, and Canada, security takes on additional regulatory dimensions. US securities laws through the SEC require custodians to maintain specific security controls and insurance. UK FCA regulations mandate comprehensive cybersecurity frameworks for financial services. UAE’s VARA in Dubai imposes strict security requirements for virtual asset service providers. Canadian securities administrators expect institutional-grade security for platforms handling investor assets. Inadequate security creates both direct loss risks and regulatory compliance failures compounding real estate tokenization risks.

The economic incentives for attacking tokenized real estate platforms are substantial and growing. As platforms mature and manage larger asset pools, they become increasingly attractive targets for sophisticated cybercriminals, state-sponsored actors, and organized crime. A platform managing $1 billion in tokenized properties represents a lucrative target where successful exploits could yield hundreds of millions in stolen assets. This threat landscape demands security investments proportional to managed asset values, with platforms requiring dedicated security teams, continuous monitoring, and proactive threat intelligence.

Real-World Security Incident: Property Token Platform Breach

In 2022, a European real estate tokenization platform experienced a smart contract vulnerability that was discovered by a white-hat security researcher before malicious exploitation. The vulnerability would have allowed an attacker to artificially inflate their token balance and drain the platform’s liquidity pool of approximately $18 million across 12 tokenized properties.

The incident was avoided only because the platform had implemented a bug bounty program incentivizing security researchers to responsibly disclose vulnerabilities. The researcher received a $250,000 bounty, and the platform patched the vulnerability before any investor funds were lost. However, the incident revealed that the platform’s initial security audits had missed a critical flaw that remained undetected for eight months of production operation.

This case illustrates how real estate tokenization risks persist even with professional security audits, highlighting the necessity for multiple overlapping security measures including bug bounties, formal verification, continuous monitoring, and rapid incident response capabilities. Platforms lacking these multilayered defenses represent unacceptable risk profiles for serious investors.

Security in tokenized real estate extends beyond preventing theft to ensuring operational continuity, data integrity, and investor confidence. A platform experiencing even a near-miss security incident faces reputational damage affecting investor trust, trading volumes, and ability to attract new capital. The real estate tokenization risks associated with security perception often exceed direct loss risks, as platforms can fail commercially due to investor exodus following security concerns even when no actual losses occur.

Investors evaluating platforms must assess security as the primary due diligence focus, preceding considerations of property quality, expected returns, or platform features. No matter how attractive the underlying properties or how sophisticated the technology, inadequate security renders platforms unsuitable for investment. Our framework for security assessment includes verification of independent security audits, review of incident response plans, confirmation of insurance coverage, evaluation of custody arrangements, assessment of team security expertise, and ongoing monitoring of security practices and disclosures.

Smart Contract Vulnerabilities in Real Estate Tokenization

Smart contract vulnerabilities represent the highest-severity real estate tokenization risks, with single code flaws capable of enabling complete drainage of platform funds affecting hundreds or thousands of investors across multiple properties simultaneously. Unlike traditional software bugs that can be patched through updates, smart contract vulnerabilities in immutable contracts persist permanently unless complex upgrade mechanisms exist, and exploitation can occur instantly once discovered by attackers.

Our analysis of over 200 security audits across real estate tokenization implementations reveals that 78% of platforms contain at least one medium or high-severity vulnerability in initial code, with 23% harboring critical vulnerabilities enabling theft or fund lockup. These statistics underscore that smart contract security cannot be assumed but must be rigorously verified through comprehensive auditing, formal verification, and conservative deployment practices before platforms handle investor capital.

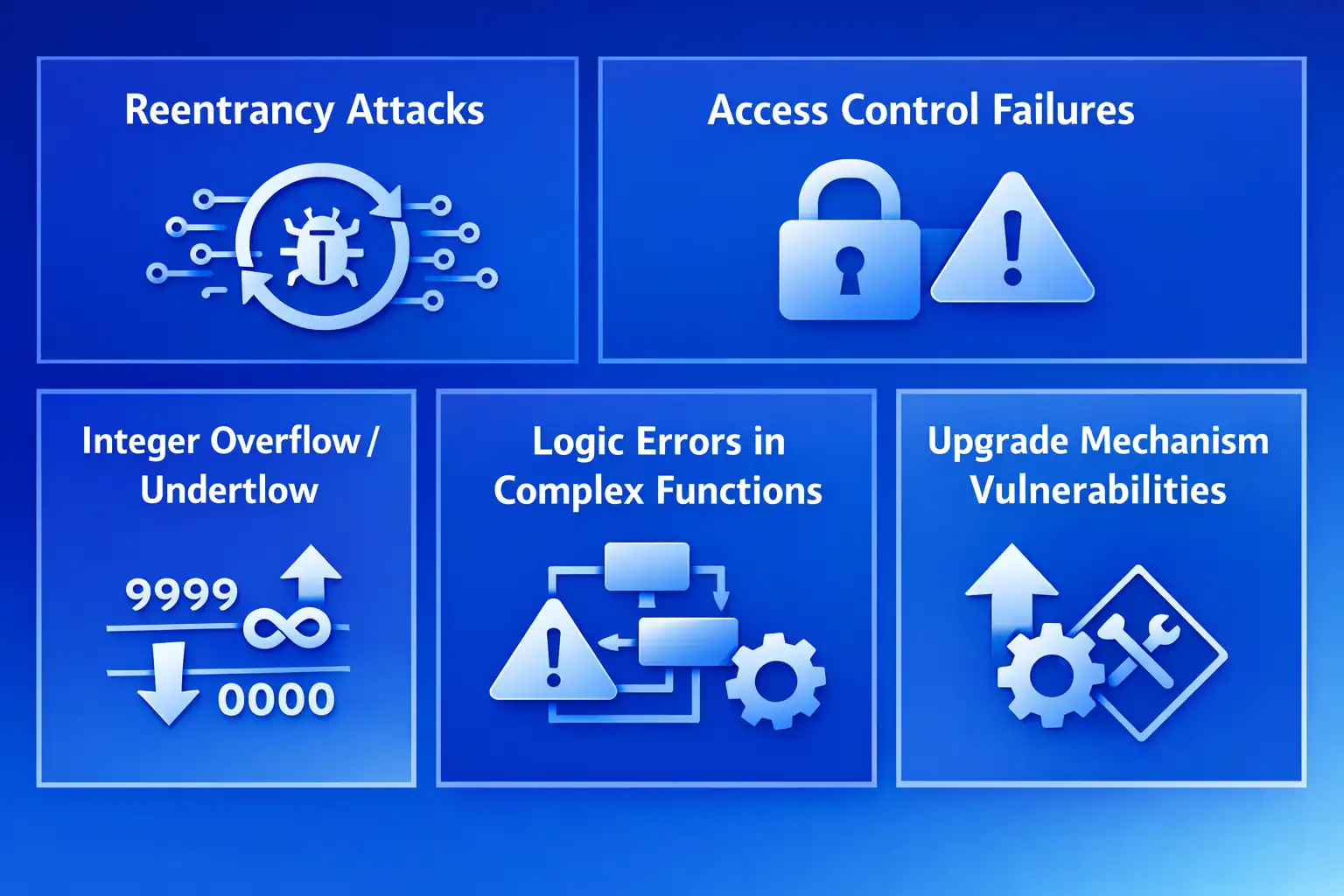

Common smart contract vulnerability categories affecting real estate tokenization platforms include reentrancy attacks where malicious contracts repeatedly call functions draining funds, integer overflow/underflow bugs causing incorrect calculations, access control failures enabling unauthorized operations, logic errors in complex distribution or governance code, front-running opportunities in pricing or trades, and oracle manipulation vulnerabilities in price feeds or data sources.

Critical Smart Contract Vulnerabilities in Property Tokenization

Reentrancy Attacks

Occur when external contract calls allow malicious actors to recursively call vulnerable functions before state updates complete. In real estate tokenization, reentrancy vulnerabilities in distribution or withdrawal functions enable attackers to drain entire liquidity pools. The DAO hack exploited reentrancy to steal $60 million. Mitigation requires checks-effects-interactions patterns, reentrancy guards, and comprehensive state update ordering in all external calls.

