Ai Overview

Web3 represents the next generation of the internet, one characterized by decentralization, user ownership, and trustless interactions facilitated by smart contracts. Stablecoins eliminate this uncertainty entirely, ensuring that a $100 payment initiated in USDC today is still worth $100 upon receipt. Traditional international wire transfers can take 2 to 5 business days to settle, involve multiple correspondent banks, and carry fees ranging from 3% to 7%.

Key Takeaways

- Stablecoins in Web3 eliminate price volatility, enabling predictable digital transactions for businesses and users in the USA, UK, UAE, and Canada.

- The stablecoin ecosystem underpins DeFi lending, borrowing, and yield farming across decentralized platforms without traditional banking intermediaries.

- DeFi stablecoins facilitate cross-border crypto payments at significantly lower fees compared to conventional remittance and SWIFT-based wire transfers.

- Smart contract-based payment automation powered by stablecoins reduces settlement times from days to seconds in decentralized finance environments.

- Web3 adoption is accelerating as stablecoins provide financial accessibility to underbanked populations in emerging markets and established economies alike.

- Regulatory compliance remains a top priority, with the EU MiCA framework and US stablecoin legislation shaping the decentralized economy’s future governance.

- Gaming, NFTs, and virtual metaverse economies increasingly rely on stablecoins to price digital assets and reward players with consistent purchasing power.

- Algorithmic, fiat-backed, and crypto-collateralized stablecoins serve distinct roles within the broader Web3 economy and decentralized financial infrastructure.

- Yield farming and liquidity pools depend on stablecoins to generate consistent returns while reducing impermanent loss risk for decentralized finance participants.

- The tokenized economy of 2025 and beyond will see stablecoins bridge real-world assets with on-chain markets, redefining global financial infrastructure.

Why Stablecoins Matter in Web3

Web3 represents the next generation of the internet, one characterized by decentralization, user ownership, and trustless interactions facilitated by smart contracts. However, for this ecosystem to function practically, a stable medium of exchange is essential. Stablecoins in Web3 fulfill this role by providing a price-predictable asset that participants can use for trading, lending, borrowing, and earning yields without worrying about drastic value swings undermining their positions.

In the UAE, where crypto adoption among enterprises and government institutions is accelerating, stablecoins are being utilized for everything from real estate transactions to supply chain financing. In Canada, fintech startups are leveraging the stablecoin ecosystem to offer dollar-equivalent payments to international contractors without the delays of SWIFT transfers. These practical applications underscore why stablecoins are considered the circulatory system of the Web3 economy.

Furthermore, stablecoins serve as the primary on-ramp for new participants entering decentralized finance. When a user converts their local fiat currency into a stablecoin, they gain immediate access to a vast ecosystem of DeFi protocols, decentralized exchanges, and Web3 applications without assuming the speculative risk associated with holding volatile crypto assets.

Types of Stablecoins Used in Blockchain Networks

Understanding the different categories of stablecoins is critical for anyone participating in the Web3 economy. Each type carries distinct risk profiles, collateralization models, and use cases within decentralized financial systems and blockchain applications.

Fiat-Backed Stablecoins

- Backed 1:1 by USD or equivalent reserves

- Examples: USDT, USDC, BUSD

- Audited by third-party institutions

- Highest adoption in crypto payments

- Central custodianship introduces counterparty risk

Crypto-Collateralized Stablecoins

- Overcollateralized with crypto assets

- Example: DAI backed by ETH

- Governed by decentralized protocols

- More transparent on-chain reserve structure

- Subject to liquidation during market downturns

Algorithmic Stablecoins

- Supply adjusted algorithmically

- No physical collateral requirement

- Higher risk of de-pegging events

- Innovative but requires robust governance

- Post-Terra/LUNA era demands caution

The Role of Stablecoins in the Web3 Economy

Stablecoins function as the foundational monetary layer of Web3, connecting users, protocols, and applications across the decentralized economy.

