Ai Overview

A token-based MLM offering is a business model where participants are recruited into a multi-level network and rewarded with digital tokens for sales activity, referrals, or both. A token qualifies as a security if it involves an investment of money in a common enterprise with the expectation of profits derived from the efforts of others. Engaging a regulatory lawyer at this stage is not optional; it is the most cost-effective thing you can do.

Key Takeaways

- The SEC uses the Howey Test to decide whether a token qualifies as a security. If it does, the entire MLM distribution model is subject to securities law.

- The FCA in the UK classifies cryptoassets into four categories. Token-based MLMs that use utility or security tokens must pass a harm-based assessment before any promotion goes live.

- MAS in Singapore requires digital token offerings to comply with the Securities and Futures Act (SFA) and the Payment Services Act (PSA) if the token functions as a payment instrument.

- All three regulators require operators to conduct KYC (Know Your Customer) and AML (Anti-Money Laundering) checks on participants in a token MLM.

- Misleading income claims in token MLM promotions are one of the most cited reasons for enforcement actions across all three jurisdictions.

- Cross-border token MLM operations are subject to all applicable laws in each country where participants reside, not just the country of incorporation.

Running a token-based MLM (multi-level marketing) business sounds exciting on paper. You get a digital token economy, a community of distributors, and a product tied to blockchain technology. But underneath that excitement sits a very real legal minefield, one that has shut down dozens of projects across the US, UK, and Singapore in the last five years alone.

The three regulators that matter most right now are the SEC (Securities and Exchange Commission) in the United States, the FCA (Financial Conduct Authority) in the United Kingdom, and the MAS (Monetary Authority of Singapore). Each of them has published specific frameworks that apply to how tokens are sold, promoted, and distributed inside multi-level or network marketing structures.

We have spent over eight years helping blockchain ventures, token issuers, and direct-selling networks navigate these exact compliance challenges. What follows is a practical breakdown of each regulator’s expectations, the tests they apply, the penalties they enforce, and what a responsible token MLM structure actually looks like on the ground.

What Are Token-Based MLM Offerings, Exactly?

A token-based MLM offering is a business model where participants are recruited into a multi-level network and rewarded with digital tokens for sales activity, referrals, or both. The tokens may have monetary value on a cryptocurrency exchange, be redeemable for products or services, or function as governance rights within a platform.

The issue regulators focus on is not the token itself but the combination of financial incentive structures. When tokens serve both as a product reward and a recruitment incentive, the structure starts to look like a financial instrument tied to a pyramid-like compensation plan. That is when SEC, FCA, and MAS attention tends to arrive.

To understand the broader blockchain context behind these networks, our guide on blockchain MLM networks covers the foundational architecture. What matters for this article is how that architecture is seen through a legal lens.

According to the FTC’s business guidance on multi-level marketing, a legitimate MLM must derive the majority of revenue from actual product sales to real consumers, not from enrollment fees or token purchases by new recruits. Token MLMs that fail this test face immediate scrutiny.

SEC Guidelines: How the US Regulates Token MLM Offerings

The SEC does not have a specific law for token MLMs. Instead, it applies existing securities law, primarily the Securities Act of 1933 and the Securities Exchange Act of 1934, to any token it determines qualifies as a security.

The primary tool the SEC uses is the Howey Test, derived from the 1946 Supreme Court case SEC v. W.J. Howey Co. A token qualifies as a security if it involves an investment of money in a common enterprise with the expectation of profits derived from the efforts of others. In a token MLM, where participants join by purchasing tokens and earn more tokens by recruiting others, almost every element of this test is met.

The SEC has pursued enforcement actions against several token-based projects that operated through referral networks. In these cases, the fact that participants were promised returns based on recruitment activity was enough to trigger securities law regardless of whether the token had a “utility” attached to it.

For token MLM operators in or targeting the US market, the practical implications are:

- If the token is a security, it must be registered under the Securities Act or sold under an exemption (Regulation D, Regulation S, or Regulation A+).

- Promoters and distributors who solicit participants may qualify as brokers under federal law and require FINRA registration.