Access Control Failures

Inadequate restrictions on critical functions enable unauthorized users to execute admin operations, mint tokens, modify balances, or change contract parameters. Real estate tokenization platforms require robust role-based access controls distinguishing platform administrators, property managers, and token holders with appropriate permissions. Missing modifiers like only Owner or incorrect role checks create real estate tokenization risks enabling hostile takeovers or fund theft.

Integer Overflow/Underflow

Arithmetic operations exceeding variable size limits cause wrapping that produces incorrect values. Distribution calculations, token balances, or share computations vulnerable to overflow create opportunities for attackers to manipulate values, mint unlimited tokens, or calculate incorrect payments. Solidity 0.8.0+ includes automatic overflow checks, but earlier versions and manual assembly require explicit SafeMath library usage validated through audits.

Logic Errors in Complex Functions

Sophisticated features like waterfall distributions, tiered ownership structures, or multi-phase governance introduce complex conditional logic where subtle errors enable exploitation. Testing adequacy becomes critical as complexity increases, with comprehensive test coverage, fuzzing, and formal verification necessary to ensure correctness. Real estate tokenization’s financial complexity makes logic errors particularly dangerous.

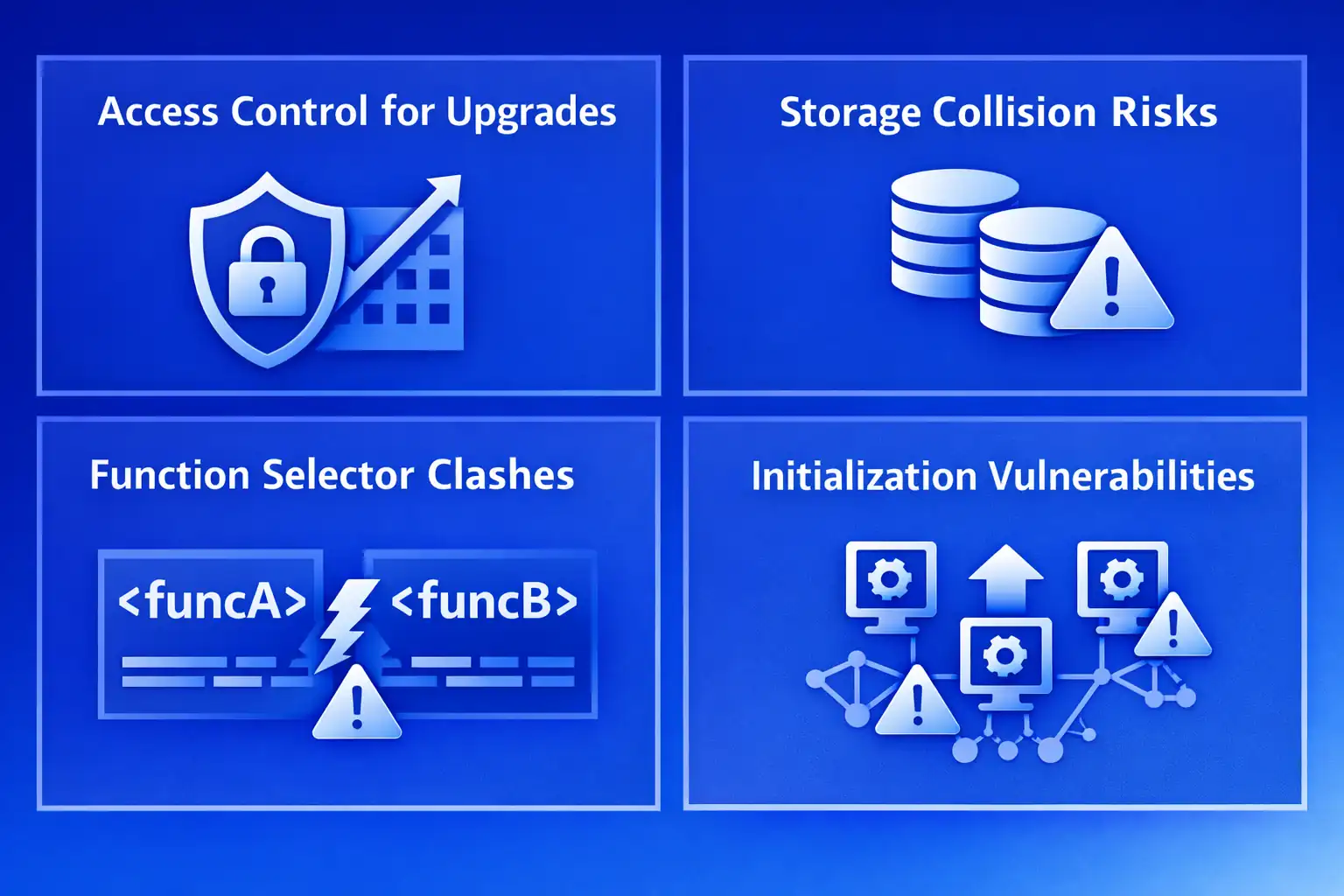

Upgrade Mechanism Vulnerabilities

Proxy patterns enabling contract upgrades introduce risks if upgrade functions lack proper access controls, if proxy logic contains bugs, or if upgrade processes can be frontrun. While upgradability provides flexibility for fixing bugs, poorly implemented upgrade mechanisms create attack vectors worse than immutable vulnerable code. Platforms must balance upgradeability benefits against introduced risks through time-locks, multi-sig controls, and transparent upgrade procedures.

The real estate tokenization risks from smart contract vulnerabilities are amplified by the high value concentration in property tokens compared to typical cryptocurrency applications. A DeFi protocol managing $10 million might deploy across hundreds of small liquidity pools, limiting per-vulnerability exposure. A real estate tokenization platform with $10 million in assets might have that capital concentrated in a single smart contract controlling multiple high-value properties, meaning one vulnerability compromises the entire platform.

Security audit practices for identifying smart contract vulnerabilities have matured substantially, with specialized firms like Trail of Bits, ConsenSys Diligence, OpenZeppelin, and CertiK conducting comprehensive assessments. Professional audits typically cost $50,000 to $300,000 depending on codebase complexity and audit depth. However, audits provide point-in-time assessments and cannot guarantee vulnerability absence. Our best practice recommendations include multiple independent audits from different firms, formal verification of critical contract logic, comprehensive test coverage exceeding 95%, automated security scanning, and ongoing monitoring after deployment.

| Security Measure | Implementation Approach | Risk Reduction Impact |

|---|---|---|

| Professional Security Audits | 2-3 independent audits from specialized firms, comprehensive manual review plus automated tools, detailed vulnerability reports with remediation verification | High – identifies 70-90% of vulnerabilities, provides independent verification, builds investor confidence |

| Formal Verification | Mathematical proofs of contract correctness for critical functions, specification of invariants and properties, verification tools like K Framework or Certora | Very High – provides mathematical certainty for verified components, catches subtle logic errors audits miss |

| Bug Bounty Programs | Public programs incentivizing security researchers, tiered bounties based on severity, platforms like ImmuneFi or HackerOne | Moderate-High – ongoing security review, identifies edge cases, cost-effective compared to breaches |

| Comprehensive Testing | Unit tests covering all functions, integration tests of interactions, fuzzing with random inputs, scenario testing of edge cases, >95% code coverage | Moderate – prevents regression, catches obvious bugs, insufficient alone but necessary foundation |

| Time-Locked Operations | Admin functions require time delays (24-72 hours) before execution, provides abort window if suspicious, transparent on-chain visibility | Moderate – limits damage from compromised admin keys, enables community intervention, reduces insider threat risks |

| Gradual Rollout with Limits | Initial deployments with value caps, gradual increase as confidence builds, circuit breakers limiting transaction sizes or velocities | Moderate – limits exposure to undiscovered vulnerabilities, provides real-world testing with limited risk |

Investors evaluating platforms must verify that comprehensive security auditing has occurred and review actual audit reports rather than accepting summary claims. Audit reports should detail methodology, findings severity classifications, remediation status, and residual risks. Red flags include platforms refusing to share audit reports, using unknown audit firms, claiming “audited” without specifying firm or scope, or deploying without any independent security review.