Enabling Stable Digital Transactions

One of the most fundamental roles stablecoins play in the Web3 economy is enabling consistent, predictable value transfers that both buyers and sellers can rely on. In traditional crypto ecosystems, the price of an asset at the time a transaction is initiated may differ dramatically from its value by the time settlement occurs. Stablecoins eliminate this uncertainty entirely, ensuring that a $100 payment initiated in USDC today is still worth $100 upon receipt.

This stability is particularly valuable web3 for e-commerce platforms, SaaS businesses, and digital service providers in the UK and USA that are beginning to accept cryptocurrency but cannot afford to absorb exchange rate volatility. By denominating contracts and invoices in stablecoins, these organizations can enjoy the speed and borderlessness of blockchain payments while maintaining budget predictability.

Additionally, stablecoins reduce the friction of Web3 onboarding. New users entering decentralized platforms can begin transacting immediately in stablecoins, building confidence in the ecosystem before they choose to explore more volatile crypto assets. This frictionless entry has been a key driver of Web3 adoption globally.

Supporting Decentralized Financial Activities

Decentralized finance relies almost exclusively on stablecoins to function at scale. Protocols like Aave, Compound, and MakerDAO allow users to deposit stablecoins as collateral, borrow against them, and earn interest, all without any bank or financial institution acting as intermediary. The stablecoin ecosystem powers every layer of this system, from the initial liquidity deposits to the final interest payments distributed to yield farmers.

For users in Canada and the UAE seeking exposure to decentralized financial services, stablecoins represent the most practical entry point. Rather than converting local currency into a volatile asset, users can hold USDC or DAI and immediately access lending platforms, decentralized exchanges, and insurance protocols within the Web3 ecosystem.

The governance frameworks surrounding DeFi stablecoins also contribute to financial transparency. On-chain reserve data, liquidation mechanisms, and voting-based protocol upgrades give participants visibility into the systems they rely on, a stark contrast to the opacity of traditional financial institutions.

Improving Liquidity Across Web3 Platforms

Liquidity is the lifeblood of any financial market, and in Web3, stablecoins are the primary source of that liquidity. Decentralized exchanges such as Uniswap, Curve, and Balancer rely on stablecoin pairs to provide low-slippage trading environments. When a user wishes to swap ETH for another token, the availability of deep stablecoin liquidity pools ensures the trade can be executed efficiently with minimal price impact.

Stablecoin liquidity also underpins the broader credit markets within decentralized finance. When lenders deposit USDC into a protocol, borrowers can access immediate capital without waiting for traditional credit approvals. This real-time, permissionless credit market has democratized financial access in ways that traditional banking simply cannot replicate.

Platforms like Curve Finance have been specifically optimized for stablecoin-to-stablecoin swaps, demonstrating that the market has recognized the unique liquidity profile these assets offer. The depth and stability of stablecoin pools remain a critical metric for the health of the entire Web3 economy.

How Stablecoins Power Web3 Payments?

Crypto payments are evolving from a fringe concept to a practical payment infrastructure. Stablecoins are at the center of this evolution, offering a digital payment method that combines the programmability and borderlessness of blockchain with the price stability of fiat currency. For merchants, service providers, and consumers globally, this combination unlocks unprecedented payment efficiencies.

From instant micropayments in Web3 gaming to large B2B transfers between corporations in the USA and UAE, stablecoins are proving that decentralized payment rails can outperform traditional financial infrastructure in speed, cost, and accessibility. The following sub-sections examine the specific mechanisms through which stablecoins are transforming global payment systems.

Faster Cross-Border Transactions

Traditional international wire transfers can take 2 to 5 business days to settle, involve multiple correspondent banks, and carry fees ranging from 3% to 7%. Stablecoin transfers, by contrast, can settle in seconds to minutes on blockchain networks like Ethereum, Solana, or Polygon, often at a fraction of a cent in transaction fees. This represents a transformational improvement in the efficiency of cross-border commerce.

