Ai Overview

These traditional assets have historically been the cornerstone of global wealth, representing trillions of dollars in value across residential properties, corporate bonds, equity stakes, natural resources, and intellectual property rights. A luxury apartment in Dubai valued at $5 million can be divided into 50,000 tokens, each representing a $100 ownership stake, making previously exclusive assets accessible to ordinary investors.

Key Takeaways

- Real world asset tokenization converts physical and traditional financial assets into blockchain-based digital tokens, enabling fractional ownership, enhanced liquidity, and 24/7 global trading across international markets including USA, UK, UAE, and Canada.

- The tokenized real estate market enables property investment with minimums as low as $100 to $1,000, compared to traditional requirements of $100,000 or more, democratizing access to high-value commercial and residential properties.

- Tokenized commodities like gold, silver, and oil provide instant settlement and fractional ownership, eliminating storage costs, insurance requirements, and the logistical complexities associated with physical commodity trading and ownership.

- Government bonds and treasury assets tokenization reduces settlement times from 2-3 days to minutes while maintaining regulatory compliance, attracting institutional investors seeking efficient fixed-income exposure with blockchain transparency benefits.

- Smart contracts automate compliance verification, dividend distributions, and transfer restrictions in tokenized assets, reducing administrative overhead by up to 90% while ensuring consistent application of regulatory requirements across jurisdictions.

- The global tokenized asset market is projected to reach $16 trillion by 2030, driven by institutional adoption, regulatory clarity improvements, and infrastructure development from established financial institutions and blockchain technology providers.

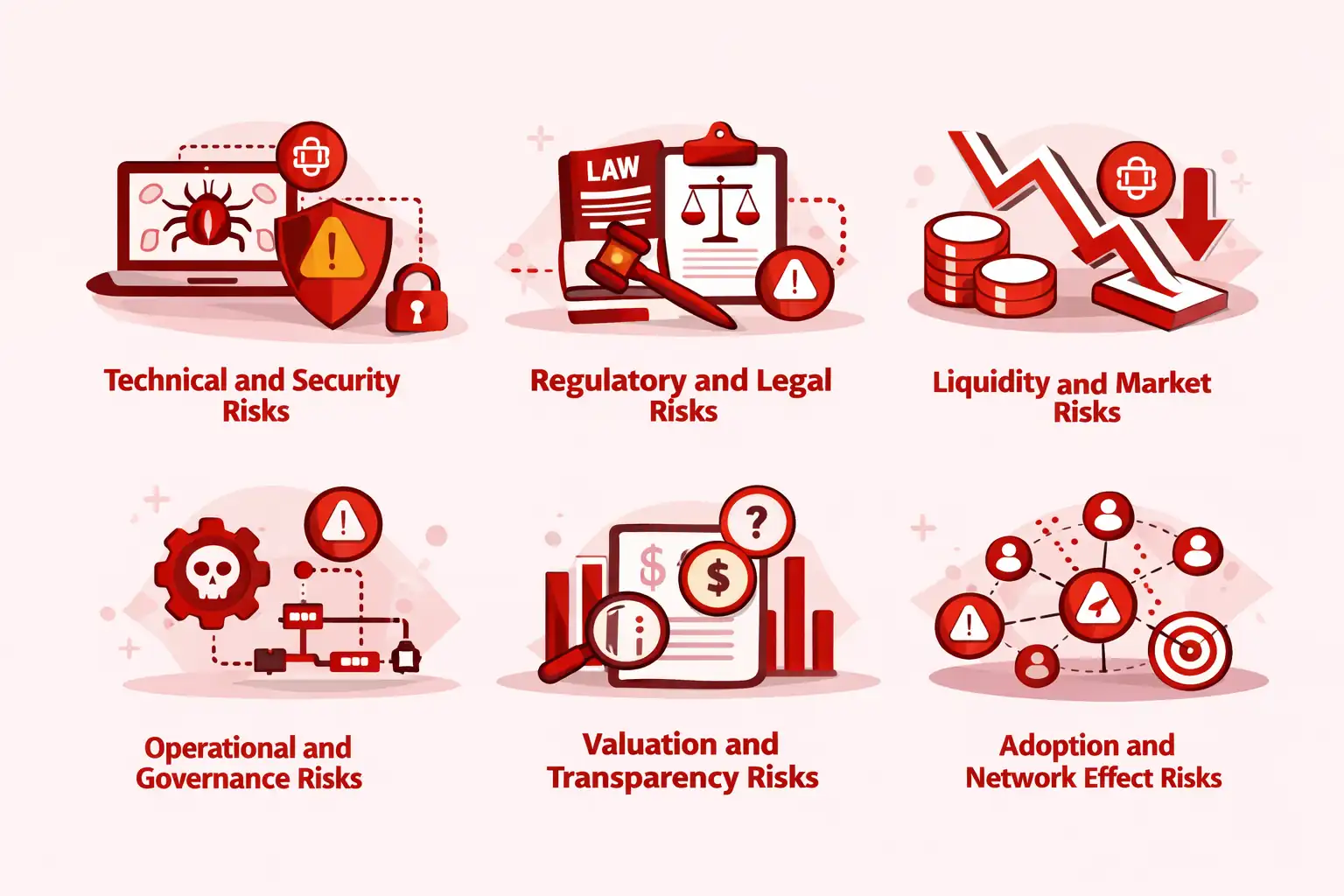

- Key regulatory challenges include navigating securities laws across multiple jurisdictions, implementing robust KYC/AML procedures, ensuring legal recognition of blockchain ownership records, and addressing cross-border tax implications for international token holders.

- Institutional-grade custody solutions, multi-signature wallets, and insurance coverage are essential security measures protecting tokenized assets from smart contract vulnerabilities, operational failures, and unauthorized access attempts by malicious actors.

What Are Real World Assets (RWAs) in Blockchain Tokenization?

Real-world assets represent tangible and intangible assets that exist outside the digital blockchain ecosystem, encompassing everything from commercial real estate properties and government securities to fine art collections and agricultural commodities. These traditional assets have historically been the cornerstone of global wealth, representing trillions of dollars in value across residential properties, corporate bonds, equity stakes, natural resources, and intellectual property rights. The challenge with these assets has always been their illiquidity, high transaction costs, geographic limitations, and barriers to entry that exclude the majority of potential investors from participation.

Blockchain tokenization transforms these physical and traditional financial assets into digital tokens that exist on distributed ledger networks, creating programmable representations of ownership rights that can be transferred, traded, and managed through smart contracts. This digital transformation does not replace the underlying asset but rather creates a more efficient mechanism for representing ownership, transferring title, and accessing liquidity. A tokenized office building in Manhattan, for example, remains a physical structure, but ownership interests are represented by digital tokens that can be traded globally on blockchain platforms rather than through traditional real estate transactions requiring extensive legal documentation, escrow services, and weeks or months of settlement time.

The tokenization process involves several critical steps that bridge traditional asset ownership with blockchain technology. First, the asset undergoes thorough valuation and due diligence by qualified professionals to establish fair market value and verify legal title. Second, a legal structure is established, typically through a special purpose vehicle or trust, that holds legal title to the asset while issuing tokens representing beneficial ownership interests. Third, smart contracts are deployed on a blockchain network encoding the ownership rules, transfer restrictions, compliance requirements, and economic rights associated with the tokens. Finally, the tokens are distributed to investors through compliant offering mechanisms and can be traded on secondary markets subject to applicable regulations.

Core Categories of Real World Assets Eligible for Tokenization

Tangible Physical Assets

Commercial and residential real estate, agricultural land, precious metals, commodities, fine art, luxury goods, collectibles, infrastructure assets, and natural resources with quantifiable market value.

Traditional Financial Instruments

Government bonds, corporate debt securities, treasury bills, private equity stakes, venture capital investments, hedge fund shares, structured products, and derivative contracts requiring regulatory compliance.