- Marketing materials cannot make forward-looking profit claims without adequate risk disclosures.

- Smart contract-based MLM reward systems do not exempt the operator from these requirements simply because the system is automated.

FCA Guidelines: Token MLM Rules in the United Kingdom

The UK’s Financial Conduct Authority has been particularly active in regulating crypto promotions since the passing of the Financial Services and Markets Act 2023 (FSMA 2023), which brought cryptoasset promotions fully under the UK financial promotion regime.

The FCA classifies cryptoassets into three broad categories: exchange tokens (like Bitcoin), security tokens (representing financial claims), and e-money tokens. A fourth category, utility tokens, sits outside formal FCA regulation but is still subject to consumer protection and promotion rules if it is being sold or promoted to UK consumers.

For token MLMs specifically, the FCA’s position is clear from its published guidance on financial promotion expectations: firms must consider whether platforms using affiliate or referral reward structures fall within the definition of financial promotions, and if so, they must be communicated by or approved by an FCA-authorised person.

The specific issues for token MLMs in the UK include:

- Any promotion that incentivises someone to refer others to a cryptoasset product likely qualifies as a financial promotion and must be registered with the FCA.

- Unregistered token MLM promotions sent to UK consumers can result in criminal prosecution with up to two years imprisonment.

- The FCA requires all financial promotions to be fair, clear, and not misleading. Income projections, token price forecasts, or claims of guaranteed returns violate this standard.

- UK consumers who invested based on illegal promotions have a right to unwind the investment and claim compensation.

The FCA has added over 1,500 companies to its warning list in recent years, a significant portion of which involved crypto token referral schemes. That number alone should signal the seriousness of the regulator’s intent.

MAS Guidelines: How Singapore Approaches Token-Based MLM

Singapore has positioned itself as a crypto-friendly jurisdiction, but MAS has been precise in defining the rules. The Payment Services Act (PSA) 2019, the Securities and Futures Act (SFA), and MAS’s own guidelines on digital token offerings together form a comprehensive framework.

According to MAS’s guidelines on standards of conduct for marketing and distribution activities, financial services firms and intermediaries must ensure that marketing materials do not mislead customers about the risks or returns of financial products, including digital tokens.

For token MLM operators using Singapore as a base or targeting Singaporean consumers:

- If the token is a capital markets product under the SFA, a full prospectus or exemption is required before it can be offered to the public.

- If the token is used as a digital payment token (DPT), the operator must be licensed under the PSA or hold a Major Payment Institution licence.

- Pyramid selling is explicitly prohibited under the Multi-Level Marketing and Pyramid Selling (Prohibition) Act in Singapore. Token-based structures that rely primarily on recruitment income rather than genuine product value fall under this prohibition.

- MAS requires all regulated entities to comply with FATF travel rule requirements, which means tracking and reporting token transfers between MLM participants above a certain threshold.

