Ai Overview

New York, January 2026 — In January 2026, the Federal Reserve announced a limited digital dollar pilot program with five commercial banks, triggering an immediate shift in how Fortune 500 treasury departments evaluate payment infrastructure. Early adopters including Microsoft, Visa, and JPMorgan Chase reported 40% efficiency gains in cash management during Q4 2025 earnings calls, creating competitive pressure on peer institutions.

New York, January 2026 — In January 2026, the Federal Reserve announced a limited digital dollar pilot program with five commercial banks, triggering an immediate shift in how Fortune 500 treasury departments evaluate payment infrastructure. Within weeks, CFOs at major corporations accelerated blockchain treasury pilots that had been in planning stages since late 2025, when the SEC published its tokenized securities framework and the Office of the Comptroller of the Currency clarified custody standards for digital assets. This regulatory clarity, combined with central bank infrastructure development, has removed the primary barriers that kept institutional treasurers on the sidelines.

The timing matters because treasury operations have historically lagged technology adoption by five to seven years compared to customer-facing functions. Early adopters including Microsoft, Visa, and JPMorgan Chase reported 40% efficiency gains in cash management during Q4 2025 earnings calls, creating competitive pressure on peer institutions. Cross-border settlement costs dropped 87% when moving from correspondent banking networks to real-time blockchain rails, while trapped liquidity in transit declined from an average 4.2 days to under 30 minutes. Treasury departments at S&P 500 companies collectively manage $3.7 trillion in working capital, meaning even marginal efficiency improvements translate to billions in recaptured value.

Key Takeaways

- Federal Reserve digital dollar pilots and SEC tokenized securities framework catalyze Fortune 500 blockchain treasury adoption in Q1 2026

- Cross-border settlement costs reduced 87% through real-time blockchain rails versus correspondent banking networks

- Working capital management, securities settlement, and FX payments migrate to blockchain infrastructure first

- Compliant implementation requires multi-signature custody, smart contract automation, and hybrid ERP integration architecture

- KYC/AML protocols, regulatory reporting automation, and board governance policies form mandatory compliance framework