For companies in the UK hiring remote talent in Southeast Asia or Africa, paying in USDC means workers receive value immediately, without losing 5% to foreign exchange conversion fees. For UAE-based import businesses procuring goods from global suppliers, stablecoin payments eliminate the need for letters of credit and reduce settlement risk dramatically.

This speed advantage is not just convenient, it is strategically significant. In fast-moving supply chains and real-time financial markets, the ability to settle in near-real-time using stablecoins creates competitive advantages that organizations leveraging traditional banking cannot replicate.

Peer-to-Peer Payments Without Intermediaries

Web3’s core value proposition is trustless, intermediary-free value exchange. Stablecoins realize this promise in the payments domain by enabling direct peer-to-peer transfers of stable value between any two wallets on the blockchain. There is no bank to approve the transaction, no payment processor to charge a percentage, and no settlement delay. The transfer is final as soon as it is recorded on the blockchain.

This is particularly powerful for the gig economy and creator ecosystem. A freelance designer in Canada who invoices a client in the USA can receive USDC payment directly into their non-custodial wallet within minutes of project completion, with full control over their funds and no bank account required. Platforms like Request Network and Superfluid are building entire payment infrastructure layers on top of stablecoin rails.

The elimination of intermediaries also reduces censorship risk. In jurisdictions where banking access is limited or politically constrained, stablecoin P2P payments provide a censorship-resistant alternative that keeps the decentralized economy accessible to all participants.

Smart Contract-Based Payment Automation

Smart contracts unlock a new paradigm in payment automation, and stablecoins are the currency that makes these automated systems financially viable. A smart contract can be programmed to release stablecoin payments upon the completion of predefined conditions, such as the delivery of a digital asset, the expiry of a vesting period, or the achievement of a performance milestone. This conditional payment logic is impossible to replicate at scale in traditional banking.

Applications include streaming salary payments in DeFi platforms, where employees receive stablecoin compensation in real-time as they work, rather than waiting for a monthly payroll cycle. Similarly, decentralized autonomous organizations use smart contract-based stablecoin distributions to pay contributors and fund operational expenses without manual treasury management.

The marriage of stablecoins and smart contracts is arguably the most powerful innovation in the Web3 payments space. It transforms financial agreements from paper contracts requiring human enforcement into self-executing code that settles automatically and transparently, reducing dispute risk and administrative overhead simultaneously.

Stablecoins Supporting Web3 Adoption

Web3 adoption faces several barriers: complexity of wallet management, unfamiliar concepts of private keys, and concerns about volatility. Stablecoins directly address the volatility barrier, making the Web3 user experience dramatically less intimidating for first-time participants. When new users know that their USDC will be worth $1 tomorrow, the psychological barrier to engaging with decentralized platforms drops significantly.

Globally, stablecoins are becoming the gateway drug for Web3 participation. In emerging markets, stablecoins denominated in US dollars serve as a store of value protecting local populations from currency devaluation. In developed markets like the USA, UK, UAE, and Canada, they serve as the practical currency for digital commerce and decentralized application interaction. Either way, stablecoins are the instrument driving mainstream Web3 adoption.

Making Crypto Payments More Practical

The practical usability of crypto payments was severely limited in the early days of Bitcoin and Ethereum due to price volatility. A merchant who accepted Bitcoin for a product priced at $100 might find the payment worth $80 by the time they checked their wallet. Stablecoins eliminate this settlement risk entirely, making crypto payments as practical as credit card transactions from the merchant’s perspective.

Major payment infrastructure providers including Stripe, Shopify, and PayPal have begun integrating stablecoin payment options into their platforms, signaling that the financial mainstream is ready to embrace stablecoin-based crypto payments. Merchants in the UK and USA who integrate USDC payments can now offer customers a frictionless digital payment alternative without the volatility exposure that previously made crypto unworkable for commerce.

For the consumer, stablecoin payments offer privacy advantages over credit cards and bank transfers, as well as access to smart contract-based loyalty programs, automated refund mechanisms, and micropayment capabilities that simply do not exist in the traditional payment landscape.