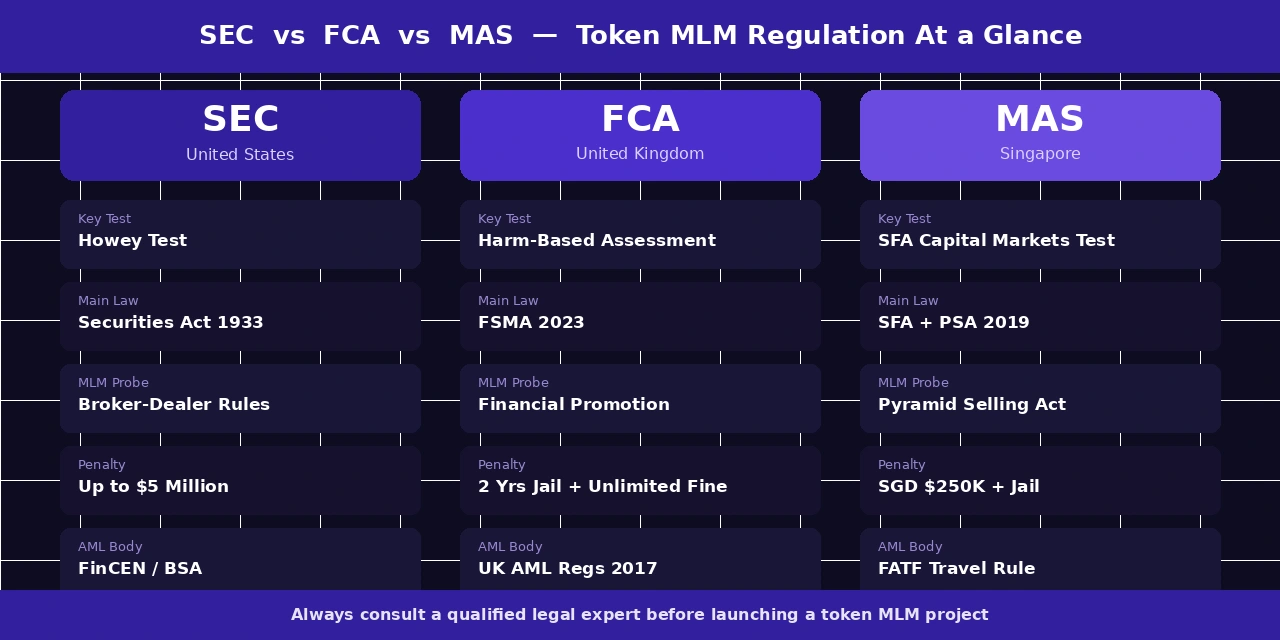

SEC vs FCA vs MAS: A Compliance Comparison for Token MLM Operators

The table below gives you a quick reference for comparing how each regulator approaches the same compliance questions. While the goals are similar, the specific tests, penalties, and licensing requirements are quite different.

| Criteria | SEC (USA) | FCA (UK) | MAS (Singapore) |

|---|---|---|---|

| Token Classification Test | Howey Test | FCA 4-Category Taxonomy | SFA / PSA Classification |

| Primary Legislation | Securities Act 1933 | FSMA 2023 / FPO | SFA + PSA 2019 |

| Registration Required? | Yes (or exemption) | Yes (or FCA-approved firm) | Yes (if CMP or DPT) |

| Referral / MLM Structure | Triggers broker-dealer rules if commissions paid | Affiliate links = financial promotion | Pyramid selling prohibited under MLM Act |

| AML / KYC Required? | Yes (BSA/FinCEN) | Yes (UK AML Regs 2017) | Yes (FATF Travel Rule) |

| Max Civil Penalty | Up to $5M per violation | Unlimited (+ 2yr imprisonment) | Up to SGD $250,000 + jail |

| Misleading Promotions | Rule 10b-5 violation | S.25 FSMA / FCA PS22/10 | MAS Guidelines FSG-G02 |

| Cross-Border Reach | Extraterritorial if US persons involved | Applies to UK consumers regardless of origin | Applies to Singapore-based persons |

The Token MLM Compliance Lifecycle: From Design to Operation

Compliance is not a one-time checkbox at launch. It is a continuous process that starts the moment you begin designing the token economy and continues for as long as the project is live. Here is how the key stages break down:

Stage 1: Token Design

Decide whether the token will function as a security, utility, or payment instrument. The classification determines every other compliance step. Engaging a regulatory lawyer at this stage is not optional; it is the most cost-effective thing you can do.

Stage 2: Legal Review

A thorough legal review must map the token against the Howey Test, FCA category taxonomy, and MAS SFA/PSA criteria. It should also assess the compensation plan to confirm it does not constitute pyramid selling under local statutes.

Stage 3: Registration and Filing

Depending on the jurisdiction, this involves filing a prospectus, registering as a money services business, obtaining an FCA registration, or applying for a Major Payment Institution licence with MAS. Some projects use exemptions, but each exemption has strict conditions on who can invest.

Stage 4: Launch and Marketing

All promotional materials must be reviewed against local advertising standards. This means no guaranteed return claims, no misleading testimonials, and no affiliate promotion unless the referral structure has been assessed as compliant. The FCA requires prominent risk warnings on all crypto promotions.