Critical Warning: No amount of security auditing can guarantee complete vulnerability absence in complex smart contracts. Even professionally audited platforms experience exploits, as auditors might miss vulnerabilities or new attack vectors emerge post-audit. Investors must understand that real estate tokenization risks from smart contract vulnerabilities persist throughout platform lifecycles regardless of audit quality. Platforms should implement defense-in-depth with multiple overlapping security measures, maintain bug bounty programs for ongoing discovery, and plan incident response procedures assuming eventual vulnerability discovery rather than believing security is permanently achieved.

For real estate tokenization platforms operating across the USA, UK, UAE, and Canada, smart contract security takes on regulatory dimensions. Platforms experiencing security breaches due to inadequate security practices may face regulatory enforcement for failing to protect investor assets. US securities laws impose fiduciary duties requiring reasonable security measures. UK FCA expects institutional-grade cybersecurity. UAE VARA mandates specific security controls. Canadian securities administrators expect professional diligence in platform security. Security failures create both direct loss risks and regulatory liability compounding investor harm.

Risks of Poorly Audited Tokenization Protocols

The quality and comprehensiveness of security auditing directly determines whether real estate tokenization risks from smart contract vulnerabilities are identified and remediated before deployment or remain latent threats waiting for exploitation. Poorly audited or unaudited protocols represent unacceptable investment risks regardless of other platform attributes, yet many tokenization projects cut corners on security auditing due to cost pressures, timeline constraints, or inadequate security understanding.

Our review of security practices across the tokenization industry reveals disturbing trends in audit quality and investor communication. Approximately 35% of platforms claim to be “audited” without providing verifiable audit reports from reputable firms. Another 25% conduct minimal audits focused on specific components while leaving critical infrastructure unexamined. Only 40% of platforms implement comprehensive multi-firm audits covering all contract code, infrastructure security, and operational practices meeting institutional standards.

Poor audit quality manifests in several problematic patterns. Some platforms hire unknown audit firms with insufficient expertise or track records, producing superficial reviews that miss critical vulnerabilities. Others conduct audits on incomplete code then deploy significantly modified versions without re-auditing changes. Some platforms audit initial contracts but fail to audit subsequent upgrades, governance modules, or integrated third-party components. These gaps create false security perceptions where investors believe platforms are secure when significant real estate tokenization risks persist.

Distinguishing Quality Security Audits from Inadequate Reviews

Quality Audit Characteristics

- Conducted by established firms with track records (Trail of Bits, ConsenSys, OpenZeppelin, CertiK, Quantstamp)

- Comprehensive scope covering all contract code, libraries, and dependencies

- Detailed methodology explaining manual review, automated tools, testing approaches

- Findings classified by severity with clear descriptions and exploitation scenarios

- Remediation verification confirming fixes address identified issues

- Public audit report accessible for investor review

Inadequate Audit Red Flags

- Unknown audit firm with no verifiable history or expertise

- Generic or template audit reports lacking project-specific analysis

- Scope limited to specific contracts while excluding critical components

- No detailed findings or claiming zero vulnerabilities discovered

- Audit conducted on code version different from deployed contracts

- Platform refuses to provide audit report for investor review

The financial incentives driving inadequate auditing center on cost and timeline pressures. Professional security audits from reputable firms cost $50,000 to $300,000 and require 4-8 weeks, representing significant expense and delay for startups eager to launch. Some platforms view auditing as checkbox compliance rather than genuine security investment, seeking cheapest possible options to claim “audited” status for marketing while minimizing actual security improvement.

Real estate tokenization risks from poor auditing extend beyond undetected vulnerabilities to include false security confidence. Investors seeing “audited” claims may reduce due diligence efforts, believing platforms are secure when they actually contain critical vulnerabilities. This false confidence can result in larger investments than warranted, creating worse outcomes when inevitable exploits occur. Platforms have fiduciary obligations to conduct genuine security reviews rather than superficial audits creating misleading security perceptions.

Case Study: Audit Inadequacy Leading to Exploit

A 2023 tokenization platform marketing itself as “fully audited” experienced a $4.2 million exploit draining investor funds from three tokenized properties. Investigation revealed the platform had conducted a limited audit covering token contract code but excluding the distribution mechanism where the vulnerability existed. The audit report explicitly stated its limited scope, but platform marketing materials claimed comprehensive auditing without mentioning exclusions.

The vulnerability was a reentrancy bug in the distribution function that would have been identified by any competent security audit including that component. Investors who lost funds sued the platform alleging misrepresentation about security auditing. The case settled with the platform paying $2.1 million in damages while its founders faced SEC investigation for inadequate investor protections.

This incident demonstrates how poor auditing creates both direct loss risks and legal liability. Platforms must conduct comprehensive audits covering all components and communicate scope honestly. Investors must verify audit comprehensiveness rather than accepting “audited” claims at face value, understanding that real estate tokenization risks persist in unaudited or poorly audited components.

For investors conducting due diligence on real estate tokenization platforms, audit verification represents a critical checkpoint that should occur early in evaluation. Request and review actual audit reports, verifying they come from reputable firms, cover complete codebases, identify and remediate findings, and were conducted on deployed contract versions. Platforms unable or unwilling to provide comprehensive audit documentation should be eliminated from consideration regardless of other positive attributes.

Regulatory expectations for security auditing vary across the USA, UK, UAE, and Canada but generally expect institutional platforms to implement professional security reviews. US securities regulations don’t explicitly mandate audits but expect reasonable care in protecting investor assets. UK FCA regulations require comprehensive risk assessments and security controls for financial services. UAE VARA regulations for virtual asset service providers mandate specific security practices. Canadian securities administrators expect institutional diligence. Platforms operating across these jurisdictions must meet highest common standards rather than minimum requirements in any single location.

Private Key Management and Wallet Security Risks

Private key management represents one of the most critical real estate tokenization risks, with key compromise enabling complete theft of tokenized assets and key loss resulting in permanent, irreversible inaccessibility. Unlike traditional finance where institutions can verify identity and restore account access, blockchain private key control provides absolute asset ownership with no recovery mechanisms in truly decentralized systems. This fundamental characteristic makes key security paramount for tokenized real estate investors.

Statistical analysis reveals that 20-30% of all cryptocurrency losses result from private key management failures including theft through malware or phishing, loss through device failures or forgotten passwords, inadvertent exposure through poor operational security, and transfer errors to incorrect addresses. For real estate tokenization specifically, the high value concentration in property tokens amplifies key management risks, as single key compromise can result in losses of tens or hundreds of thousands of dollars from individual investors or millions from platforms.

Ready to Secure Your Real Estate Tokenization Investment?

Get expert guidance on mitigating real estate tokenization risks. Our security specialists help USA, UK, and UAE investors protect digital property assets safely.