Enhancing Financial Accessibility

Over 1.4 billion adults globally remain unbanked, lacking access to basic financial services. Stablecoins in Web3 represent a historically significant opportunity to provide these individuals with dollar-equivalent savings, cross-border payments, and access to credit markets, all through a smartphone and internet connection. No bank account, credit history, or government identification required.

In regions with unstable local currencies, stablecoins pegged to the US dollar offer a more reliable store of value than the local fiat alternative. Citizens of countries experiencing inflation can hold USDC or USDT as a dollar-denominated savings instrument, preserving purchasing power in ways that their local banking system cannot guarantee.

The combination of financial accessibility and digital programmability positions stablecoins as a foundational tool for financial inclusion. As mobile internet penetration continues to grow in emerging markets, the stablecoin ecosystem is positioned to bring billions of new participants into the global decentralized economy.

Building Trust Through Price Stability

Trust is the foundational requirement for any financial system, and stablecoins build that trust through price transparency and programmatic reserve management. Unlike speculative cryptocurrencies, where price discovery is driven entirely by market sentiment, stablecoins offer a clearly defined value proposition: one token equals one dollar. This predictability builds institutional and retail confidence simultaneously.

Leading stablecoin issuers like Circle (USDC) publish monthly attestation reports audited by major accounting firms, providing transparent confirmation of reserve adequacy. For enterprise adopters in the UAE and Canada evaluating stablecoin integration, this level of financial transparency compares favorably with opaque traditional banking counterparts.

As the stablecoin ecosystem matures and regulatory frameworks clarify in major markets, the trust foundation will only strengthen. This growing institutional confidence is a key driver of Web3 adoption among organizations that previously viewed cryptocurrency as too speculative for operational integration.

Real-World Use Cases of Stablecoins in Web3

Stablecoins are no longer theoretical constructs. Across e-commerce, remittances, gaming, and the metaverse, their practical applications are reshaping entire industries and creating new economic opportunities that were impossible before the stablecoin ecosystem reached critical maturity.

| Use Case | Stablecoin Used | Market | Key Benefit |

|---|---|---|---|

| E-Commerce Payments | USDC, USDT | USA, UK | Zero chargeback, instant settlement |

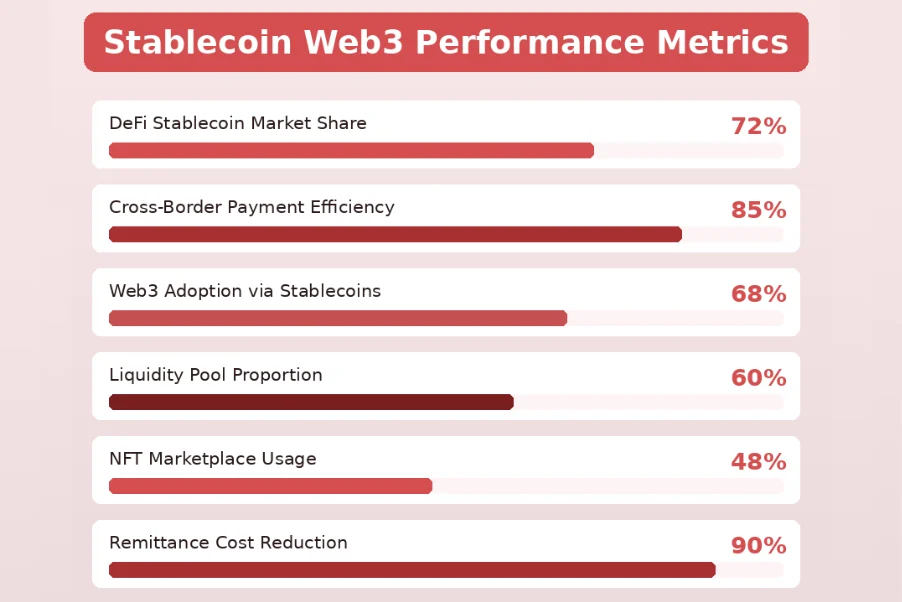

| Cross-Border Remittance | USDT, BUSD | UAE, Canada | 90% lower fees vs. wire transfers |

| DeFi Lending | DAI, USDC | Global | Permissionless credit access |

| NFT Marketplace Pricing | USDC | USA, UK | Stable asset pricing for digital goods |

| Web3 Gaming Rewards | USDT, USDC | Global | Consistent purchasing power for players |

| DAO Treasury Management | DAI, USDC | Canada, UAE | Stable operational reserves |