Intangible Assets and Rights

Intellectual property including patents and trademarks, music and film royalties, carbon credits, renewable energy certificates, revenue streams from businesses, and licensing rights with demonstrable economic value.

With over eight years of experience facilitating real-world asset tokenization projects across USA, UK, UAE, and Canada, our agency has observed that the most successful implementations share common characteristics: clear legal frameworks establishing token holder rights, robust compliance mechanisms addressing securities regulations, transparent governance structures enabling investor participation, and realistic liquidity expectations accounting for market development stages. Assets with stable valuations, established track records, and strong demand from retail and institutional investors tend to achieve successful tokenization outcomes with active secondary market trading.

The distinction between tokenized real-world assets and native cryptocurrencies is fundamental to understanding this market segment. While cryptocurrencies like Bitcoin or Ethereum are digital-native assets deriving value from network effects, utility, or speculative demand, tokenized RWAs derive their value from underlying physical or financial assets with intrinsic worth. This connection to real-world value provides different risk-return profiles, regulatory treatment, and investor appeal compared to pure cryptocurrency investments. Tokenized assets typically exhibit lower volatility, generate income streams from underlying asset performance, and offer exposure to traditional asset classes through blockchain-enabled infrastructure.

Why Tokenization Is Reshaping Traditional Asset Ownership

Traditional asset ownership has operated under fundamentally unchanged paradigms for centuries, characterized by high friction, intermediary dependence, geographic constraints, and exclusionary minimum investment requirements that concentrate wealth among institutions and high-net-worth individuals. A commercial real estate transaction in London, for example, requires extensive involvement from brokers, lawyers, surveyors, escrow agents, and registrars, with fees consuming 3% to 6% of transaction value and settlement periods extending weeks or months. These inefficiencies create significant drag on capital allocation, reduce liquidity, and prevent efficient price discovery across asset markets.

Tokenization fundamentally disrupts these inefficiencies by eliminating intermediaries, automating compliance processes, enabling fractional ownership, and creating global markets accessible 24/7 from any internet-connected device. Smart contracts replace escrow agents, title companies, and transfer agents, executing transactions automatically when predefined conditions are met without human intervention. Blockchain networks provide transparent, immutable records of ownership and transaction history, reducing due diligence costs and fraud risks. The programmability of tokens enables sophisticated features like automated dividend distributions, governance voting, and compliance enforcement that would be impractical or cost-prohibitive using traditional mechanisms.

The fractional ownership enabled by tokenization represents perhaps the most transformative aspect of this technology. A luxury apartment in Dubai valued at $5 million can be divided into 50,000 tokens, each representing a $100 ownership stake, making previously exclusive assets accessible to ordinary investors. This fractionalization does not dilute value but rather expands the investor base, potentially increasing overall demand and asset valuations. Investors can diversify across multiple tokenized properties, bonds, or commodities with capital amounts that would have purchased minimal exposure through traditional channels, fundamentally democratizing access to wealth-building asset classes.

Liquidity enhancement stands as another critical benefit driving tokenization adoption across markets in USA, UK, UAE, and Canada. Traditional real estate investments, for instance, suffer from extreme illiquidity, with property sales requiring months of marketing, negotiation, due diligence, and legal processing. Tokenized real estate creates continuous markets where ownership interests can be traded instantly at prevailing market prices, similar to publicly traded securities. While secondary market liquidity for tokenized assets remains nascent compared to mature equity markets, the infrastructure development and regulatory clarification occurring across major jurisdictions are gradually improving trading volumes and price discovery mechanisms.

Transparency represents another fundamental advantage of blockchain-based asset ownership. All transactions, ownership changes, and corporate actions are recorded on distributed ledgers visible to all network participants, creating unprecedented auditability and reducing information asymmetries between asset managers and investors. This transparency extends to asset performance metrics, income distributions, and compliance activities, enabling investors to verify claims independently rather than relying solely on intermediary reporting. The immutability of blockchain records prevents retroactive manipulation or record alteration, building trust and reducing fraud risks that plague traditional systems.

Our experience implementing tokenization projects reveals that successful market transformation requires more than just technical blockchain deployment. Legal frameworks must be established providing clarity on token holder rights, obligations, and remedies. Regulatory compliance must be embedded into token smart contracts and platform operations from inception rather than retrofitted later. Market infrastructure including custody solutions, trading venues, and price discovery mechanisms must achieve institutional-grade security and reliability. Education initiatives must address investor understanding of tokenized assets, their risks, and their differences from both traditional assets and cryptocurrencies.

How Real-World Asset Tokenization Works (Simple Overview)

The tokenization process transforms traditional assets into blockchain-based digital representations through a systematic workflow combining legal structuring, technical implementation, regulatory compliance, and market distribution. Understanding this process is essential for asset owners, investors, and service providers participating in tokenized asset markets. While specific implementations vary based on asset type, jurisdiction, and platform choice, the fundamental workflow follows consistent patterns refined through years of market development and regulatory evolution.

Complete Tokenization Lifecycle: From Asset to Token

Step 1: Asset Selection and Valuation

Asset owners identify properties, securities, or commodities suitable for tokenization based on liquidity goals, investor demand, and regulatory feasibility. Independent valuation experts conduct appraisals using comparable transactions, discounted cash flow analysis, or market-based approaches to establish fair market value. Legal due diligence verifies clear title, absence of liens or encumbrances, and compliance with applicable regulations.

Timeline: 2-4 weeks for straightforward assets, 8-12 weeks for complex structures

Step 2: Legal Structure Implementation

A special purpose vehicle, trust, or holding company is established to hold legal title to the underlying asset. Token holders receive beneficial ownership interests or economic rights defined in offering documents and governing agreements. Legal counsel drafts subscription agreements, token holder agreements, and disclosure documents addressing securities regulations, investor protections, and dispute resolution mechanisms.

Key Consideration: Structure must comply with securities laws in all jurisdictions where tokens will be offered

Step 3: Smart Contract Development and Blockchain Deployment

Blockchain developers create smart contracts encoding ownership rules, transfer restrictions, compliance requirements, and economic rights. Token standards like ERC-20 or ERC-1400 provide standardized interfaces ensuring interoperability with wallets and exchanges. Smart contracts undergo security audits by third-party specialists to identify vulnerabilities before mainnet deployment. Tokens are minted and allocated to the issuing entity for distribution.

Critical Requirement: Comprehensive security audits prevent exploits that could compromise token holder funds

Step 4: Regulatory Compliance and KYC/AML Integration

Issuers implement know-your-customer and anti-money laundering procedures verifying investor identities, accreditation status, and geographic eligibility. Compliance systems integrate with smart contracts to enforce transfer restrictions based on regulatory requirements. Ongoing monitoring tracks token holders for sanctions screening and suspicious activity reporting. Regulatory filings are completed with securities commissions or financial authorities as required by jurisdiction.

Compliance Principle: Better to over-engineer compliance than face enforcement actions later

Step 5: Token Offering and Distribution

Marketing materials are prepared following securities regulations regarding permissible claims and disclosures. Investors subscribe for tokens through compliant offering platforms requiring identity verification and investor suitability assessments. Funds are collected in escrow accounts and tokens are distributed to investor wallets after closing conditions are satisfied. Offering proceeds are transferred to the special purpose vehicle to manage the underlying asset.

Distribution Timeline: Primary offerings typically range from 30 days to 6 months depending on target raise

Step 6: Ongoing Asset Management and Secondary Trading

Asset managers oversee underlying property operations, investment performance, and income generation. Smart contracts automatically distribute dividends, interest, or rental income to token holders based on ownership percentages. Secondary market platforms enable token trading subject to transfer restrictions and compliance requirements. Regular reporting provides transparency on asset performance, financial statements, and material events affecting valuations.