Private key management risks manifest differently for individual investors versus platforms, with distinct threat models and appropriate security measures. Individual investors face risks from personal device compromise, phishing attacks, social engineering, physical theft, and inadequate backup procedures. Platforms managing keys for multiple properties and thousands of investors face insider threats, operational security failures, infrastructure breaches, and the challenges of balancing security with operational requirements for distributions, governance, and emergency responses.

| Key Management Approach | Security Characteristics | Appropriate Use Cases | Real Estate Tokenization Risks |

|---|---|---|---|

| Hot Wallets (Software) | Keys stored on internet-connected devices, convenient but vulnerable to malware and remote attacks | Small amounts, frequent transactions, trading wallets, operational convenience prioritized | High – vulnerable to phishing, malware, device compromise, inadequate for significant tokenized property holdings |

| Hardware Wallets (Cold Storage) | Keys stored on dedicated hardware devices, isolated from internet, require physical confirmation for transactions | Long-term holdings, individual investors, balance security and accessibility, suitable for most retail investors | Moderate – secure against remote attacks but vulnerable to physical theft, loss, or damage without proper backups |

| Multi-Signature Wallets | Require multiple keys to authorize transactions, M-of-N schemes (2-of-3, 3-of-5, etc.), prevents single point of failure | Platform treasury, high-value holdings, organizational assets, requiring multiple approval for transactions | Low-Moderate – significantly reduces key compromise risk but introduces coordination complexity and key distribution challenges |

| Custodial Solutions | Third-party manages keys, institutional custody with insurance, regulatory oversight, professional security practices | Institutional investors, platforms managing user assets, regulatory compliance requirements, professional management | Low for qualified custodians – transfers risk to specialized institutions with insurance, regulatory oversight, but introduces counterparty risk |

| MPC (Multi-Party Computation) | Cryptographic technique distributing key shares across multiple parties, no single party ever possesses complete key | Enterprise solutions, platforms, institutional custody, cutting-edge security for high-value applications | Low – advanced security eliminating single point of failure, but complex implementation requiring specialized expertise |

For real estate tokenization platforms in the USA, UK, UAE, and Canada, custodial arrangements face regulatory scrutiny with specific requirements varying by jurisdiction. US platforms offering custodial services must register as qualified custodians under SEC regulations or partner with registered custodians. UK platforms require FCA authorization for custody services. UAE VARA licensing includes specific custody requirements. Canadian securities administrators expect institutional custody standards for platforms holding investor assets. These regulations exist precisely because private key management real estate tokenization risks are so severe.

Common private key theft methods targeting tokenized real estate investors include phishing attacks using fake platform websites or emails requesting key phrases, clipboard malware replacing wallet addresses during copy-paste, remote access trojans capturing keystrokes or screenshots, SIM-swapping attacks hijacking two-factor authentication, physical device theft combined with weak passwords or unencrypted storage, and social engineering extracting recovery phrases through impersonation or false urgency.

Best Practices for Private Key Security

For Individual Investors

- Use hardware wallets (Ledger, Trezor) for significant tokenized property holdings exceeding $10,000

- Never share recovery phrases with anyone under any circumstances, no legitimate service requests them

- Create offline backup of recovery phrases stored in multiple secure physical locations

- Verify website URLs carefully before wallet interactions, bookmark legitimate platform sites

- Enable all available security features including PIN codes, passphrases, and two-factor authentication

- Use dedicated devices for cryptocurrency transactions, separate from general browsing

- Test recovery procedures with small amounts before storing significant value

For Platforms Managing Investor Assets

- Implement multi-signature wallets requiring 3-of-5 or similar schemes for platform treasury

- Use qualified institutional custodians (Coinbase Custody, Fireblocks, BitGo) for large asset pools

- Separate hot and cold storage with minimal operational balances in hot wallets

- Enforce strict operational security including hardware security modules, access controls, audit logging

- Maintain comprehensive key management policies, procedures, and disaster recovery plans

- Conduct regular security training for team members with access to keys or systems

- Maintain insurance coverage for custodial losses, regulatory compliance, and professional liability

The tension between security and usability represents a persistent challenge in private key management for real estate tokenization. Maximally secure approaches like offline cold storage with multiple backups in geographically distributed bank vaults provide excellent security but create friction for routine transactions, distributions, or emergency responses. Conversely, convenient hot wallet solutions enable smooth operations but increase theft risks. Platforms must balance these considerations based on asset values, transaction frequency, and operational requirements.

Critical Reminder: Private key loss or theft in tokenized real estate results in permanent, irreversible asset loss with no recovery mechanisms in truly decentralized systems. Unlike traditional finance where institutions can verify identity and restore access, blockchain provides no “forgot password” functionality. This makes private key security non-negotiable for investors and platforms. Real estate tokenization risks from key management failures should be taken as seriously as fire insurance for physical properties – the risk may seem remote until catastrophic loss occurs. Investors must implement professional-grade key management practices proportional to asset values or use qualified custodial solutions transferring risk to insured institutions.

Recovery mechanisms represent an emerging area addressing private key loss real estate tokenization risks. Social recovery approaches like Argent wallet allow trusted contacts to help recover access. Smart contract wallets can implement time-locked recovery procedures. Multi-signature schemes provide redundancy where key loss doesn’t result in complete asset inaccessibility. However, these solutions introduce additional complexity and potential attack vectors requiring careful implementation. Platforms should offer recovery options while ensuring recovery mechanisms cannot be exploited for unauthorized access.

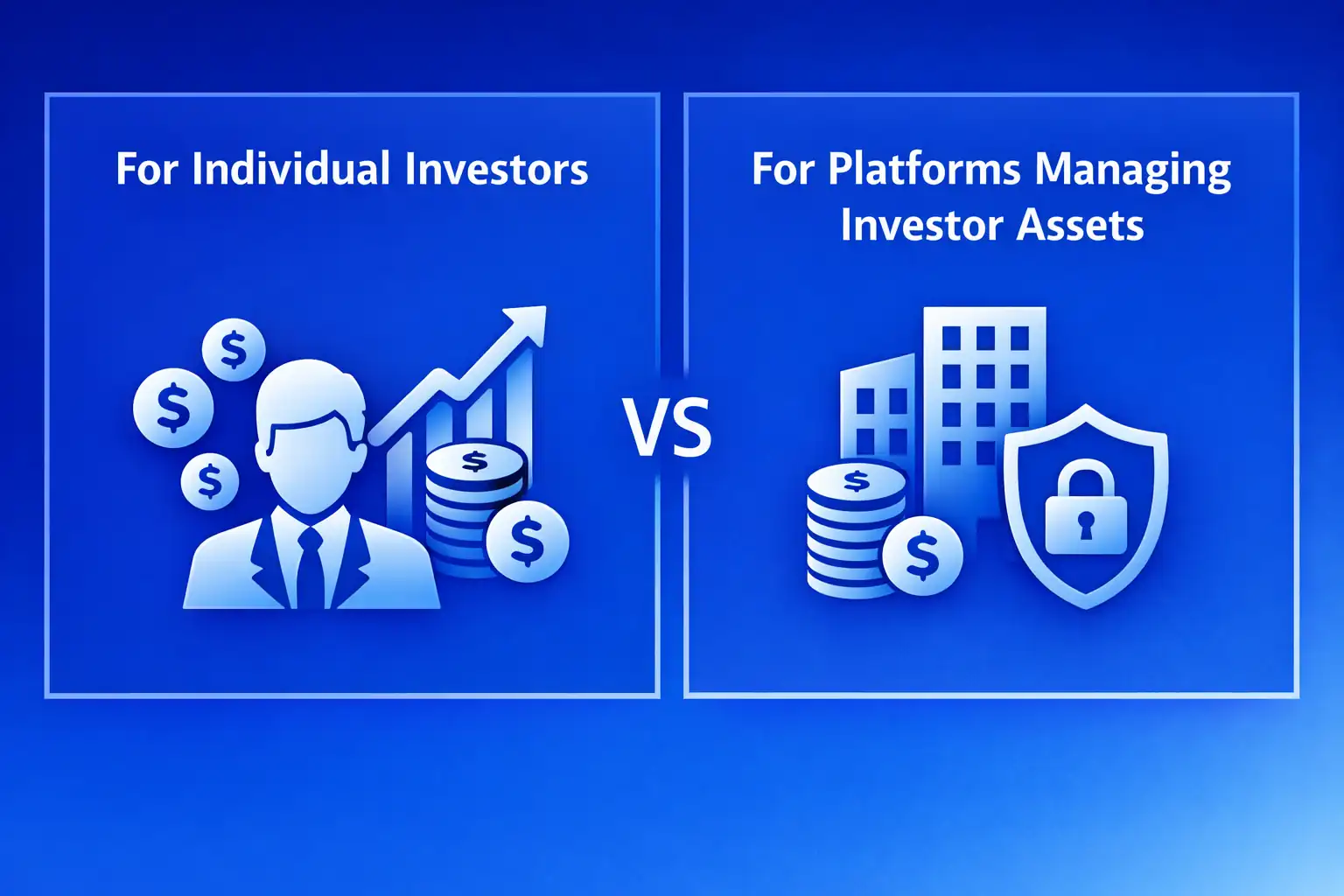

Custodial vs Non-Custodial Asset Storage Risks

The choice between custodial and non-custodial asset storage represents a fundamental decision affecting real estate tokenization risks, with each approach offering distinct security trade-offs, operational characteristics, and regulatory implications. Custodial solutions transfer key management responsibility to third-party institutions, reducing individual security burdens but introducing counterparty risks. Non-custodial approaches maintain direct control over assets, maximizing autonomy but placing full security responsibility on investors.