Why Fortune 500 Treasurers Are Restructuring Operations Around Blockchain

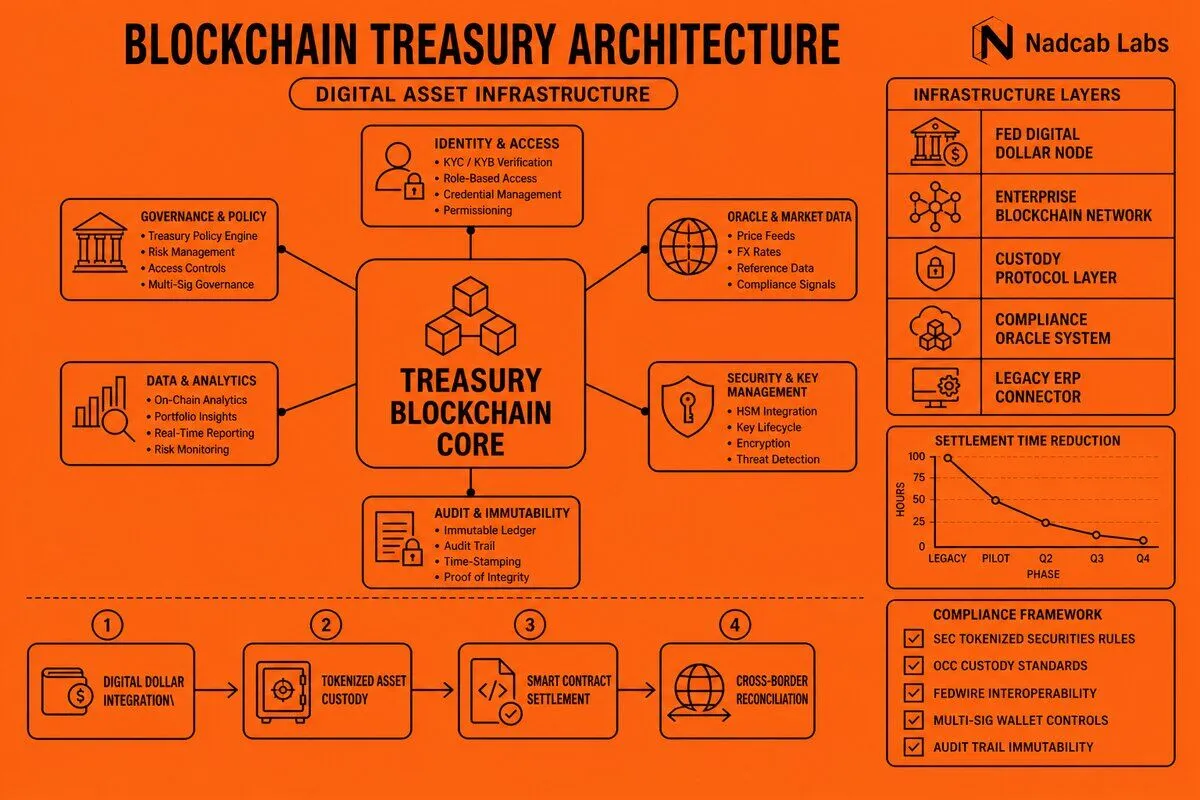

The Federal Reserve’s digital dollar pilot program, announced January 2026, provides institutional-grade infrastructure that treasury departments can integrate with existing banking relationships. Unlike earlier cryptocurrency experiments, the Fed pilot includes API specifications for commercial bank integration, real-time gross settlement finality, and programmable compliance checks embedded in the protocol layer. Five participating banks—JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, and U.S. Bancorp—are building treasury management interfaces that allow corporate clients to move funds between traditional accounts and digital dollar wallets within the same banking relationship.

Cross-border settlement represents the most immediate value driver for blockchain treasury adoption. Traditional correspondent banking networks require 2-5 business days for international payments, with funds locked in transit and exposed to FX volatility during settlement windows. Blockchain-based settlement systems reduce this timeline to under 30 minutes with cryptographic finality, eliminating counterparty risk and reducing working capital requirements. A multinational manufacturer with $800 million in annual cross-border supplier payments can recapture approximately $9.2 million in trapped liquidity by moving to instant settlement rails.

The SEC’s tokenized securities framework, published December 2025, enables compliant on-chain issuance of commercial paper, bonds, and other debt instruments. This regulatory clarity allows treasury departments to issue short-duration securities directly to institutional investors without intermediary dealer networks, reducing issuance costs by 60-75 basis points while improving secondary market liquidity.

Treasury departments recapture significant value through instant settlement and programmable money features. Smart contracts automate cash sweeps, liquidity rebalancing, and investment allocation based on predefined rules, eliminating manual treasury workstation operations that consume 15-20% of treasury staff time. Automated compliance checks embedded in payment rails reduce failed transactions from 2.3% to under 0.1%, saving rework costs and improving vendor relationships.

Competitive pressure accelerates adoption as early movers report material operational improvements. Microsoft disclosed in October 2025 that blockchain treasury infrastructure reduced days sales outstanding by 1.8 days through automated invoice reconciliation and instant payment settlement. Visa reported 40% lower FX hedging costs by eliminating settlement timing uncertainty in cross-border transactions. JPMorgan’s blockchain-based repo platform processed $300 billion in transactions during Q4 2025, demonstrating institutional-scale throughput. For teams exploring Real World Asset Tokenization, these treasury use cases demonstrate how tokenized instruments integrate with corporate finance workflows.

Which Treasury Functions Are Migrating to Blockchain Infrastructure First

Working capital management via stablecoin rails leads blockchain treasury adoption because it addresses immediate pain points in accounts payable and receivables collection. Companies with complex supplier networks—automotive manufacturers, retailers, and technology firms with 5,000+ active vendors—use stablecoin payments to reduce processing costs from $15-25 per wire transfer to under $0.50 per blockchain transaction. Instant settlement eliminates early payment discount programs that cost 2-3% annually, replacing them with same-day payment at par value.