Stage 5: Ongoing Reporting

Registered entities must file regular reports with their respective regulators, maintain transaction records for AML purposes, and update risk disclosures when the token’s function or value characteristics change materially. Any change to the compensation structure may require a fresh legal review.

Real-World Example: What a Non-Compliant Token MLM Looks Like

Case Study: A Token MLM that Triggered SEC Action

Consider a hypothetical project called TokenReach, launched in 2021 across the US, UK, and Singapore. TokenReach sold “membership packages” bundled with a proprietary token called TRX. Participants earned TRX by recruiting new members. The company’s promotional materials showed income charts with monthly returns between 15% and 40%.

Under the Howey Test, TRX was clearly a security: participants invested money, the enterprise was common, and returns came from the company’s management efforts. TokenReach had not registered TRX as a security, nor did it qualify for any exemption. Its promoters were soliciting investments without broker-dealer registration.

In the UK, the promotional material was disseminated via an affiliate link network without FCA approval. In Singapore, TRX was traded on a local exchange without a PSA licence. Within 14 months of launch, the project faced enforcement actions in all three jurisdictions simultaneously.

This pattern is unfortunately common. The lesson is not that token MLMs are inherently illegal. The lesson is that compliance must be built into the design, not retrofitted after launch when regulators are already at the door.

Most Common Compliance Mistakes in Token-Based MLM Projects

| Mistake | Why It’s a Problem | Applicable Regulator |

|---|---|---|

| Skipping the Howey analysis | Token treated as utility when it’s actually a security | SEC |

| Affiliate links without FCA approval | Constitutes an unlawful financial promotion | FCA |

| No KYC/AML process | Violates FinCEN, UK AML Regs, FATF rules | SEC, FCA, MAS |

| Misleading income claims | Violates securities, consumer, and FTC rules | SEC, FCA, MAS, FTC |

| Operating exchange without PSA licence | Illegal DPT service provision in Singapore | MAS |

| Ignoring cross-border reach | US law covers any transaction involving a US person | SEC |

| Compensation based on recruitment not sales | Pyramid selling, illegal across all three jurisdictions | SEC, FCA, MAS |

How to Build a Token MLM Structure That Can Actually Pass Regulatory Review

There is no single formula that makes a token MLM automatically compliant. But there is a set of structural decisions that significantly reduce exposure across all three jurisdictions. Here is what our team consistently recommends to clients building in this space.

The first decision is token design that separates reward from investment. Tokens used in the compensation plan should not also function as tradeable financial instruments unless the full securities registration process has been completed. A utility token that gives access to a platform service, with clearly defined use cases and no expectation of appreciation, is far less likely to trigger the Howey Test.

The second decision is building compensation primarily on product sales. The FTC’s guidance on MLM, referenced earlier, makes clear that a legitimate network marketing business must demonstrate that participants earn primarily from selling real products to real consumers, not from recruiting new members. This same standard is used as a reference point by FCA and MAS when assessing whether a token distribution scheme constitutes a pyramid operation.

The third decision is geo-fencing for jurisdictions where you are not licensed. If you hold a MAS Major Payment Institution licence but not an FCA registration, you must actively prevent UK consumers from participating. This means IP blocking is not enough. You need contractual restrictions, geo-targeted onboarding, and verified user location at KYC stage.

The fourth decision is promotional content review before any affiliate or referral network is activated. Every piece of content shared by a distributor or referral partner that promotes the token offering to new participants is potentially a financial promotion. FCA in particular holds the issuer liable for the communications of its distributors.

If you are at the planning stage of a token-based direct selling project, our work on blockchain MLM regulation provides a useful foundation for understanding what a compliant architecture looks like in practice.

“In our experience working with over 1200 token and blockchain projects across three continents, the single biggest compliance failure is not the token design itself. It is the promotional structure. The moment you add a referral reward to a crypto promotion, you have introduced a layer of financial regulation that most teams are not prepared for. Building compliance into the affiliate model from day one is not just smart, it is the only way to scale across multiple jurisdictions without eventually facing a shutdown.”