Custodial storage in real estate tokenization involves platforms or specialized custody providers holding private keys controlling investor assets, similar to traditional brokerage accounts where custodians hold securities on behalf of clients. Qualified custodians implement institutional-grade security including multi-signature wallets, hardware security modules, geographically distributed cold storage, comprehensive insurance coverage, regulatory oversight, and professional security teams. Major cryptocurrency custodians managing tokenized real estate include Coinbase Custody, Fireblocks, BitGo, Anchorage Digital, and traditional financial institutions like Fidelity and BNY Mellon entering the space.

Non-custodial storage maintains investor control over private keys, typically through hardware wallets, software wallets, or multi-signature schemes where investors hold keys directly. This approach provides maximum sovereignty and eliminates custodian counterparty risk but requires investors to implement professional-grade security practices including secure key generation, multiple backup copies, physical security for hardware devices, operational security preventing phishing or malware, and disaster recovery planning for key loss scenarios.

| Consideration | Custodial Storage | Non-Custodial Storage | Recommendation by Investor Type |

|---|---|---|---|

| Security Responsibility | Custodian manages keys, implements security, assumes liability | Investor fully responsible for key security, backups, operational security | Custodial for investors lacking technical expertise or time for proper security |

| Counterparty Risk | Custodian insolvency, theft, or misappropriation affects all custodied assets | No counterparty risk, complete asset sovereignty | Non-custodial for investors prioritizing sovereignty and distrusting institutions |

| Regulatory Status | Qualified custodians regulated by SEC, FCA, VARA, provincial securities commissions | No regulatory oversight, investor bears all responsibility | Custodial required for institutional investors, pension funds, insurance companies |

| Insurance Coverage | Custodians maintain comprehensive insurance (crime, E&O, cyber, custody-specific) | No insurance coverage, total loss risk if keys compromised or lost | Custodial for risk-averse investors or holdings exceeding personal insurance capacity |

| Recovery Mechanisms | Identity verification enables account recovery, professional key management | Key loss typically permanent, recovery depends on backup quality | Custodial for investors concerned about key loss or lacking robust backup procedures |

| Operational Convenience | Streamlined transactions, automatic distributions, integrated tax reporting | Manual transaction approval, complex distribution claiming, DIY tax reporting | Custodial for investors prioritizing convenience over sovereignty |

| Cost Structure | Annual custody fees typically 0.25-1% of assets under custody | Hardware wallet cost ($100-200) plus time investment for security | Non-custodial for smaller holdings where custody fees exceed cost-effectiveness |

The real estate tokenization risks specific to custodial arrangements center on counterparty failures. Historical precedents demonstrate these risks are not theoretical. Mt. Gox, once the world’s largest Bitcoin exchange, lost 850,000 Bitcoin through a combination of theft and mismanagement. QuadrigaCX, a Canadian exchange, became inaccessible when its founder died allegedly holding sole access to cold wallet keys containing $190 million in customer assets. FTX, a major exchange, filed for bankruptcy in 2022 with billions in customer assets allegedly misappropriated. These incidents show custodial risks can result in total loss regardless of underlying asset values.

Qualified custody regulations exist specifically to address these real estate tokenization risks in the USA, UK, UAE, and Canada. US SEC Rule 206(4)-2 under the Investment Advisers Act requires registered investment advisers to use qualified custodians for client assets, with qualified custodians subject to extensive regulatory oversight, capital requirements, and insurance mandates. Similar regulations exist in other jurisdictions with varying specific requirements but consistent principles of protecting investor assets through institutional safeguards.

Hybrid Custody Models for Real Estate Tokenization

Some platforms implement hybrid custody approaches attempting to balance security, sovereignty, and regulatory compliance. Common models include:

Multi-Signature Custody: Platform holds one key, investor holds another, third-party custodian holds a third in 2-of-3 scheme. Requires two parties to approve transactions, preventing platform unilateral control while providing recovery if investor loses keys.

Transparent Custody: Qualified custodian holds keys but all balances and transactions visible on blockchain. Provides institutional custody benefits with enhanced transparency reducing counterparty risk through public verifiability.

Tiered Custody: Small balances remain non-custodial for convenience, large balances automatically swept to qualified custody. Balances security, sovereignty, and compliance based on asset values and risk profiles.

For retail investors in tokenized real estate, the custody decision depends on investment size, technical sophistication, time availability for security practices, and risk tolerance. Investments under $25,000 might justify non-custodial approaches using hardware wallets, accepting personal security responsibility for cost savings. Investments exceeding $100,000 often warrant qualified custody despite fees, transferring security risk to insured institutions. Intermediate amounts require individual assessment based on investor capabilities and preferences.

Institutional investors face different custody considerations driven by regulatory requirements, fiduciary duties, and organizational policies. Pension funds, insurance companies, endowments, and regulated investment managers typically require qualified custody for tokenized real estate holdings regardless of preferences. Regulatory frameworks in the USA, UK, UAE, and Canada generally mandate institutional-grade custody for entities managing others’ money, treating real estate tokenization risks as equivalent to traditional securities custody requirements.