Securities settlement for tokenized commercial paper, repo transactions, and short-duration bonds follows working capital applications because the infrastructure requirements overlap significantly. Treasury departments already using blockchain rails for payments can extend the same custody, compliance, and integration architecture to securities issuance and settlement. Tokenized commercial paper eliminates the dealer network entirely—issuers mint tokens representing debt obligations and sell directly to institutional investors through decentralized exchanges or private placement platforms.

Foreign exchange and cross-border payments replace SWIFT infrastructure with blockchain-based instant settlement networks, particularly for high-volume corridors like USD/EUR, USD/GBP, and USD/CNY. Traditional FX transactions require correspondent banking relationships in each currency jurisdiction, with funds moving through multiple intermediaries over 2-5 business days. Blockchain settlement networks reduce this to under 60 seconds with transparent fee structures and real-time exchange rates.

Reserve asset allocation including 2-5% digital asset holdings reflects updated corporate treasury policies following regulatory clarity and institutional custody infrastructure maturation. Treasury departments traditionally hold reserves in money market funds, short-duration government securities, and bank deposits earning 4-5% yields. Digital asset allocations—primarily stablecoins earning 5-7% yields through DeFi protocols or tokenized treasury securities yielding comparable rates—provide diversification and higher returns within acceptable risk parameters.

Automated cash sweeps and liquidity rebalancing through smart contract treasury management systems eliminate manual treasury workstation operations. Traditional cash management requires treasury analysts to monitor account balances across dozens of bank accounts, manually initiating wire transfers to rebalance liquidity pools and fund investment accounts. Smart contract automation executes these operations based on predefined rules, reducing treasury staff time spent on routine operations by 40-50%. Teams implementing these workflows often reference RWA tokenization smart contract architecture patterns that enable programmable treasury operations.

How CFOs Are Architecting Compliant Tokenized Treasury Workflows

Multi-signature custody with institutional-grade key management forms the foundation of compliant blockchain treasury infrastructure. Platforms like Fireblocks, Anchorage Digital, and Coinbase Prime provide enterprise custody solutions with policy-based approval workflows, hardware security module key storage, and insurance coverage for digital assets. Multi-signature wallets require 3-of-5 or 4-of-7 key holder approval for transactions above materiality thresholds—typically $100,000 for routine payments and $1 million for investment transactions.

Smart contract automation implements approval hierarchies, payment limits, and automated compliance checks that mirror traditional treasury management system controls. Payment smart contracts enforce dual authorization for transactions exceeding $50,000, require CFO approval for amounts over $500,000, and automatically reject transactions to non-whitelisted wallet addresses. Compliance modules integrated into smart contract logic screen transactions against OFAC sanctions lists, verify counterparty KYC status, and flag high-risk jurisdictions for manual review.

API integration layers connect blockchain rails to legacy SAP, Oracle, and Workday ERP systems, maintaining unified general ledger and cash management visibility. Middleware platforms like Baton Systems and Tassat provide pre-built connectors that translate blockchain transactions into standard accounting entries, automatically posting debits and credits to appropriate GL accounts based on transaction metadata.

Hybrid architecture combines permissioned networks for internal operations with public rails for external settlement, optimizing for confidentiality and interoperability simultaneously. Internal treasury operations—inter-company loans, cash pooling, and notional pooling—execute on permissioned blockchains like Hyperledger Besu or R3 Corda where transaction details remain confidential to participants. External payments to suppliers, customers, and financial institutions settle on public stablecoin rails or central bank digital currency networks.

Real-time treasury dashboards aggregate on-chain and traditional positions for unified liquidity visibility, replacing overnight batch reconciliation processes with continuous monitoring. Dashboard interfaces display current balances across all bank accounts, blockchain wallets, money market funds, and short-term investments in a single view, with drill-down capability to transaction-level detail.