Ongoing Obligation: Continuous compliance monitoring and investor communication throughout asset lifecycle

The technical infrastructure supporting tokenization extends beyond smart contracts to encompass custody solutions, oracle networks, and interoperability protocols. Institutional-grade custodians provide secure storage for tokens using multi-signature wallets, hardware security modules, and segregated key management preventing unauthorized access. Oracle networks feed real-world data like asset valuations, rental income, or commodity prices into smart contracts enabling automated decision-making based on external events. Cross-chain bridges and wrapped tokens facilitate trading across different blockchain networks, expanding liquidity and investor access.

Blockchain selection represents a critical decision impacting transaction costs, scalability, security, and regulatory positioning. Ethereum dominates tokenized asset deployments due to its mature smart contract ecosystem, extensive developer tooling, and institutional adoption. However, competing platforms like Polygon, Avalanche, and Stellar offer lower transaction fees and higher throughput potentially better suited for high-frequency trading or microtransaction applications. Private or permissioned blockchains provide greater control over network participants and transaction visibility, appealing to institutions requiring confidentiality or regulatory oversight.

Throughout our eight years facilitating tokenization projects, we have identified common pitfalls that undermine project success. Insufficient legal planning creates ambiguity about token holder rights and remedies, leading to disputes and regulatory scrutiny. Inadequate security audits expose vulnerabilities that malicious actors exploit, resulting in token theft or smart contract manipulation. Poor market infrastructure planning leaves tokens stranded without viable trading venues or price discovery mechanisms. Unrealistic liquidity expectations disappoint investors who assumed tokenization alone would create active secondary markets regardless of underlying asset quality or market conditions.

Top 6 Tokenized Real-World Assets

The tokenization movement has gained traction across diverse asset classes, with certain categories demonstrating particularly strong product-market fit, regulatory acceptance, and investor demand. These leading use cases showcase the versatility of blockchain technology in transforming traditional assets while highlighting the unique value propositions that tokenization delivers for different asset types. Understanding these top categories provides insight into where the market is heading and which opportunities present the greatest potential for investors, asset owners, and service providers operating across USA, UK, UAE, and Canada.

Each asset class presents distinct advantages and challenges for tokenization, requiring tailored approaches to legal structuring, technical implementation, and market development. Real estate benefits from stable cash flows and familiar investor dynamics but faces complex property law considerations. Commodities offer simple valuation and established markets but require physical storage and insurance coordination. Financial securities align naturally with existing regulatory frameworks but must navigate securities law complexities across jurisdictions. The most successful tokenization projects recognize these nuances and design solutions specifically addressing each asset class’s unique characteristics rather than applying generic one-size-fits-all approaches.

Leading Real-World Asset Categories Driving Tokenization Adoption

1. Tokenized Real Estate

- Commercial and residential property fractional ownership

- Minimums from $100 to $1,000 vs. $100,000+ traditionally

- Automated rental income distribution via smart contracts

- Global investor access to international property markets

- Reduced transaction costs and settlement timeframes

2. Tokenized Commodities

- Gold, silver, platinum, and precious metals exposure

- Oil, natural gas, and energy commodity tokenization

- Agricultural products including grains and livestock

- Eliminates physical storage and insurance costs

- Instant settlement replacing weeks of logistics

3. Tokenized Bonds

- Government bonds and treasury securities on blockchain

- Corporate debt instruments with programmable features

- Settlement in minutes vs. 2-3 days traditionally

- Fractional access to institutional-grade fixed income

- Automated coupon payments via smart contracts

4. Private Equity and Venture Capital

- Startup equity stakes accessible to retail investors

- Venture capital fund shares with enhanced liquidity

- Secondary markets for illiquid private investments

- Automated cap table management and distributions

- Reduced minimums democratizing alternative investments

5. Art, Collectibles, and Luxury Assets

- Fine art masterpieces owned by multiple investors

- Rare collectibles including cars, watches, and wine

- Luxury handbags and fashion items tokenization

- Provenance tracking preventing counterfeits

- Previously exclusive markets opened to broader participation

6. Carbon Credits and Environmental Assets

- Verified carbon offset credits on blockchain

- Renewable energy certificates and attributes

- Transparent tracking preventing double-counting

- Enhanced liquidity for environmental commodities

- Connecting climate projects with global capital

Market data demonstrates significant growth trajectories across these asset categories, with tokenized real estate leading adoption metrics followed by fixed income securities and commodities. According to industry analysis, the total value of tokenized real-world assets reached approximately $150 billion in 2024, with projections suggesting growth to $16 trillion by 2030 as institutional adoption accelerates, regulatory frameworks mature, and infrastructure improves. This growth is driven by demand from both retail investors seeking access to previously exclusive assets and institutional investors pursuing operational efficiencies, cost reductions, and new revenue opportunities.

Geographic distribution of tokenization activity reflects regulatory environments, financial market development, and technological infrastructure availability. The United States leads in tokenized asset volume with established exemptions like Regulation D and Regulation A+ providing compliant pathways for securities tokenization. The United Kingdom has developed comprehensive regulatory approaches through the Financial Conduct Authority, encouraging innovation while maintaining investor protections. The UAE, particularly Dubai, has emerged as a tokenization hub with progressive regulations attracting international issuers and investors. Canada balances innovation support with prudent regulation, creating opportunities within clear legal frameworks.

Tokenized Real Estate: Fractional Property Ownership at Scale

Real estate tokenization represents the most mature and widely adopted application of blockchain technology to traditional assets, driven by the industry’s chronic inefficiencies, high capital requirements, and geographic barriers that have historically limited participation to institutions and wealthy individuals. The global real estate market exceeds $280 trillion in value, yet remains plagued by illiquidity, high transaction costs, opaque pricing, and lengthy settlement periods that create friction for buyers, sellers, and investors. Tokenization addresses these pain points by fractionalizing property ownership, automating compliance and income distribution, and creating secondary markets that enhance liquidity for an asset class traditionally characterized by extreme illiquidity.

The fundamental value proposition of tokenized real estate lies in democratizing access to commercial-grade properties that generate stable income streams and appreciation potential. A Class A office tower in Manhattan valued at $50 million might be divided into 500,000 tokens at $100 each, enabling retail investors to gain exposure to institutional-quality real estate with capital amounts that would traditionally purchase minimal ownership stakes through REITs with higher fees and less direct property exposure. Token holders receive proportional rental income distributions automatically via smart contracts, vote on major property decisions based on ownership percentages, and can sell tokens on secondary markets without the complexities of traditional property transactions.

| Feature | Traditional Real Estate Investing | Tokenized Real Estate |

|---|---|---|

| Minimum Investment | $100,000 to $500,000+ for direct ownership; $1,000 to $5,000 for REITs | $100 to $1,000 for fractional property tokens |

| Transaction Costs | 3% to 6% of transaction value for brokers, lawyers, title insurance | 0.5% to 2% platform fees plus minimal blockchain gas fees |

| Settlement Time | 30 to 90 days for due diligence, financing, legal processing | Minutes to hours for token transfers on blockchain |

| Liquidity Options | Extremely limited; property sales require months of marketing | Secondary market trading with varying liquidity by platform |

| Geographic Access | Limited to local markets or through high-fee international funds | Global access to international properties from any location |

| Income Distribution | Quarterly or annual distributions with manual processing | Monthly or quarterly automated distributions via smart contracts |

| Transparency | Dependent on property manager reporting; limited auditability | Full transaction history on blockchain; transparent ownership records |

| Diversification Capability | Difficult due to high minimums; concentrated positions common | Easy diversification across multiple properties and geographies |

Several property types have emerged as particularly suitable for tokenization based on cash flow stability, valuation transparency, and investor familiarity. Commercial office buildings generate predictable rental income from creditworthy corporate tenants under long-term leases, providing stable returns attractive to income-focused investors. Multi-family residential complexes benefit from diversified tenant bases and steady demand, reducing vacancy risks compared to single properties. Industrial and logistics facilities have gained popularity due to e-commerce growth driving warehouse demand and reliable lease structures. Luxury vacation properties in markets like Dubai, Miami, and London offer tokenized fractional ownership combining investment returns with usage rights for token holders.