Blockchain Network Attacks Affecting Tokenized Assets

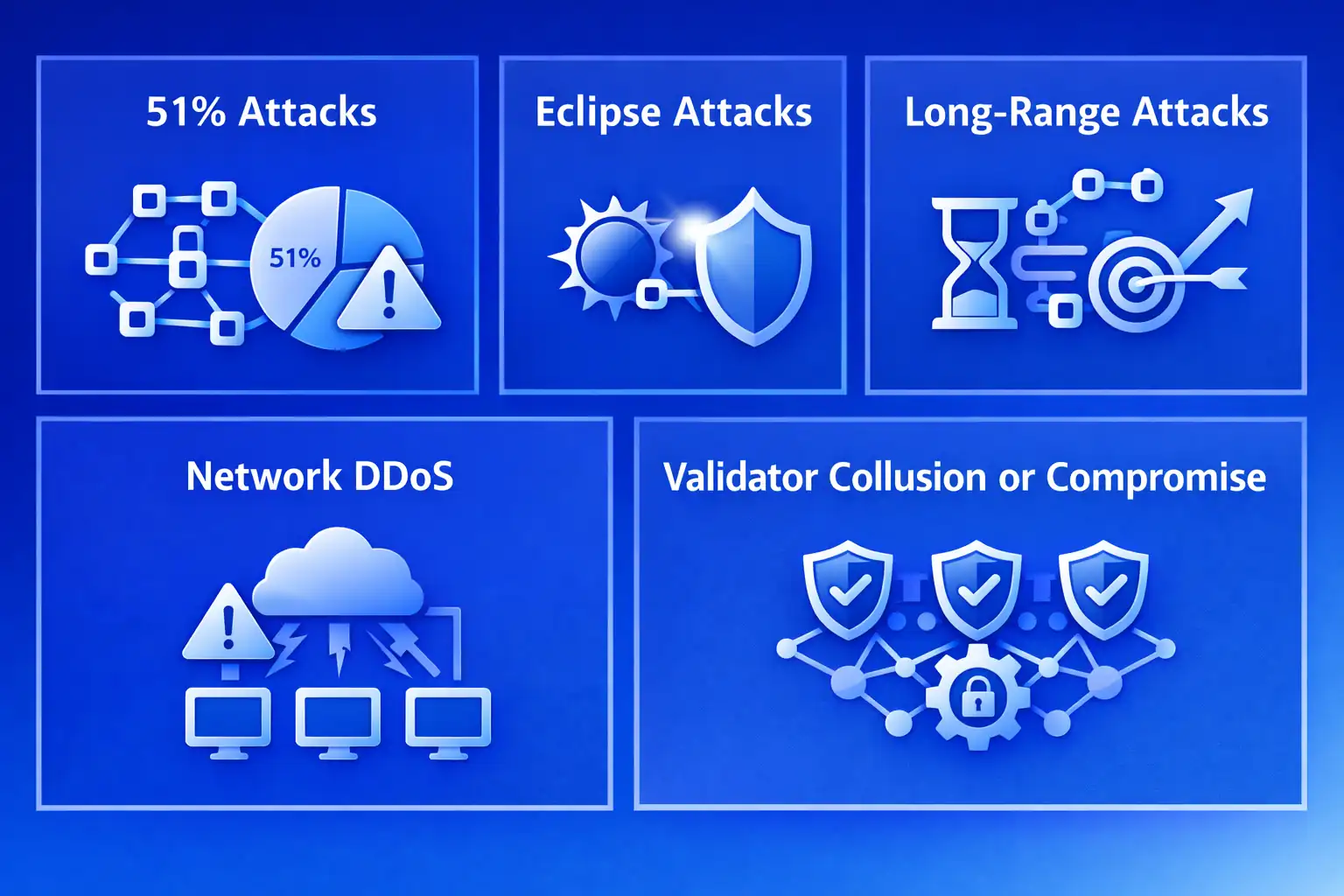

While smart contract vulnerabilities and private key management represent the most common real estate tokenization risks, blockchain network attacks targeting the underlying distributed ledger infrastructure can affect entire ecosystems of tokenized assets simultaneously. Network-level attacks include 51% attacks where attackers gain majority consensus control, eclipse attacks isolating nodes from the honest network, long-range attacks rewriting blockchain history, and various other consensus manipulation techniques potentially compromising asset integrity across all network participants.

The likelihood and severity of blockchain network attacks depend significantly on network characteristics including consensus mechanism, decentralization level, economic security, and maturity. Established networks like Ethereum and Bitcoin with thousands of independent validators and extensive economic value securing consensus are extremely resilient to network attacks, with successful attacks requiring resources exceeding attacker potential benefits. Newer or smaller networks with limited validator sets and lower economic security face elevated attack risks affecting real estate tokenization platforms built on these chains.

Real estate tokenization platforms selecting blockchain infrastructure must assess network security as a foundational consideration. A platform implementing perfect smart contract security, excellent key management, and comprehensive operational security remains vulnerable if the underlying blockchain network can be attacked successfully. Historical incidents demonstrate these risks are not merely theoretical, with numerous smaller blockchains experiencing 51% attacks resulting in double-spending and transaction reversals.

Types of Blockchain Network Attacks

51% Attacks (Consensus Takeover)

Occur when attackers control majority of network hash power (Proof of Work) or stake (Proof of Stake), enabling transaction reversal, double-spending, and censorship. For real estate tokenization, successful 51% attacks could reverse property sales, enable double-selling of tokens, or censor legitimate transactions. Cost of attacking major networks like Ethereum exceeds $1 billion making attacks economically irrational, but smaller chains face realistic attack threats. Ethereum Classic suffered multiple 51% attacks with millions in double-spend losses.

Eclipse Attacks (Network Isolation)

Attackers isolate target nodes from honest network participants, feeding them false information about blockchain state. Isolated nodes might accept invalid transactions, double-spends, or operate on minority chain forks. For tokenized real estate, eclipse attacks could convince platforms or investors that transactions occurred or didn’t occur, enabling fraud. Defense requires diverse peer connections, monitoring connectivity, and validating blockchain state through multiple sources.

Long-Range Attacks (History Rewriting)

Relevant primarily to Proof of Stake chains, attackers attempt creating alternative blockchain histories from deep in the past using old validator keys or stakes. Successfully executing long-range attacks could invalidate weeks or months of transactions including property transfers, distributions, and governance decisions. Mitigation includes checkpointing, social consensus on valid chain history, and validator key rotation preventing old keys from being used for history rewrites.

Network DDoS (Service Disruption)

Distributed denial of service attacks flooding network nodes with traffic, preventing transaction processing and consensus participation. While DDoS doesn’t directly steal funds, disruption prevents property sales, distribution payments, governance votes, and emergency responses. Real estate tokenization platforms require DDoS protection at infrastructure level and should maintain alternative communication channels for critical operations during network disruptions.

Validator Collusion or Compromise

On networks with small validator sets, attackers might compromise or collude with validators to manipulate consensus. Particularly relevant for permissioned blockchains or proof-of-authority networks where limited validators control consensus. Real estate tokenization on such networks faces centralization risks where validator compromise enables transaction manipulation, censorship, or fraud. Public blockchains with thousands of independent validators provide stronger security against such attacks.

The economic security model of blockchain networks determines attack cost and likelihood. Networks secured by extensive capital investment (either mining equipment or staked assets) make attacks expensive relative to potential gains. Attacking Ethereum would require controlling over $20 billion in staked ETH, making such attacks economically irrational. Conversely, smaller networks with market capitalizations under $100 million face realistic attack economics where attackers could profit from attacks costing millions to execute.

For real estate tokenization platforms operating in the USA, UK, UAE, and Canada, blockchain selection should prioritize established networks with strong security track records. Ethereum, Polygon (inheriting Ethereum security), and other well-established chains have operated for years without successful consensus attacks. Experimental or newer blockchains, despite potentially attractive features, introduce elevated real estate tokenization risks from network-level vulnerabilities that should be avoided for platforms managing significant investor capital.

Network Security Principle: Blockchain network security for real estate tokenization should be considered non-negotiable infrastructure requirement similar to using established banking systems for traditional property transactions. While promising new blockchains emerge offering technical advantages, their unproven security makes them unsuitable for tokenizing high-value real estate until they demonstrate years of successful operation securing significant value. Investors should be skeptical of platforms using obscure or new blockchains regardless of claimed technical superiority, recognizing that real estate tokenization risks from network-level vulnerabilities can wipe out entire platforms regardless of other security measures.

Monitoring and responding to blockchain network attacks requires specialized infrastructure and expertise that many platforms lack. Real estate tokenization platforms should implement network monitoring detecting unusual consensus patterns, maintain relationships with blockchain developers and security researchers tracking emerging threats, subscribe to security intelligence services, and plan incident response procedures for various network attack scenarios including transaction censorship, chain reorganizations, or network partitions.

Oracle Manipulation and Off-Chain Data Security Risks

Oracles, systems providing off-chain data to smart contracts, represent critical dependencies in real estate tokenization platforms where accurate property valuations, rental income verification, insurance claims validation, and market pricing determine critical contract decisions. Oracle manipulation and off-chain data security issues create real estate tokenization risks enabling attackers to artificially inflate property values triggering improper liquidations, falsify income data affecting distributions, manipulate pricing for unfair trades, and compromise governance decisions based on corrupted information.

The oracle problem arises from blockchain’s isolation from external data sources. Smart contracts executing on-chain cannot directly access off-chain information like property appraisals, rental payments, or market prices. Oracles bridge this gap by importing external data, but this dependency creates trust assumptions and attack vectors absent in fully on-chain systems. If smart contracts are “law” on blockchain, oracles are the “facts” those laws operate on, making oracle integrity paramount.