E-Commerce and Digital Payments

The e-commerce sector is rapidly warming to stablecoin payments. Online retailers in the USA and UK are integrating USDC payment options that provide instant settlement, zero chargeback risk, and access to a growing customer base that prefers crypto-native payment methods. Unlike credit card payments that can take up to 30 days to settle and carry 2-3% processing fees, stablecoin payments settle in minutes with negligible transaction costs.

Platforms like Shopify have enabled stablecoin payment integrations through partners like Coinbase Commerce, allowing merchants to accept USDC without needing deep blockchain expertise. The settlement process is automated, converting customer stablecoin payments into merchant accounts without any manual intervention required.

Beyond traditional retail, digital goods platforms including gaming item marketplaces, stock photography sites, and software license distributors are discovering that stablecoins enable instant global access to their products without the payment gateway delays and currency conversion complications of traditional payment processors.

Remittances and Global Transfers

The global remittance market exceeds $800 billion annually, and traditional providers like Western Union charge average fees of 6-8% for international transfers. Stablecoins are disrupting this market dramatically. A worker in the UAE sending money home to family in South Asia or Africa can transfer USDT directly to a recipient wallet for a fraction of a percent in transaction fees, with the funds arriving in minutes rather than days.

The practical impact on household finances is significant. A 7% fee saving on a $500 monthly remittance adds up to $420 per year, money that stays within the family rather than being captured by financial intermediaries. Platforms like Bitso in Latin America and Coins.ph in Southeast Asia have demonstrated that stablecoin-based remittances can achieve mainstream adoption when combined with accessible user interfaces.

Canada, with one of the world’s largest diaspora communities, represents a particularly important market for stablecoin remittances. The combination of high immigration rates and expensive traditional remittance corridors makes the Canadian market a natural proving ground for stablecoin-based cross-border transfers.

Gaming, NFTs, and Digital Economies

Web3 gaming and the metaverse represent one of the fastest-growing verticals for stablecoin adoption. Play-to-earn games like Axie Infinity and Decentraland incorporate stablecoins as in-game currencies, ensuring that the rewards players earn maintain consistent real-world value. When a player earns 10 USDC for completing a quest, that reward is worth $10 today and tomorrow, unlike volatile game tokens that may halve in value between earning and spending.

NFT marketplaces are increasingly pricing digital artworks, collectibles, and virtual real estate in stablecoins to provide buyers and sellers with clear, volatility-free price discovery. When a digital artwork is listed at 1000 USDC, both parties understand exactly what the transaction is worth, simplifying valuation and reducing negotiation friction.

Virtual real estate in metaverse platforms is emerging as a significant asset class, with stablecoins serving as the primary currency for land purchases and property transactions. As the metaverse economy matures, stablecoins will function as the reserve currency of digital worlds, enabling commerce, services, and labor markets within these virtual environments.

Challenges Associated With Stablecoins in Web3

Despite their transformative potential, stablecoins in Web3 face significant challenges that must be addressed for the ecosystem to reach its full potential. From regulatory uncertainty to technical vulnerabilities and reserve management risks, the path forward requires deliberate governance, technical diligence, and regulatory collaboration.

Understanding these challenges is not a reason for pessimism; it is a prerequisite for responsible participation in the stablecoin ecosystem. Organizations and individuals who approach stablecoin integration with a clear-eyed assessment of the risks are far better positioned to leverage the opportunities these instruments present.