Legal structuring for tokenized real estate requires careful attention to securities regulations, property law, and tax considerations across relevant jurisdictions. Most projects utilize special purpose vehicles owning legal title to properties while issuing tokens representing beneficial interests or profit participation rights. This structure separates blockchain token ownership from traditional property registries, avoiding challenges of integrating blockchain records into government land registry systems. Token holder agreements define voting rights, income distribution mechanisms, property management responsibilities, and exit strategies ensuring alignment between digital token ownership and real-world property rights.

Our agency has facilitated tokenization for commercial properties across USA, UK, UAE, and Canada, observing that successful projects share common characteristics: high-quality assets in prime locations, experienced property management teams, conservative leverage ratios, and realistic projections about secondary market liquidity. Properties with complex title issues, heavy debt burdens, or uncertain cash flows face challenges attracting investors regardless of tokenization benefits. The technology enables fractional ownership but cannot overcome fundamental asset quality problems or market fundamentals affecting property values.

Regulatory treatment of tokenized real estate varies significantly across jurisdictions, with most authorities classifying property tokens as securities subject to registration requirements or exemptions. In the United States, issuers typically rely on Regulation D for private placements to accredited investors or Regulation A+ for broader offerings with disclosure requirements. The UK applies existing securities frameworks through the Financial Conduct Authority, requiring authorization for platforms facilitating property token issuance or trading. The UAE has developed specific regulations for digital assets including real estate tokens, with Dubai establishing dedicated free zones encouraging tokenization innovation. Canada applies provincial securities laws requiring compliance with prospectus requirements or available exemptions.

Tokenized Commodities: Gold, Silver, and Physical Resources

Commodity tokenization transforms physical resources into blockchain-based digital assets providing ownership claims on gold bars stored in vaults, barrels of oil in strategic reserves, or agricultural products in warehouses. This application addresses longstanding challenges in commodity markets including high storage costs, insurance requirements, transportation logistics, verification complexities, and minimum purchase quantities that exclude retail participants from direct commodity ownership. Tokenized commodities combine the inflation hedging and diversification benefits of physical resources with the convenience, divisibility, and instant settlement characteristics of digital assets.

Precious metals, particularly gold and silver, represent the most established commodity tokenization category due to their standardized quality specifications, established pricing mechanisms, and centuries-long history as stores of value and portfolio diversifiers. Each token represents ownership of a specific quantity of physical metal, typically one gram or one troy ounce, stored in audited vaults operated by qualified custodians. Token holders avoid storage fees, insurance costs, and security concerns associated with physical possession while maintaining claims on real metal redeemable for physical delivery if desired. The tokens trade continuously on digital exchanges, providing liquidity that physical metal ownership lacks.

Energy commodities including crude oil, natural gas, and refined petroleum products present unique tokenization opportunities addressing inefficiencies in energy markets. Traditional energy trading involves complex futures contracts, physical delivery logistics, and infrastructure constraints limiting market participation to specialized trading firms and energy companies. Tokenized energy commodities enable retail investors to gain exposure to oil price movements without navigating futures contract rollovers, contango effects, or physical delivery obligations. The tokens represent ownership claims on barrels stored in strategic petroleum reserves or terminal facilities, with custodians managing storage and quality verification.

Agricultural commodities including grains, livestock, and soft commodities like coffee and cocoa have begun adopting tokenization despite unique challenges related to product perishability, quality variability, and seasonal production cycles. Tokens may represent ownership of grain stored in certified warehouses, livestock in managed feeding operations, or forward purchase contracts with producers. These structures provide farmers with upfront capital while offering investors exposure to agricultural commodity prices and potential supply chain financing returns. Smart contracts can automate quality inspections, insurance claims, and delivery logistics based on oracle data feeds from sensors and inspection services.

Industrial metals including copper, aluminum, and nickel represent significant tokenization opportunities given their importance to manufacturing, construction, and energy transition applications. Battery metals like lithium, cobalt, and nickel are particularly attractive due to electric vehicle demand growth and renewable energy storage requirements. Tokenization enables direct investment in physical metal inventories rather than through mining company equities or commodity futures, providing purer commodity price exposure. The challenge involves establishing secure custody arrangements with reputable warehouses and implementing verification systems ensuring physical metal matches token supply.

Regulatory treatment of tokenized commodities generally falls under commodity regulations rather than securities laws, though specific classifications depend on token structure and investor rights. The US Commodity Futures Trading Commission regulates commodity derivatives while physical commodity ownership may be less regulated. However, tokens structured as investment contracts with expectation of profits from issuer efforts may trigger securities classification. Our experience across USA, UK, UAE, and Canada demonstrates that proactive engagement with regulators clarifying token structure and business model reduces enforcement risks and facilitates market development.

Critical success factors for commodity tokenization include reputable custodians with established track records, regular third-party audits verifying physical holdings, comprehensive insurance coverage protecting against theft or loss, clear redemption procedures enabling physical delivery, and transparent fee structures avoiding hidden charges. Projects failing on these dimensions face investor skepticism, regulatory scrutiny, and potential fraud allegations. The physical-digital bridge requires robust operational processes ensuring blockchain records accurately reflect real-world commodity holdings at all times.

Tokenized Bonds and Treasury Assets

Fixed income securities including government bonds, treasury bills, and corporate debt instruments represent a natural fit for blockchain tokenization given their standardized structures, established valuation methodologies, and massive market sizes exceeding $130 trillion globally. Traditional bond markets suffer from settlement delays, high minimum denominations, opaque pricing for retail investors, and limited secondary market access for smaller participants. Tokenization addresses these inefficiencies by enabling instant settlement, fractional ownership, transparent pricing, and continuous trading on digital exchanges accessible to retail and institutional investors worldwide.

Government bonds and treasury securities issued by USA, UK, UAE, Canada, and other sovereign nations provide low-risk, stable income streams backing tokenized offerings that attract conservative investors seeking alternatives to bank deposits with higher yields. Several financial institutions and blockchain platforms have launched tokenized treasury products allowing investors to purchase fractional interests in US Treasury bills or UK gilts with minimums as low as $1. Smart contracts automatically distribute interest payments based on coupon rates and ownership percentages, eliminating manual processing and reducing administrative overhead. Settlement occurs in minutes rather than the 2-3 day standard for traditional bond transactions, improving capital efficiency and reducing counterparty risk.

| Bond Type | Tokenization Benefits | Implementation Considerations |

|---|---|---|

| Government Treasury Securities | Instant settlement, fractional ownership from $1, automated interest distributions, 24/7 trading access, transparent pricing, reduced intermediary costs | Regulatory approval processes, custodian selection for underlying securities, smart contract audits, KYC/AML compliance, tax reporting integration |

| Corporate Bonds | Enhanced liquidity for illiquid issues, lower issuance costs, programmable covenant enforcement, automatic credit rating updates, real-time market data | Securities law compliance, issuer cooperation, rating agency integration, default handling procedures, investor communication systems |

| Municipal Bonds | Broader investor access, reduced issuance costs for municipalities, tax-exempt income automation, transparent project tracking, simplified refinancing processes | State and local regulations, tax documentation requirements, project performance monitoring, voter approval processes, municipal cooperation |

| Asset-Backed Securities | Transparent collateral tracking, automated cash flow distribution, reduced servicing costs, real-time performance data, simplified waterfall calculations | Collateral verification systems, servicer integration, rating methodology adaptation, regulatory capital treatment, investor reporting automation |

| Green Bonds | Environmental impact tracking, transparent fund allocation, automated sustainability reporting, enhanced investor trust, simplified green certification | Impact measurement integration, certification authority coordination, oracle network design for environmental data, stakeholder communication platforms |

Corporate debt tokenization enables companies to access broader investor bases while reducing issuance costs associated with traditional bond offerings. A mid-sized corporation might tokenize a $10 million bond offering with $100 minimum investments rather than traditional $1,000 or $5,000 denominations, dramatically expanding the potential investor pool. Smart contracts encode bond covenants, automatically monitoring compliance with financial ratios, restriction on additional debt, or dividend limitations. Covenant breaches trigger immediate notifications to token holders and potentially automatic remedies like interest rate increases or trading restrictions, providing stronger protections than traditional monitoring mechanisms requiring manual oversight.