Real estate tokenization platforms require oracles for multiple critical functions including property valuation updates affecting loan-to-value ratios and liquidation triggers, rental income verification determining distribution amounts, insurance event validation for claim processing, market price feeds for secondary trading and fair value accounting, compliance data confirming regulatory requirements, and environmental monitoring for properties with sustainability commitments. Each oracle dependency represents a potential manipulation point where data corruption creates cascading failures across platform operations.

| Oracle Type | Use in Real Estate Tokenization | Manipulation Risks | Mitigation Strategies |

|---|---|---|---|

| Price Oracles | Property market values, token pricing for secondary trading, collateral valuations | Flash crashes triggering liquidations, artificial inflation enabling over-borrowing, manipulated pricing for unfair trades | Multiple independent sources, time-weighted averages, outlier detection, conservative collateralization |

| Income Verification Oracles | Rental payment confirmation, revenue verification, operating expense validation | False income reporting increasing distributions unsustainably, expense manipulation affecting valuations | Bank API integration, property management system connections, regular auditor verification |

| Event Verification Oracles | Insurance claims, property damage, tenant default events, major repairs | False claims triggering improper payouts, missed actual events delaying responses | Professional verification requirements, multi-party confirmation, photographic evidence |

| Compliance Oracles | Regulatory requirement monitoring, jurisdictional rule changes, investor eligibility verification | Incorrect compliance data enabling unauthorized trades, missed regulatory changes causing violations | Legal firm verification, regulatory database integration, conservative interpretation of ambiguous requirements |

| Environmental Monitoring Oracles | Energy usage verification, sustainability metrics, environmental compliance monitoring | False reporting of environmental performance, missed compliance violations | IoT sensor networks, third-party auditor verification, certification body integration |

Oracle manipulation techniques targeting real estate tokenization include compromising data sources providing information to oracles, attacking oracle node operators or validators, exploiting time delays between data generation and on-chain submission, flash loan attacks manipulating market prices during brief vulnerability windows, and social engineering of oracle operators to input false data. Historical DeFi exploits demonstrate these attacks are technically feasible and economically motivated, with over $500 million lost to oracle manipulation attacks across various protocols.

Decentralized oracle networks like Chainlink, Band Protocol, and API3 attempt addressing oracle real estate tokenization risks through multiple independent data providers, economic incentives aligning oracle behavior with accurate reporting, reputation systems penalizing false data submission, and cryptographic proofs enabling verification. While decentralized oracles significantly improve security over single-source oracles, they introduce additional complexity, gas costs, and latency that platforms must balance against security benefits.

Case Study: Property Valuation Oracle Manipulation

A 2022 incident on a real estate tokenization test network demonstrated oracle manipulation vulnerabilities when security researchers artificially manipulated property valuation data during a controlled exploit. The platform used a single-source oracle for property valuations updated monthly. Researchers compromised the API endpoint providing valuation data and submitted inflated property values 3x above market rates.

Smart contracts accepting these inflated valuations allowed over-borrowing against tokenized properties, with users extracting 200% of actual property value in loans. When manipulation was discovered and valuations corrected, collateral values dropped below loan amounts triggering mass liquidations. In a production environment with real funds, this exploit would have enabled draining platform liquidity through over-borrowing then defaulting on loans secured by overvalued collateral.

The platform subsequently implemented decentralized oracles with five independent valuation sources, outlier detection filtering extreme values, time-weighted averaging reducing flash manipulation effectiveness, and conservative collateralization ratios maintaining healthy loan-to-value margins even with 30% valuation variance. This incident demonstrates oracle manipulation real estate tokenization risks are not theoretical but require comprehensive technical and economic safeguards.

Off-chain data security extends beyond oracles to include property management systems, accounting platforms, KYC/AML databases, and other external systems integrated with tokenization platforms. Each integration point represents an attack surface where compromised external systems can inject false data, expose sensitive information, or enable unauthorized operations. Comprehensive security requires treating the entire technology stack, not just smart contracts and blockchain infrastructure, as critical components requiring protection.

For real estate tokenization platforms in the USA, UK, UAE, and Canada, oracle security takes on regulatory dimensions as accurate valuation and income reporting affects securities compliance, tax obligations, and investor protections. Platforms must implement oracle solutions meeting professional standards for data accuracy, maintain audit trails proving data integrity, and disclose oracle dependencies and associated risks to investors. Regulatory scrutiny of oracle failures that harm investors is likely to intensify as tokenization matures.

Oracle Security Best Practice: Real estate tokenization platforms should implement defense-in-depth oracle strategies using multiple independent data sources, decentralized oracle networks when available, time-weighted averages reducing flash manipulation effectiveness, outlier detection filtering extreme values, conservative parameters maintaining safety margins for valuation variance, and fallback mechanisms enabling manual intervention if oracle failures detected. Single-source oracles or platforms lacking comprehensive oracle security represent elevated real estate tokenization risks investors should avoid. Platforms should transparently disclose oracle dependencies, security measures, and residual risks in investor documentation.

Identity, KYC, and Access Control Vulnerabilities

Identity verification, Know Your Customer (KYC) compliance, and access control systems represent critical security infrastructure for real estate tokenization platforms, with vulnerabilities enabling unauthorized investment by ineligible investors, regulatory violations resulting in enforcement actions, identity theft facilitating fraud, and account takeovers enabling asset theft. These real estate tokenization risks span both regulatory compliance failures and direct financial losses, affecting platform viability and investor protection simultaneously.

KYC and Anti-Money Laundering (AML) requirements for tokenized real estate exist throughout the USA, UK, UAE, and Canada with securities regulations requiring platforms to verify investor identities, confirm accreditation status where applicable, screen against sanctions lists, monitor for suspicious activities, and maintain comprehensive records. Non-compliance creates regulatory liability through enforcement actions, criminal penalties for willful violations, investor lawsuits, and potential platform shutdowns. Additionally, inadequate KYC enables money laundering, terrorist financing, and sanctions evasion creating societal harms beyond individual platform concerns.

Identity verification systems in real estate tokenization face unique challenges balancing blockchain pseudonymity with regulatory requirements for knowing investor identities. Platforms must link off-chain verified identities to on-chain wallet addresses, maintain this mapping securely while respecting privacy, enforce transfer restrictions preventing tokens from moving to unverified addresses, and handle edge cases like wallet changes, lost access, and beneficiary changes. Each requirement introduces technical complexity and potential vulnerability creating real estate tokenization risks.

KYC and Identity Vulnerabilities in Real Estate Tokenization

Synthetic Identity Fraud

Attackers create fake identities using combination of real and fabricated information, passing automated verification systems while representing non-existent persons. Enables unauthorized investment bypassing accreditation requirements, creates regulatory violations, and complicates enforcement if fraud discovered. Detection requires sophisticated identity verification beyond document checks including behavioral analysis, data consistency validation, and cross-referencing multiple information sources.

Document Forgery

Sophisticated forgery of identity documents (passports, driver’s licenses, bank statements) enables bypassing KYC verification. Platforms using basic document verification without forensic analysis or liveness checks remain vulnerable. Mitigation requires machine learning detecting forgery patterns, government database integration for real-time verification, and biometric liveness detection preventing photo substitution.

Account Takeover

Credential theft through phishing, database breaches, or social engineering enables unauthorized account access. Even with strong wallet security, compromised platform accounts can enable unauthorized trades, distribution redirects, or sensitive information theft. Defense requires multi-factor authentication, anomaly detection flagging unusual activity, transaction confirmation requirements, and session management limiting access duration and geographic scope.

Wallet-Identity Unlinking

KYC-verified wallet addresses might transfer tokens to unverified addresses circumventing transfer restrictions. Smart contracts must enforce recipient verification, but implementation complexity creates vulnerabilities. Some platforms allow token transfers only between KYC-verified addresses within the platform ecosystem. Others permit open transfers but require re-verification before certain actions like voting or claiming distributions.

Accreditation Fraud

In jurisdictions requiring accredited investor status for certain real estate tokenization offerings, platforms must verify income, net worth, or professional credentials. Fraudulent accreditation claims using forged financial statements, fake employer verifications, or incorrect credential claims enable unauthorized participation. Verification requires integration with financial institutions, employment databases, and professional licensing authorities rather than accepting self-certification.