Regulatory and Compliance Concerns

The regulatory landscape for stablecoins remains fragmented and evolving across major markets. In the USA, the SEC and CFTC have competing jurisdictional claims over different categories of stablecoins, creating compliance uncertainty for issuers and enterprise adopters. The proposed US Stablecoin Act is still working through Congress, leaving businesses operating in a gray zone that complicates treasury and payment planning.

The EU has made more regulatory progress with its Markets in Crypto-Assets (MiCA) framework, which establishes clear licensing and reserve requirements for stablecoin issuers operating within European markets, including the UK post-Brexit framework through the FCA. The UAE’s VARA framework provides another model of proactive crypto regulation that has made Dubai a stablecoin-friendly jurisdiction for institutional adoption.

For Canadian businesses, the Office of the Superintendent of Financial Institutions (OSFI) guidance on crypto assets affects how banks and regulated entities can interact with stablecoins, requiring careful legal review before integration. The regulatory divergence between markets means that global stablecoin strategies must account for local compliance requirements in each jurisdiction of operation.

Security and Transparency Issues

Smart contract vulnerabilities represent a serious risk in the stablecoin ecosystem. Several high-profile DeFi hacks have exploited weaknesses in stablecoin-integrated protocols, resulting in hundreds of millions of dollars in losses. The immutable nature of blockchain means that once funds are stolen through a contract exploit, recovery is typically impossible without sophisticated governance intervention or legal action.

Transparency, while often cited as a stablecoin advantage, can also be inconsistently applied. Some stablecoin issuers have faced criticism for insufficient disclosure of reserve composition, as the Tether controversy illustrated. Users and institutions relying on stablecoin price parity must be able to verify that claimed reserves are genuinely available and properly segregated.

Phishing attacks, wallet draining malware, and centralized exchange compromises represent additional vectors of risk for stablecoin holders. The security practices of individual users and organizational treasury teams must evolve in parallel with the sophistication of the threat landscape targeting the Web3 economy.

Dependence on Reserve Management

Fiat-backed stablecoins are only as reliable as the reserve management practices of their issuers. If a stablecoin issuer invests reserves in risky or illiquid assets, a sudden demand for redemptions could trigger a liquidity crisis that causes the stablecoin to de-peg from its target value. This concern became particularly acute during the Silicon Valley Bank collapse in 2023, when USDC briefly lost its peg after Circle disclosed $3.3 billion in SVB deposits.

Algorithmic stablecoins carry even more significant reserve risk, as demonstrated by the catastrophic collapse of the Terra/LUNA ecosystem in May 2022, which wiped out over $40 billion in market value and triggered a broader DeFi market contraction. The incident served as a stark warning about the dangers of stablecoins that lack genuine overcollateralization.

Ongoing reserve management risk means that stablecoin users should diversify across multiple issuers and stablecoin types, rather than concentrating all holdings in a single instrument. Crypto-collateralized stablecoins like DAI, with their on-chain, transparent collateral mechanisms, offer an alternative reserve model that reduces dependence on centralized custodians.

The Future of Stablecoins in the Web3 Economy

The next decade will see stablecoins evolve from a financial instrument into fundamental infrastructure for the global decentralized economy.

The trajectory of stablecoins in Web3 points unmistakably toward deeper integration, higher adoption, and broader functionality. Central bank digital currencies (CBDCs) are converging with the stablecoin ecosystem, while traditional financial institutions are building their own regulated stablecoin products. This institutionalization will accelerate the pace at which stablecoins become the default medium of exchange for global digital commerce.

Technological innovations in layer-2 scaling, cross-chain interoperability, and zero-knowledge proof privacy are expanding the capabilities of stablecoin-based systems, enabling them to serve markets and use cases that were previously impractical due to high transaction costs or slow settlement times.

Growth of Stablecoin Infrastructure

The infrastructure supporting stablecoins in Web3 is growing at an unprecedented rate. Layer-2 networks like Arbitrum, Optimism, and Base have dramatically reduced the cost of stablecoin transactions on Ethereum, making micropayments and high-frequency trading strategies economically viable for the first time. Cross-chain bridges have enabled stablecoins to flow seamlessly between blockchain networks, expanding their liquidity and utility across the entire multi-chain Web3 ecosystem.