Municipal bonds financing infrastructure projects for cities and states present compelling tokenization opportunities given their tax-advantaged status, public interest orientation, and need for efficient capital markets. Tokenized municipal bonds could enable direct citizen investment in local infrastructure while reducing issuance costs that burden public budgets. Smart contracts can link interest payments to project milestones or revenue generation, aligning investor returns with project success. Transparent blockchain records provide taxpayers with visibility into how bond proceeds are deployed and whether projects meet performance expectations, potentially increasing public support for infrastructure financing.

Asset-backed securities including mortgage-backed securities, auto loan securitizations, and credit card receivable structures benefit significantly from tokenization’s transparency and automation capabilities. Traditional securitizations involve complex waterfall structures distributing cash flows across multiple tranches with different risk-return profiles, requiring extensive administrative overhead and offering limited transparency to investors. Tokenized structures encode waterfall logic into smart contracts, automatically distributing payments based on collateral performance with full auditability. Investors can verify underlying collateral characteristics, delinquency rates, and prepayment speeds directly rather than relying solely on servicer reports, reducing information asymmetries and improving pricing efficiency.

Our agency’s experience implementing tokenized bond offerings across multiple jurisdictions reveals that regulatory compliance remains the primary challenge and success factor. Securities regulations apply to most tokenized bonds regardless of blockchain deployment, requiring registration statements or reliance on exemptions with associated disclosure and reporting obligations. Transfer restrictions must be embedded into smart contracts preventing transfers to ineligible investors or jurisdictions. Tax reporting requirements necessitate integration with existing infrastructure capturing interest income, original issue discount calculations, and capital gains or losses for regulatory submissions.

Institutional adoption of tokenized bonds has accelerated as major financial institutions recognize efficiency gains and cost reductions. Several European banks have issued tokenized bonds raising hundreds of millions of dollars, demonstrating scalability and regulatory feasibility. These offerings typically utilize private blockchains or permissioned networks providing confidentiality and regulatory oversight while maintaining blockchain’s efficiency benefits. As infrastructure matures and regulatory frameworks clarify, tokenized bonds are positioned to capture increasing market share from traditional fixed income issuance, particularly for smaller offerings where traditional costs are prohibitively high.

Tokenized Private Equity and Venture Capital Assets

Private equity and venture capital investments have historically remained accessible only to institutional investors and high-net-worth individuals due to extreme minimum investment requirements, extensive lock-up periods, and regulatory restrictions limiting participation to accredited investors. Traditional private equity funds require commitments of $250,000 to $5 million, with capital locked up for 7-10 years and minimal secondary market liquidity. Tokenization fundamentally disrupts this exclusivity by enabling fractional ownership of private equity stakes, venture capital fund shares, or direct startup equity with dramatically reduced minimums and enhanced liquidity through secondary token markets.

The value proposition extends beyond democratized access to include operational efficiencies that benefit fund managers, portfolio companies, and investors. Cap table management, historically a manual process prone to errors and disputes, becomes automated through blockchain records providing real-time visibility into ownership structure. Investor communications including capital calls, distribution notices, and performance reports can be delivered automatically to token holders based on their ownership percentages. Voting rights for portfolio company decisions are programmed into tokens, enabling proportional governance participation without the administrative burden of tracking proxy votes and consent solicitations.

Tokenized Private Market Investment Models

Direct Startup Equity Tokens

- Companies issue tokenized shares directly to investors

- Smart contracts manage cap tables and vesting schedules

- Automated dividend or profit distribution mechanisms

- Secondary markets enable early liquidity before IPO or acquisition

- Minimums reduced from $25,000+ to $100 to $1,000

Tokenized Fund Shares

- Venture capital or private equity funds issue tokenized LP interests

- Fractional ownership reduces minimums from $250,000+ to $5,000+

- Enhanced liquidity through secondary token trading

- Automated capital calls and distribution processing

- Transparent portfolio company performance tracking

Secondary Market Platforms

- Existing private equity stakes converted to tokens

- Early employees and angel investors gain liquidity

- Price discovery through continuous trading

- Compliance-integrated platforms enforce transfer restrictions

- Connects buyers seeking private company exposure with sellers needing exits

Tokenized Syndicates and SPVs

- Special purpose vehicles pool capital for single investments

- Lead investors curate opportunities for follow-on participants

- Tokens represent beneficial interests in SPV holdings

- Lower minimums democratize access to curated deal flow

- Transparent tracking of investment performance and exits

Regulatory considerations for tokenized private equity and venture capital remain complex, with securities laws strictly governing private placement offerings and restricting participation to accredited investors or sophisticated purchasers in most jurisdictions. While tokenization technology enables fractional ownership and enhanced liquidity, it does not eliminate accreditation requirements or suitability standards designed to protect unsophisticated investors from high-risk, illiquid investments. Most tokenized private equity offerings rely on Regulation D exemptions in the United States, requiring verification of investor accreditation status and limiting general solicitation and advertising.

Secondary market development for tokenized private equity represents both the greatest opportunity and most significant challenge. Traditional private equity secondary markets are inefficient, with transactions occurring sporadically at significant discounts to net asset value due to information asymmetries, due diligence costs, and limited buyer pools. Tokenized secondary markets promise continuous pricing, lower transaction costs, and broader participation, but face challenges related to transfer restrictions, valuation uncertainty for illiquid portfolios, and regulatory compliance for broker-dealer activities. Platforms facilitating secondary token trading must navigate alternative trading system regulations or broker-dealer licensing requirements depending on their operational model.

Portfolio companies and fund managers must carefully evaluate whether tokenization aligns with their strategic objectives and investor relations capabilities. The transparency inherent in blockchain systems may be uncomfortable for companies accustomed to confidential operations with limited disclosure requirements. Managing a diverse base of small token holders requires different capabilities than servicing a concentrated group of sophisticated institutional investors. Governance becomes more complex when hundreds or thousands of token holders potentially participate in voting rather than a handful of fund representatives. These considerations necessitate thoughtful analysis before proceeding with tokenization strategies.

Our experience implementing tokenized private equity offerings across USA, UK, UAE, and Canada demonstrates that successful projects prioritize clear governance frameworks, realistic liquidity expectations, and transparent communication with token holders. The technology enables new models but cannot eliminate fundamental risks associated with private company investing including business failure, illiquidity, and information asymmetry. Investors must conduct thorough due diligence on underlying companies or funds rather than assuming tokenization itself reduces investment risk. The democratization of access to private markets creates opportunities but also responsibilities for education and investor protection that the industry is still addressing.

Tokenized Art, Collectibles, and Luxury Assets

The art and collectibles market, valued at hundreds of billions of dollars globally, has long operated as an opaque, exclusive domain accessible only to wealthy collectors and institutions with capital, expertise, and industry connections. Fine art masterpieces by renowned artists trade for tens of millions of dollars, rare collectible cars command similar premiums, and luxury goods like limited edition watches or handbags maintain values through scarcity and brand prestige. Tokenization disrupts this exclusivity by enabling fractional ownership of high-value items, creating liquid markets for traditionally illiquid assets, and providing transparent provenance tracking that combats counterfeiting and fraud.