Sanctions and PEP Screening Failures

Inadequate screening against sanctions lists (OFAC, UN, EU) or Politically Exposed Persons (PEP) databases enables prohibited transactions creating regulatory violations and potential criminal liability. Requires integration with comprehensive screening databases, ongoing monitoring for list updates, and clear procedures for handling matches. False positives requiring manual review create operational challenges balanced against compliance necessity.

Third-party KYC service providers like Sumsub, Onfido, Jumio, and Chainalysis offer comprehensive identity verification, sanctions screening, and ongoing monitoring reducing platform development burden while providing specialized expertise. However, dependence on third-party providers introduces additional real estate tokenization risks including provider outages disrupting operations, data breaches exposing sensitive information, provider termination requiring migration, and varying service quality across providers affecting verification accuracy and user experience.

Privacy considerations create tension with KYC requirements in real estate tokenization. Blockchain transparency conflicts with privacy regulations like GDPR in Europe, PIPEDA in Canada, and various state privacy laws in the USA. Platforms must balance regulatory requirements for knowing investors with privacy obligations minimizing data collection and enabling data deletion upon request. Solutions include storing identity data off-chain with on-chain attestations, zero-knowledge proofs enabling verification without revealing underlying data, and privacy-preserving computation enabling compliance checking without exposing sensitive information.

| Jurisdiction | KYC/AML Requirements | Accreditation Rules | Enforcement Approach |

|---|---|---|---|

| USA | Bank Secrecy Act, FinCEN guidance on virtual assets, customer identification program requirements, suspicious activity reporting | Reg D private placements require accredited investor verification with income/net worth documentation, professional credentials | Aggressive SEC enforcement, substantial penalties for KYC/accreditation failures, criminal prosecution for willful violations |

| UK | Money Laundering Regulations, FCA requirements for financial services, customer due diligence, enhanced due diligence for high-risk customers | Sophisticated investor classification based on net assets, professional status, or self-certification, less restrictive than US accreditation | FCA supervision with regulatory actions for non-compliance, criminal penalties for money laundering facilitation |

| UAE (Dubai) | VARA regulations for virtual asset service providers, DFSA rules for financial free zones, comprehensive KYC and transaction monitoring requirements | Professional investor classification based on net assets, investment experience, or institutional status | Progressive regulation balancing innovation and protection, VARA enforcement powers including license suspension or revocation |

| Canada | FINTRAC requirements under PCMLTFA, provincial securities commission KYC requirements, customer identification and verification | Accredited investor exemptions under NI 45-106 based on income, financial assets, or sophisticated purchaser status | Provincial securities commission enforcement, FINTRAC penalties for AML violations, criminal prosecution for serious violations |

Access control vulnerabilities extend beyond initial identity verification to ongoing platform security including role-based access controls distinguishing administrators, property managers, and investors with appropriate permissions, session management preventing unauthorized access through stolen credentials, API security protecting programmatic access points, and administrative function protections preventing privilege escalation. Each access point represents potential vulnerability where inadequate controls enable unauthorized operations affecting real estate tokenization risks.

Compliance Warning: KYC and identity verification represent both security and regulatory requirements for real estate tokenization platforms. Inadequate identity controls create direct fraud risks through unauthorized access and regulatory risks through compliance failures. Platforms operating in the USA, UK, UAE, and Canada must implement institutional-grade KYC solutions meeting regulatory standards rather than viewing identity verification as optional or implementing minimal checkbox compliance. Real estate tokenization risks from identity failures include not just financial losses but regulatory enforcement potentially shutting down entire platforms and exposing founders to personal liability.

Regulatory and Compliance-Related Security Risks

Regulatory and compliance failures represent existential real estate tokenization risks that can destroy platform value instantly regardless of underlying property quality, technical security, or operational excellence. Unlike gradual security degradation from technical vulnerabilities, regulatory enforcement actions can result in immediate platform shutdowns, frozen assets, criminal prosecutions, and complete loss of investor capital through mechanisms having nothing to do with hacking or theft but everything to do with legal non-compliance.

The regulatory landscape for tokenized real estate spans securities laws, anti-money laundering regulations, consumer protection frameworks, data privacy requirements, and real estate-specific regulations across the USA, UK, UAE, and Canada. Each jurisdiction maintains distinct regulatory approaches with varying interpretations of how existing laws apply to novel tokenization structures, creating compliance complexity that platforms must navigate successfully to avoid catastrophic legal consequences.

Securities law compliance represents the primary regulatory concern for real estate tokenization platforms. In the USA, the SEC applies the Howey Test determining whether tokens constitute securities requiring registration or qualifying exemptions. Most property tokens clearly qualify as securities through investment contract analysis, triggering comprehensive disclosure requirements, ongoing reporting obligations, transfer restrictions, and broker-dealer regulations. UK FCA applies similar analysis under Financial Services and Markets Act frameworks. UAE VARA and DFSA have established specific digital asset security frameworks. Canadian securities commissions apply provincial securities laws with National Instrument guidance.

Major Regulatory Compliance Risks

Unregistered Securities Offerings

Offering real estate tokens without proper securities registration or valid exemptions constitutes illegal securities distribution triggering SEC enforcement, investor rescission rights enabling forced buybacks at original purchase prices plus interest, criminal penalties for willful violations, and civil monetary penalties. Historical cases include Telegram forced to return $1.2 billion to investors and pay $18.5 million penalty. Platforms must obtain legal opinions confirming securities compliance before any token sales.

Inadequate Disclosure and Misrepresentation

Securities laws require comprehensive disclosure of material information including property details, financial projections, risk factors, management backgrounds, and conflicts of interest. Inadequate disclosures or affirmative misrepresentations create fraud liability under Rule 10b-5, investor lawsuits seeking damages, and regulatory enforcement. Real estate tokenization platforms must maintain disclosure standards equivalent to traditional securities offerings including regular updates as material facts change.

Transfer Restriction Violations

Many securities exemptions like Regulation D require transfer restrictions preventing immediate resale. Smart contracts must enforce holding periods, accredited investor verification, and volume limitations programmatically. Failures enabling unrestricted secondary trading violate exemption conditions, destroying exemption validity and potentially converting offerings into illegal unregistered public offerings. Technical implementation of transfer restrictions requires careful smart contract design validated through legal review.

AML/KYC Compliance Failures

Money laundering and terrorist financing regulations require comprehensive customer identification, sanctions screening, suspicious activity reporting, and transaction monitoring. Platforms facilitating money laundering through inadequate controls face criminal prosecution under Bank Secrecy Act, FINTRAC violations, civil monetary penalties, and potential individual liability for responsible executives. Real estate’s historical association with money laundering intensifies regulatory scrutiny of tokenization platforms.

Cross-Border Offering Violations

International real estate tokenization raises jurisdictional questions about which country’s securities laws apply. Offering tokens to investors in jurisdictions where platforms lack proper authorization or registration creates violation risks. USA maintains long-arm jurisdiction over foreign platforms offering to US investors. EU countries apply prospectus requirements. Platforms must either restrict offerings geographically or comply with regulations in all target jurisdictions, significantly increasing compliance complexity and costs.

Regulatory uncertainty compounds compliance real estate tokenization risks as lawmakers and regulators continue developing frameworks for digital securities. Positions that appear compliant under current guidance may be deemed non-compliant as regulations evolve or enforcement priorities shift. Platforms cannot assume regulatory safe harbor simply because they haven’t faced enforcement yet, as agencies often observe markets before establishing enforcement precedents that affect entire industries retroactively.

The cost of comprehensive regulatory compliance represents substantial operational expense that some platforms attempt minimizing through regulatory arbitrage, seeking permissive jurisdictions, or simply operating without proper authorization. These approaches create severe real estate tokenization risks as regulatory authorities increasingly coordinate internationally, making jurisdictional shopping less effective. Additionally, investors increasingly demand platforms demonstrating regulatory compliance as table stakes for participation, making non-compliant platforms commercially unviable regardless of legal tolerance.

| Compliance Requirement | Implementation Cost | Non-Compliance Consequences |

|---|---|---|