Payment infrastructure providers like Circle’s Cross-Chain Transfer Protocol (CCTP) and Chainlink’s Cross-Chain Interoperability Protocol (CCIP) are building the interoperability rails that will allow stablecoins to move instantaneously between any blockchain without requiring wrapped token intermediaries or centralized bridging solutions.

Banking institutions in the USA, UK, and Canada are beginning to offer stablecoin custody and integration services, signaling that the infrastructure gap between traditional finance and the stablecoin ecosystem is closing rapidly. This convergence will be a defining feature of the financial landscape over the next five years.

Integration With Web3 Applications

The next generation of Web3 applications will assume stablecoin integration as a baseline feature rather than an optional add-on. Social media platforms, professional networking tools, and content creator economies are building stablecoin payment rails directly into their core product experiences. Platforms like Farcaster and Lens Protocol already allow users to tip content creators in stablecoins without leaving the application environment.

Enterprise applications are also beginning to integrate stablecoins into supply chain management, payroll automation, and accounts payable workflows. A manufacturing company in Canada can automate supplier payments in USDC upon delivery confirmation verified by IoT sensors, creating a fully automated, trustless supply chain finance system that eliminates weeks of manual processing.

The programmability of stablecoins through smart contracts means that applications will increasingly move beyond simple payment functionality to complex financial products embedded directly within user interfaces, making sophisticated DeFi operations as accessible as everyday banking transactions.

Expanding Role in the Tokenized Economy

The tokenized economy represents the convergence of real-world assets with blockchain-based ownership and exchange mechanisms. Stablecoins serve as the settlement currency in this evolving landscape, enabling the purchase, trading, and income distribution of tokenized real estate, bonds, commodities, and equity. As major financial institutions in the USA and UAE tokenize billions in assets, stablecoins will handle the settlement rails that make these transactions possible.

2023-2024: Institutional Stablecoin Adoption

Major banks in USA and UK launch regulated stablecoin pilots; USDC surpasses $40B in circulating supply as institutional treasury adoption accelerates.

2025: MiCA Implementation & Regulatory Clarity

EU MiCA framework fully enforced, creating compliance blueprint for stablecoin issuers; UAE VARA expands licensed stablecoin operators within DIFC.

2026-2027: Tokenized Asset Settlement

Stablecoins become primary settlement currency for tokenized real estate, bonds, and commodities; BlackRock BUIDL fund demonstrates institutional viability.

2028-2030: Global Reserve Currency Role

Dollar-denominated stablecoins process over $10T in annual transaction volume; CBDC-stablecoin interoperability frameworks standardized across G20 nations.

Stablecoin Model Selection Criteria for Organizations

Choosing the right stablecoin model is a critical strategic decision for any organization integrating digital assets into treasury, payments, or DeFi operations.

Step 1: Risk Assessment

- Evaluate counterparty risk of issuers

- Assess reserve composition and quality

- Review historical de-peg incidents

- Audit smart contract security record

- Rate regulatory compliance track record

Step 2: Use Case Fit

- Match stablecoin to payment type

- Evaluate DeFi protocol compatibility

- Assess liquidity depth for volume

- Confirm multi-chain availability

- Verify merchant acceptance rates

Step 3: Governance & Exit

- Establish diversification limits per stablecoin

- Document de-pegging response procedures

- Set maximum single-issuer exposure caps

- Plan off-ramp to fiat if needed

- Schedule quarterly stablecoin reviews

Final Thoughts

Stablecoins in Web3 have evolved from a niche instrument to the essential monetary foundation of the decentralized economy. Across every dimension of the Web3 ecosystem, from DeFi lending and yield farming to cross-border payments and metaverse commerce, stablecoins provide the price stability that makes blockchain-based financial systems practical and accessible for mainstream adoption.