Fine art tokenization allows a Picasso painting valued at $20 million to be owned collectively by hundreds or thousands of investors, each holding tokens representing fractional ownership stakes. The physical artwork remains in secure, climate-controlled storage or on display in museums, while token holders gain exposure to potential appreciation and can trade their positions on secondary markets. Some platforms allow token holders to vote on exhibition locations, insurance coverage, or eventual sale decisions, creating participatory ownership models impossible with traditional structures. The combination of fractional ownership and enhanced liquidity transforms art from a purely aesthetic or status investment into a more accessible financial asset class.

Provenance tracking emerges as a critical application of blockchain technology in art and collectibles markets plagued by counterfeiting, authentication disputes, and opaque ownership histories. Each token contains immutable records documenting the item’s creation, previous owners, exhibition history, restoration work, and expert authentication certificates. This transparency reduces fraud risks and increases buyer confidence, potentially commanding premium valuations for items with clearly documented provenance. The technology cannot prevent initial introduction of counterfeit items, but once genuine articles are tokenized with authenticated provenance, subsequent ownership transfers maintain verifiable chains of custody impossible to forge.

Luxury goods tokenization extends beyond passive investment to include utility components enabling token holders to access physical items temporarily. A tokenized luxury handbag worth $50,000 might offer holders the right to borrow the physical bag for special occasions, creating shared ownership models where multiple owners rotate physical possession while maintaining fractional economic interests. Similar models apply to exotic cars, vacation properties, or other luxury items where full ownership exceeds needs or budgets but temporary access provides value. These hybrid models blend financial investment with experiential benefits, creating new value propositions impossible in traditional ownership structures.

Valuation challenges represent significant obstacles for art and collectibles tokenization, as these items lack standardized pricing methodologies and market values fluctuate based on subjective factors including artistic merit, historical significance, condition, and collector demand. Independent appraisals provide initial valuations, but ongoing price discovery depends on secondary market trading activity that may be limited for unique, high-value items. Unlike stocks with continuous market prices, tokenized collectibles may trade infrequently, creating challenges for investors requiring liquidity or portfolio valuation. Platforms must develop fair pricing mechanisms balancing issuer interests, investor liquidity needs, and market efficiency.

Our agency’s work with art and collectibles tokenization across USA, UK, UAE, and Canada reveals that successful projects invest heavily in authentication, custody, and insurance arrangements protecting token holders from loss or damage. Items must be stored in professional facilities with appropriate climate control, security systems, and insurance coverage. Regular condition assessments by qualified experts ensure items maintain value over time. Clear exit strategies, whether through eventual auction sales or redemption mechanisms, provide token holders with confidence in their ability to ultimately realize investment returns. Without these foundational elements, tokenization becomes a superficial technical exercise rather than genuine value creation for participants.

Tokenized Carbon Credits and Environmental Assets

Carbon credits and environmental assets represent a rapidly growing tokenization category driven by corporate sustainability commitments, regulatory carbon pricing mechanisms, and investor demand for climate-positive investments. Carbon markets, both voluntary and compliance-based, suffer from opacity, double-counting risks, fragmentation across jurisdictions, and limited liquidity that constrains their effectiveness in driving emission reductions. Blockchain tokenization addresses these deficiencies by creating transparent, immutable records of carbon credit issuance and retirement, preventing double-counting through unique token identifiers, and enabling liquid global markets connecting credit suppliers with corporate and individual buyers.

A carbon credit represents the removal or avoidance of one metric ton of carbon dioxide equivalent through activities like reforestation, renewable energy deployment, or methane capture. Traditional carbon credits are tracked through registries operated by organizations like Verra or Gold Standard, but these systems are siloed, opaque, and vulnerable to double-counting when credits move between registries or jurisdictions. Tokenizing carbon credits creates blockchain-based representations that move seamlessly across platforms while maintaining verifiable provenance and preventing multiple claims on the same emission reduction. Smart contracts can automatically retire tokens when used for offsetting, providing transparent proof of climate action.

Tokenizable Environmental Asset Categories

Verified Carbon Offset Credits

Credits certified by recognized standards like Verra VCS or Gold Standard representing verified emission reductions from reforestation, renewable energy, methane capture, or cookstove projects, with blockchain preventing double-counting and enabling transparent tracking from issuance through retirement.

Renewable Energy Certificates

Certificates representing the environmental attributes of renewable electricity generation, separated from the physical power and traded independently, enabling corporations to claim renewable energy usage regardless of their physical grid connection or electricity source location.

Biodiversity and Nature Credits

Emerging instruments representing measurable biodiversity improvements or habitat preservation outcomes, enabling financing for conservation projects through tokenized credits purchased by corporations seeking nature-positive impacts beyond carbon neutrality commitments.

Plastic Recovery Credits

Credits representing verified collection and proper disposal of plastic waste, particularly in regions lacking waste management infrastructure, enabling corporations to offset plastic packaging use through financing waste recovery projects in developing countries.

Water Rights and Conservation Credits

Tokenized water rights enabling trading in regions with established water markets, plus conservation credits representing verified water savings in water-stressed regions, creating financial incentives for efficient water usage and conservation investments.

The transparency benefits of tokenized carbon credits extend throughout the project lifecycle from initial certification through final retirement. Each token contains metadata describing the underlying project type, location, vintage year, certification standard, and sustainable development co-benefits. Blockchain records document when and by whom credits were retired for offsetting purposes, preventing fraudulent multiple retirements. Investors and corporate buyers can verify credit authenticity and environmental integrity directly rather than relying on intermediary claims, building confidence in carbon markets and encouraging greater participation from skeptical buyers.

Liquidity enhancement represents another significant benefit driving carbon credit tokenization adoption. Traditional carbon markets suffer from fragmentation across project types, geographies, and certification standards, with limited trading platforms and wide bid-ask spreads reflecting illiquidity and information asymmetries. Tokenized carbon credits trade on digital exchanges accessible globally, creating deeper markets with tighter spreads and better price discovery. Fractional trading enables smaller buyers to participate in carbon markets previously dominated by large corporate purchasers, democratizing access to climate action while providing financing for emission reduction projects.

Project financing benefits particularly from tokenization as developers can pre-sell carbon credits before projects are operational, providing upfront capital for equipment purchases, land acquisition, or infrastructure development. A reforestation project might tokenize expected carbon sequestration over 20 years, selling tokens to investors and corporations seeking future offsets at discounted prices. Smart contracts can release tokens to developers as projects achieve verified milestones, aligning financing with performance and reducing risks of non-delivery. This model transforms carbon credits from purely commodity instruments into vehicles for climate project financing.

Regulatory developments across USA, UK, UAE, and Canada are increasingly recognizing tokenized carbon credits within compliance markets and corporate reporting frameworks. While voluntary carbon markets dominate current tokenization activity, integration with cap-and-trade systems and carbon tax regimes would dramatically expand addressable markets. The European Union’s emissions trading system, California’s cap-and-trade program, and various national carbon pricing mechanisms represent multi-billion dollar markets that could benefit from blockchain’s transparency and efficiency. However, regulatory acceptance requires demonstrating that tokenized credits meet the same verification and additionality standards as traditional instruments.

Critical challenges facing environmental asset tokenization include ensuring real-world project quality matches token claims, preventing greenwashing through rigorous verification standards, addressing permanence concerns for nature-based solutions vulnerable to reversal, and developing standardized methodologies for emerging credit types like biodiversity or plastic recovery. Our agency’s experience implementing environmental tokenization projects emphasizes the importance of third-party verification, conservative crediting approaches, and transparent disclosure about project risks and limitations. Tokenization technology provides infrastructure for transparent markets but cannot substitute for fundamental environmental integrity in underlying projects.