Compliance Strategist, Blockchain MLM Advisory Practice (8+ years, 1200+ projects)

Quick Reference: Licensing Requirements by Jurisdiction

| Jurisdiction | Licence / Registration | Issued By | Typical Timeline |

|---|---|---|---|

| USA | Regulation D / A+ Filing or Full Registration | SEC | 4 to 12 months |

| USA (AML) | MSB Registration | FinCEN | 1 to 3 months |

| UK | Cryptoasset Business Registration | FCA | 3 to 9 months |

| Singapore | Major Payment Institution Licence | MAS | 6 to 18 months |

| Singapore (securities) | Capital Markets Services Licence | MAS | 6 to 24 months |

A Note on Multi-Jurisdictional Operations: India and Beyond

While this article focuses on the SEC, FCA, and MAS, many token MLM operators also have significant participant bases in India. India has its own regulatory complexity. The Ministry of Consumer Affairs issued direct selling guidelines that govern how MLM businesses must operate, and India’s government rules for MLM companies require formal registration, transparent compensation disclosure, and a cooling-off period for participants.

For those exploring how to formally incorporate an MLM entity in India, Taxmann’s expert guide to starting an MLM company in India offers a practical breakdown of the legal entity structure, SEBI requirements, and direct selling guidelines that apply.

The broader point is that token MLM operations targeting participants in multiple countries must conduct a separate regulatory analysis for each major jurisdiction. There is no single “global licence” that covers token-based MLM activity across the US, UK, Singapore, and India simultaneously.

Build a Compliant Token MLM Platform

Our team has helped 80+ token and blockchain ventures navigate SEC, FCA, and MAS compliance. From token design to smart contract architecture, we build solutions that scale without regulatory risk.

The Bottom Line: Compliance Is Not a Barrier, It’s a Foundation

Many founders come to us worried that compliance will slow them down or price them out of the market. The opposite is true. Projects that launch without regulatory clarity either fail to scale because institutional partners and exchanges will not touch them, or they face enforcement actions that cost far more than compliant launch would have.

The SEC, FCA, and MAS are not trying to eliminate token-based businesses. They are trying to ensure that participants are protected, that promotions are honest, and that operators have taken responsibility for the financial instruments they are putting into the market. These are standards that any serious long-term business should want to meet.

Whether you are running a cryptocurrency MLM software platform or launching a new token-based direct selling network, the framework exists to help you do it right. Use it.

For a broader look at global MLM regulation across different regions and business types, our guide on MLM meaning, types, benefits, and global regulation is worth reading alongside this one.

Frequently Asked Questions

Q1.Is a token-based MLM considered a security under SEC rules?

It depends on the Howey Test. If participants invest money in a common enterprise and expect profits primarily from the efforts of others, the token is likely a security. Most token MLMs that pay referral commissions in tokens will trigger this test.

Q2.Can I launch a token MLM in the UK without FCA registration?

Not safely. The FCA requires any business making financial promotions of cryptoassets to either be FCA-registered or have its promotions approved by an FCA-authorised firm. Operating without this exposes you to criminal prosecution.

Q3.What is the difference between a utility token and a security token under MAS rules?

MAS distinguishes digital tokens by their primary function. A utility token gives access to a product or service. A security token represents an ownership claim, debt obligation, or right to future profits. Security tokens fall under the Securities and Futures Act and require a full prospectus or exemption.

Q4.What happens if an MLM company distributes tokens to members without complying with SEC rules?

The SEC can impose civil penalties of up to $5 million per violation, require disgorgement of profits, issue cease-and-desist orders, and in serious cases, pursue criminal referrals to the Department of Justice.

Q5.Do token MLM platforms need to apply anti-money laundering controls?

Yes. All three regulators require AML and KYC compliance. MAS, in particular, mandates that digital payment token service providers register under the Payment Services Act and implement FATF-aligned AML controls.

Q6.Can a token MLM structure be run legally if it has a genuine product?

Yes, but having a genuine product is only one part of the compliance picture. The FTC in the US, along with the SEC and FCA, still requires that the majority of revenue comes from real product sales to real end consumers, not from recruiting new members who buy tokens to participate.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.