For businesses and individuals in the USA, UK, UAE, and Canada, the stablecoin ecosystem represents a remarkable opportunity to participate in a more efficient, inclusive, and programmable financial system. The challenges of regulation, security, and reserve management are real but manageable with proper diligence and strategic planning.

With 8+ years of experience advising clients at the intersection of blockchain technology and financial operations, we have witnessed the transformation of stablecoins from a theoretical concept to indispensable infrastructure. The stablecoin ecosystem will continue to grow, mature, and integrate more deeply into the global decentralized economy, and those who understand its mechanics and opportunities today will be best positioned to lead in the Web3 economy of tomorrow.

Ready to Build on Stablecoins in Web3?

Our team has 8+ years integrating stablecoin payments, DeFi, and Web3 solutions for businesses in USA, UK, UAE & Canada.

People Also Ask

Q1.What are stablecoins in Web3 and how do they work?

Stablecoins in Web3 are blockchain-based digital assets engineered to maintain a consistent value relative to a reference asset, most commonly the US dollar. They work through three primary mechanisms: fiat collateralization (holding equivalent dollar reserves in a bank), crypto overcollateralization (locking more crypto value than the stablecoin issued), or algorithmic supply control (expanding or contracting token supply programmatically). Because their value does not fluctuate like Bitcoin or Ethereum, they serve as the de facto operating currency of decentralized applications, DeFi protocols, NFT marketplaces, and cross-border payment systems within the broader Web3 economy.

Q2.How do stablecoins support the DeFi ecosystem?

DeFi stablecoins function as the primary liquidity asset across decentralized lending, borrowing, and yield farming platforms. Users deposit stablecoins like USDC or DAI into protocols such as Aave or Compound to earn interest, or borrow against crypto collateral without selling their holdings. This creates a permissionless credit market accessible to anyone with a crypto wallet. Stablecoins also power automated market maker liquidity pools on exchanges like Uniswap and Curve Finance, where their price stability minimizes impermanent loss risk and provides deep, consistent liquidity for the entire decentralized finance ecosystem globally.

Q3.Why are stablecoins important for Web3 adoption?

Web3 adoption has historically been hindered by cryptocurrency price volatility, which makes it impractical for everyday financial transactions. Stablecoins eliminate this barrier by providing a crypto-native asset with predictable value, allowing users to transact, save, and earn within Web3 without speculative risk. For businesses in the USA, UK, UAE, and Canada considering blockchain integration, stablecoins offer a practical entry point that mirrors the stability of fiat currency while delivering the programmability, speed, and borderlessness of blockchain technology. They are effectively the gateway asset that makes Web3 financially accessible to mainstream users.

Q4.What is the difference between fiat-backed and algorithmic stablecoins?

Fiat-backed stablecoins like USDT and USDC maintain their peg by holding equivalent dollar reserves in regulated bank accounts or in safe instruments like US Treasury bills, with the reserves audited by third-party accounting firms. Algorithmic stablecoins, by contrast, use smart contract-based supply mechanisms to maintain their peg, expanding the token supply when price rises above target and contracting it when price falls below. The Terra/LUNA collapse of 2022 demonstrated the catastrophic risk of poorly designed algorithmic models, while fiat-backed stablecoins have maintained their peg far more reliably, making them the dominant choice for enterprise and institutional adoption in the stablecoin ecosystem.

Q5.How do stablecoins enable faster cross-border payments?

Traditional international wire transfers routed through the SWIFT banking network can take 2 to 5 business days to settle, involving multiple correspondent banks and fees of 3 to 7 percent of the transaction value. Stablecoin transfers on blockchain networks like Ethereum, Solana, or Polygon settle in seconds to minutes, with transaction fees typically amounting to fractions of a cent. A business in the UAE paying a supplier in Canada can send USDC directly to a wallet address and have the full dollar-equivalent value arrive instantaneously, with full on-chain verification, no intermediaries, and no currency conversion losses. This represents a paradigm shift in the efficiency of global financial settlements.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.