How Tokenized RWAs Improve Liquidity in Illiquid Markets

Liquidity, defined as the ease of buying or selling an asset without significantly impacting its price, represents one of the most significant challenges across real-world asset markets. Real estate transactions require months to complete, private equity investments lock up capital for years, and collectibles trade infrequently in opaque dealer networks with wide bid-ask spreads. This illiquidity creates substantial economic costs including reduced valuations to compensate investors for holding illiquid positions, inefficient capital allocation as funds remain trapped in suboptimal investments, and limited participation by smaller investors unable to tolerate long holding periods or lacking exit optionality.

Tokenization attacks illiquidity through multiple complementary mechanisms that transform how assets are traded, priced, and accessed. Fractional ownership dramatically expands the potential buyer pool for high-value assets by reducing minimum purchase requirements from hundreds of thousands to hundreds of dollars. A commercial property requiring $500,000 minimum investment might attract perhaps 1,000 qualified buyers globally, while tokenized ownership at $500 minimum could attract millions of potential investors, deepening markets and improving price discovery. This expanded participation creates more continuous trading activity rather than sporadic large transactions separated by months or years.

| Liquidity Enhancement Mechanism | Traditional Assets | Tokenized Assets | Liquidity Improvement |

|---|---|---|---|

| Minimum Investment Reduction | $100,000+ limits participation to wealthy investors and institutions | $100 to $1,000 enables mass market participation | Potential buyer pool expands 100x to 1,000x |

| 24/7 Global Market Access | Limited to business hours in specific geographies | Continuous trading across all time zones | 3x to 5x increase in available trading hours |

| Transaction Cost Reduction | 3% to 6% fees discourage frequent trading | 0.5% to 2% fees enable active trading | 50% to 75% cost reduction increases velocity |

| Settlement Time Acceleration | Days to months for settlement completion | Minutes to hours for finality | 100x to 1,000x faster capital recycling |

| Price Discovery Enhancement | Sparse transactions create valuation uncertainty | Continuous trading provides real-time pricing | Bid-ask spreads narrow 40% to 60% |

| Automated Market Making | Manual intermediation required for matching | Smart contract pools provide instant liquidity | Guaranteed execution availability |

Automated market maker protocols, borrowed from decentralized finance applications, provide guaranteed liquidity for tokenized assets through algorithmic pricing curves. Liquidity providers deposit tokens into smart contract pools, enabling instant buy and sell execution for traders at algorithmically determined prices that adjust based on supply and demand. This mechanism ensures continuous liquidity even for assets with limited trading activity, though at the cost of price slippage for larger transactions. The availability of instant execution, even at slightly unfavorable prices, represents a substantial improvement over waiting weeks or months to locate counterparties in traditional illiquid markets.

Geographic expansion of investor bases contributes significantly to liquidity improvements for tokenized assets. A commercial property in Toronto traditionally attracts primarily Canadian investors with some cross-border interest from US buyers, limiting the potential buyer pool to perhaps tens of thousands of qualified participants. Tokenization enables global access, potentially attracting investors from Europe, Asia, Middle East, and other regions seeking real estate exposure without physical market presence. This international participation deepens markets, narrows bid-ask spreads, and enables more continuous price discovery reflecting global capital flows rather than local market conditions alone.

Transform Your Asset Portfolio Today

Join leading institutions leveraging Real World Asset Tokenization for enhanced liquidity, reduced costs, and global investor access. Expert consultation available.

However, liquidity expectations must remain realistic about the current state of tokenized asset markets. While tokenization infrastructure enables enhanced liquidity, actual trading volumes depend on investor adoption, platform network effects, and asset quality fundamentals. A tokenized office building in a secondary market with uncertain occupancy will not achieve stock-like liquidity simply through tokenization; the underlying asset quality fundamentally constrains investor demand and trading activity. Early-stage tokenization markets also lack the depth and sophistication of established securities markets, creating risks of manipulation, extreme volatility, and illiquidity during market stress periods.

Our agency’s eight years of experience with tokenized asset liquidity demonstrates that successful projects develop liquidity gradually through strategic initiatives including market maker agreements ensuring minimum bid-ask spreads, integration with multiple trading platforms expanding exposure, investor education programs building demand, and realistic expectations about liquidity timelines. Projects promising immediate stock-like liquidity for illiquid assets set unrealistic expectations that disappoint investors and damage industry credibility. The technology enables liquidity improvements but cannot manufacture buyer demand for assets lacking fundamental investment appeal.

Reducing Entry Barriers for Global Investors Through Tokenization

Traditional asset ownership has perpetuated wealth inequality by concentrating lucrative investment opportunities among institutions and high-net-worth individuals while excluding the majority of global population from participation. A middle-class worker in USA, UK, UAE, or Canada faces insurmountable barriers accessing commercial real estate, private equity, fine art, or other alternative assets offering superior risk-adjusted returns and portfolio diversification benefits compared to stocks and bonds. These barriers include excessive minimum investments, accreditation requirements, geographic restrictions, information asymmetries, and relationship requirements with gatekeeping intermediaries who serve only wealthy clients.

Tokenization fundamentally disrupts this exclusivity by reducing entry barriers across multiple dimensions simultaneously. Minimum investment requirements plummet from hundreds of thousands to hundreds of dollars through fractional ownership, making previously exclusive assets accessible to ordinary investors with modest capital. A teacher earning $50,000 annually can now allocate $500 to tokenized commercial real estate, $300 to fine art, and $200 to carbon credits, achieving portfolio diversification previously available only to millionaires. This democratization does not compromise investment quality but rather expands the investor base for institutional-grade assets, potentially increasing demand and valuations while broadening wealth creation opportunities.

How Tokenization Eliminates Traditional Investment Barriers

Capital Barriers Eliminated

- Fractional ownership reduces minimums 100x to 1,000x

- Invest $100 in properties previously requiring $100,000+

- Diversify across multiple assets with limited capital

- Eliminate need for debt financing or partner pooling

- Access institutional-grade assets at retail scale

Geographic Barriers Removed

- Global access from any internet-connected location

- Invest in international assets without local presence

- No travel costs for property inspections or meetings

- Cross-border transactions in minutes vs. weeks

- Diversify geographically without operational complexity

Information Asymmetries Reduced

- Transparent blockchain records level playing field

- All investors access same real-time data

- Automated reporting eliminates selective disclosure

- Smart contracts ensure equal treatment

- Reduced reliance on expensive advisors

Time Commitment Minimized

- Digital platforms enable investment in minutes

- No lengthy application or approval processes

- Automated compliance reduces paperwork

- Portfolio management through simple interfaces

- Exit flexibility reduces lock-up concerns

Relationship Requirements Eliminated

- No need for private banker or advisor relationships

- Direct access without intermediary gatekeepers

- Merit-based rather than connection-based access

- Equal opportunity for qualified investors

- Reduced favoritism and preferential allocations

Specialized Expertise Less Critical

- User-friendly platforms simplify complex processes

- Educational resources democratize knowledge

- Standardized offerings reduce due diligence burden

- Professional management included in structures

- Lower barriers to understanding and participation

Geographic democratization represents a particularly transformative aspect of tokenization, enabling investors in emerging markets to access premium assets in developed economies while allowing developed market investors to access high-growth opportunities in emerging regions. An investor in India can now allocate capital to London office buildings or Manhattan luxury apartments, while a Canadian investor can access emerging market infrastructure projects or Asian technology ventures. This bidirectional flow of capital improves global capital allocation efficiency by connecting surplus savings in some regions with investment opportunities in others, previously constrained by currency controls, regulatory barriers, and operational complexity.