Compliance and Risk Frameworks Required for Blockchain Treasury Operations

KYC and anti-money laundering protocols form the first line of defense in blockchain treasury compliance frameworks. Wallet whitelisting restricts outbound transactions to pre-approved counterparty addresses that have completed enhanced due diligence, including beneficial ownership verification, sanctions screening, and business purpose documentation. Transaction screening via Chainalysis, Elliptic, or TRM Labs analyzes blockchain transaction history for connections to sanctioned entities, darknet markets, or mixing services.

Regulatory reporting automation addresses GAAP fair value measurement requirements, IFRS digital asset classification standards, and tax basis tracking for realized gains and losses. Digital assets held in treasury portfolios require daily mark-to-market valuation at fair value, with unrealized gains and losses flowing through other comprehensive income or current period earnings depending on asset classification.

Internal controls frameworks address segregation of duties, dual authorization, and immutable audit trails required by Sarbanes-Oxley and similar corporate governance regulations. Key management policies separate custody functions from transaction initiation and approval, with no single individual holding sufficient keys to execute transactions independently.

Cyber risk management protocols address unique threat vectors in blockchain treasury operations, including private key compromise, smart contract vulnerabilities, and social engineering attacks targeting key holders. Cold storage protocols keep the majority of digital assets offline in hardware wallets stored in bank vaults or secure facilities, accessed only for periodic rebalancing or large transactions. Understanding Blockchain Regulation in 2026: What Every Business Needs to Know helps treasury teams navigate evolving compliance requirements.

Board governance policies define digital asset allocation limits, approved protocols, and risk tolerance parameters that guide treasury decision-making within acceptable boundaries. Typical policies limit digital asset holdings to 2-5% of total reserves, require institutional-grade custody with insurance coverage, and restrict investments to regulated stablecoins or tokenized securities with transparent reserve backing.

Platform Selection: Permissioned Networks vs Public Stablecoin Rails

Permissioned enterprise blockchains like Hyperledger Besu and R3 Corda serve confidential inter-company settlements where transaction privacy matters more than public verifiability. Multinational corporations use permissioned networks for cash pooling arrangements, inter-company loans, and notional pooling structures that consolidate liquidity across subsidiaries while maintaining separate legal entity accounting.

Public stablecoin infrastructure using Circle USDC or Paxos USDP dominates vendor payments and liquidity management applications where broad interoperability and 24/7 availability outweigh privacy concerns. Stablecoins provide dollar-denominated digital currency that settles instantly on public blockchain networks, eliminating correspondent banking delays and reducing transaction costs from $15-25 per wire transfer to under $0.50 per blockchain payment.

Central bank digital currency integration becomes mandatory as Federal Reserve digital dollar pilots expand to commercial participants throughout 2026. The Fed’s wholesale CBDC pilot focuses on interbank settlement and securities transactions initially, with retail CBDC capabilities planned for 2027 deployment. Treasury departments participating in pilot programs integrate CBDC wallets into existing treasury management systems, using digital dollars for same-day tax payments, government contract settlements, and interbank transfers.

Layer-2 scaling solutions including Polygon and Optimism reduce transaction costs while maintaining Ethereum settlement finality for treasury operations requiring public blockchain transparency. Layer-2 networks batch hundreds of transactions into single Ethereum mainnet commitments, reducing per-transaction costs from $5-20 to under $0.10 while preserving cryptographic security and finality guarantees.