However, some barriers remain despite tokenization infrastructure. Accreditation requirements persist in many jurisdictions, limiting certain tokenized securities to investors meeting income or net worth thresholds intended to protect unsophisticated participants from complex or risky investments. While tokenization can reduce minimum amounts, it cannot eliminate suitability standards embedded in securities regulations. Platforms must implement robust investor verification ensuring compliance with applicable restrictions, balancing democratization goals against regulatory obligations and investor protection principles.

Education represents another critical component of successful democratization efforts. Lowering entry barriers without corresponding investor education creates risks of uninformed decision-making and unrealistic expectations about returns, risks, or liquidity. Responsible platforms invest in educational content explaining asset characteristics, risk factors, fee structures, and realistic performance expectations. This education enables informed participation rather than simply opening access to complex investments that investors lack capacity to evaluate properly. The goal should be empowered participation, not merely expanded participation.

Our agency’s experience facilitating tokenization across USA, UK, UAE, and Canada demonstrates that platforms successfully democratizing access balance innovation with responsibility through graduated access levels based on investor sophistication, mandatory education requirements before investment, clear risk disclosures avoiding marketing hyperbole, realistic liquidity expectations, and investor protection mechanisms including cooling-off periods and suitability assessments. These measures ensure democratization creates genuine opportunity rather than exposing unsophisticated investors to inappropriate risks they cannot adequately evaluate or manage.

Role of Smart Contracts in Managing Tokenized Assets

Smart contracts serve as the operational backbone enabling automated, trustless management of tokenized assets without reliance on intermediaries or centralized authorities. These self-executing programs deployed on blockchain networks encode business logic, compliance rules, and economic mechanisms directly into computer code that executes deterministically when predefined conditions are met. Smart contracts eliminate the inefficiencies, errors, and potential for fraud inherent in manual processes while reducing operational costs and enabling complex functionalities impractical under traditional systems. Understanding smart contract capabilities and limitations is essential for designing effective tokenization solutions.

The fundamental value proposition of smart contracts in tokenized asset management lies in automation replacing manual administrative processes. Traditional asset management involves numerous intermediaries including transfer agents tracking ownership, paying agents distributing income, trustees enforcing bond covenants, and corporate action processors managing votes and tender offers. Each intermediary adds costs, delays, and potential for error or misconduct. Smart contracts consolidate these functions into programmable code executing automatically, reducing costs by up to 90% while improving accuracy, speed, and transparency.

Compliance automation represents perhaps the most impactful smart contract application for regulated tokenized securities. Traditional securities transfers require manual verification that buyers and sellers meet eligibility requirements, creating delays and potential for error or fraud. Smart contracts integrate compliance logic directly into token transfer functions, automatically checking that proposed transfers satisfy all applicable restrictions before execution. A token might verify that the recipient holds valid accreditation credentials, resides in a permitted jurisdiction, does not exceed ownership concentration limits, and satisfies any holding period requirements, all within a single atomic transaction executed in seconds.

Income distribution automation demonstrates another high-value smart contract application particularly relevant for real estate, fixed income, and dividend-paying equity tokens. Traditional distribution processing involves manual calculations determining each holder’s proportional entitlement, payment system integration, reconciliation, and reporting. Smart contracts execute distributions automatically based on ownership snapshots at predetermined dates, calculating payments mathematically according to token holdings and transferring funds simultaneously to all holders. This automation reduces errors, eliminates selective delays or preferential treatment, and provides transparent audit trails documenting distribution calculations and execution.

Oracle integration enables smart contracts to respond to real-world events and data despite blockchains’ inability to directly access external information. Oracles are trusted data feeds providing verified information from outside blockchain networks to smart contracts, enabling conditional logic based on asset valuations, interest rate changes, corporate events, or performance metrics. A tokenized bond might use interest rate oracles to adjust floating coupon payments, while a real estate token could use property valuation oracles to calculate net asset value for redemptions. The security and reliability of oracle networks is critical, as compromised data feeds can trigger incorrect smart contract executions with financial consequences.

Smart contract security represents a paramount concern given that code vulnerabilities can be exploited to steal tokens, manipulate prices, or disrupt operations. Unlike traditional software that can be patched when bugs are discovered, blockchain smart contracts are typically immutable after deployment, making errors permanent and unfixable. Comprehensive security audits by specialized firms are essential before mainnet deployment, identifying logical flaws, reentrancy vulnerabilities, arithmetic errors, or access control weaknesses. Even audited contracts remain vulnerable to novel attack vectors or interactions with other contracts creating unexpected behaviors, requiring ongoing monitoring and incident response capabilities.

Our agency’s eight years of smart contract development experience has revealed that successful implementations balance automation benefits against flexibility needs through upgradeability mechanisms, emergency pause functions, timelocks on critical operations, and off-chain governance processes for parameter adjustments. Over-automation without human oversight creates risks of systems executing inappropriate actions during exceptional circumstances that code cannot anticipate. The optimal approach combines smart contract automation for routine operations with human governance for extraordinary decisions requiring judgment, maintaining efficiency gains while preserving appropriate control and adaptability.

Compliance and Regulation in Real-World Asset Tokenization

Regulatory compliance represents both the greatest challenge and most critical success factor for real-world asset tokenization, determining whether projects achieve mainstream adoption or face enforcement actions, investor losses, and market credibility damage. While blockchain technology enables innovative asset management approaches, tokenized securities remain subject to the same regulatory frameworks governing traditional securities, requiring registration with authorities or reliance on exemptions with associated disclosure and ongoing compliance obligations. Understanding regulatory requirements across USA, UK, UAE, Canada, and other key markets is essential for designing compliant tokenization solutions that balance innovation with investor protection and legal certainty.

The fundamental regulatory question for tokenized assets centers on classification: are tokens securities, commodities, currencies, or novel instruments requiring new regulatory categories? In most jurisdictions, tokens representing ownership interests, profit participation rights, or investment contracts expecting returns from others’ efforts are classified as securities subject to comprehensive regulation. This classification triggers registration requirements, disclosure obligations, anti-fraud provisions, and ongoing reporting duties that issuers must satisfy. The technology of tokenization does not exempt assets from securities regulation; rather, it requires thoughtful integration of compliance mechanisms into technical infrastructure.

| Jurisdiction | Regulatory Framework | Key Requirements | Common Exemptions |

|---|---|---|---|

| United States | Securities Act 1933, Securities Exchange Act 1934, SEC oversight | Registration or exemption, disclosure documents, ongoing reporting, transfer restrictions, accredited investor verification | Regulation D (Rule 506b, 506c), Regulation A+, Regulation S, Section 4(a)(2) |

| United Kingdom | Financial Services and Markets Act 2000, FCA regulation | FCA authorization for platforms, prospectus requirements, investor categorization, conduct rules, ongoing supervision | Prospectus exemptions for qualified investors, private placements, small offerings under thresholds |

| UAE (Dubai) | DFSA regulations, VARA regulations, SCA oversight | License requirements for issuers and platforms, offering documentation, investor suitability, AML compliance, ongoing reporting | Professional investor exemptions, free zone offerings, private placement frameworks |

| Canada | Provincial securities acts, CSA harmonized approach | Prospectus or exemption in each province, disclosure documents, dealer registration for platforms, transfer restrictions, continuous disclosure | Accredited investor exemption, offering memorandum exemption, crowdfunding exemptions, private issuer exemptions |

Know-your-customer and anti-money laundering compliance represents a non-negotiable requirement for tokenized asset platforms, mandating verification of investor identities, sources of funds, and ongoing monitoring for suspicious activities. Traditional KYC processes involving manual document review and verification are incompatible with blockchain’s global, pseudonymous nature, requiring innovative solutions integrating identity verification into token transfer protocols. Many platforms implement whitelist systems where only verified addresses can hold or receive tokens, with smart contracts automatically rejecting transfers to non-verified addresses. This approach maintains compliance while preserving efficiency benefits of blockchain settlement.