Interoperability protocols like Chainlink CCIP and LayerZero enable cross-chain treasury operations and unified liquidity pools spanning multiple blockchain networks. Treasury departments maintain positions across Ethereum, Polygon, Avalanche, and permissioned enterprise networks based on counterparty preferences and transaction requirements. Teams building these capabilities often reference RWA Infrastructure Behind Modern Tokenization Platforms for architectural patterns.

| Treasury Function | Traditional Cost | Blockchain Cost | Savings | Settlement Time |

|---|---|---|---|---|

| Cross-border wire transfer | $25-45 + 3-5% FX spread | $0.50 + 0.1% FX spread | 87% total cost reduction | 2-5 days → 30 minutes |

| Commercial paper issuance | 60-75 basis points | 5-10 basis points | $3-7.5M annually (on $500M program) | T+2 → instant |

| Repo transaction settlement | $150-300 per trade | $2-5 per trade | 98% cost reduction | T+1 → instant |

| Vendor ACH payment | $0.50-1.50 + 2-3 day float | $0.10 + instant settlement | Working capital recapture: 1.8 DSO | 2-3 days → instant |

| FX hedge execution | 2-3% annual hedging cost | 0.5-1% annual hedging cost | 40% lower hedging costs | T+2 → instant |

Conclusion: Strategic Implementation Timeline for Treasury Teams

Fortune 500 treasury departments face a 12-18 month window to implement blockchain infrastructure before competitive disadvantage becomes material. Early adopters reporting 40% efficiency gains and $5-15 million annual savings create board-level pressure on peer companies to accelerate pilot programs and production deployments. The Federal Reserve digital dollar pilot and SEC tokenized securities framework provide regulatory clarity that removes the primary barriers to institutional adoption.

Successful implementation requires phased deployment starting with working capital management and cross-border payments, where value capture is immediate and integration complexity is manageable. Treasury teams should establish governance frameworks, custody relationships, and compliance protocols during pilot phases, then extend the same infrastructure to securities settlement and reserve asset management as operational confidence builds.

Frequently Asked Questions

Q1.What regulatory approvals do Fortune 500 companies need for blockchain treasury operations?

Fortune 500 firms require SEC approval for tokenized securities, FinCEN registration for virtual currency activities, and state money transmitter licenses where applicable. Bank Secrecy Act compliance, OFAC sanctions screening, and SOC 2 Type II attestations are mandatory. Cross-border operations need approval from foreign regulators like FCA or MAS. Internal audit committees must approve blockchain treasury policies before implementation.

Q2.How do CFOs measure ROI on blockchain treasury infrastructure investments?

CFOs track settlement time reduction (typically 72 hours to 10 minutes), FX conversion cost savings (30-60 basis points), and reduced counterparty risk exposure. Key metrics include treasury staff productivity gains, reduced reconciliation errors (often 90%+ reduction), and lower banking fees. Payback periods average 18-24 months for enterprise implementations with transaction volumes exceeding $500M annually.

Q3.Which Fortune 500 companies have publicly disclosed blockchain treasury implementations?

Walmart uses blockchain for cross-border supplier payments across 15 countries. IBM operates a blockchain-based treasury management system processing $2B+ annually. Mastercard disclosed tokenized settlement infrastructure in 2024. Shell and BP have piloted blockchain commodity trading settlements. Microsoft uses distributed ledger technology for royalty payments to partners, though specific treasury volumes remain undisclosed.

Q4.What are the accounting treatment requirements for tokenized treasury assets under GAAP?

Under ASC 820, tokenized assets require fair value measurement with Level 1, 2, or 3 classification based on market observability. Stablecoins typically classify as cash equivalents if redeemable within 90 days. Tokenized securities follow existing investment accounting (ASC 320/321). Companies must disclose custody arrangements, smart contract risks, and valuation methodologies in footnotes per ASC 825.

Q5.How do blockchain treasury systems integrate with existing bank relationships and credit facilities?

Integration occurs through API connections between blockchain nodes and bank treasury workstations, maintaining existing SWIFT/FedWire rails as fallback. Banks provide custodial wallets with multi-signature controls tied to credit facility covenants. Real-time blockchain data feeds into cash concentration accounts. Most implementations use hybrid models where blockchain handles internal transfers while banks manage external regulatory reporting and credit line draws.

Explore Services