Ai Overview

The generative AI market landscape has undergone a seismic shift over the past two years. This expert analysis covers everything from generative AI market size and key statistics to regional insights, sector-specific growth, investment trends, and a forward-looking generative AI market forecast analysis through 2032. The UAE placed $4 billion in private AI investment in 2025, making it the 15th largest national investor in AI globally a remarkable position for an economy of its size.

The generative AI market landscape has undergone a seismic shift over the past two years. What was once a niche research domain has evolved into one of the fastest-scaling technology markets in recorded history. With over eight years of hands-on experience advising enterprises across India, the UAE, and global markets, our team has witnessed this transformation first-hand. In 2026, the generative AI market is no longer about experimentation; it is about execution, scale, and competitive survival. Businesses that fail to build a strategic AI roadmap today risk falling permanently behind peers who moved decisively. This expert analysis covers everything from generative AI market size and key statistics to regional insights, sector-specific growth, investment trends, and a forward-looking generative AI market forecast analysis through 2032.

Key Takeaways

The global generative AI market size is projected to reach $83–161 billion in 2026, with forecasts pointing to over $890 billion by 2032 at a CAGR above 40 percent.

The UAE ranks among the top global nations for AI adoption with over 80 percent of employees using AI tools regularly, making Dubai a critical hub for generative AI market growth in the Middle East.

India is the fastest-growing regional market in Asia Pacific, projected to surpass $8.3 billion in generative AI revenue by 2030, driven by its large IT sector and digital-first enterprises.

Multimodal AI and SaaS-based generative AI platforms are the fastest-growing segments, with the SaaS segment projected to register a CAGR of 57 percent through 2032.

Healthcare and life sciences is among the fastest-growing end-user sectors, with generative AI applications spanning drug discovery, protein design, and intelligent patient-support automation.

Top five generative AI market players, including OpenAI, Microsoft, Google, NVIDIA, and Anthropic, collectively held over 58 percent of global market share in 2025.

Corporate investment in generative AI more than doubled in 2025, and organisational adoption rose to 88 percent globally, signalling irreversible mainstream integration across enterprise sectors.

Generative AI adoption has jumped from 33 percent of companies in 2023 to 79 percent in 2025, representing one of the steepest two-year adoption curves in enterprise technology history.

Generative adversarial networks (GANs) are projected to account for 57.5 percent of total generative AI market share in 2026, fuelled by demand for realistic synthetic image, video, and audio generation.

Data privacy, regulatory uncertainty, and high compute costs remain the primary barriers constraining smaller businesses from scaling generative AI market participation in emerging economies.

Overview of the Generative AI Market in 2026

The generative AI market in 2026 stands at an inflection point that few technologies have reached this quickly. Across industries, continents, and company sizes, generative AI has transitioned from a buzzword to a business-critical capability. Having worked with enterprise clients across India and the UAE for over eight years, we can say with confidence that the pace of adoption we are witnessing today is unprecedented. Enterprises are no longer piloting generative AI they are operationalising it, embedding it into core workflows, customer interactions, product creation, and strategic decision-making.

Generative AI refers to AI systems capable of creating new content text, images, video, audio, code, and synthetic data by learning patterns from vast training datasets. Unlike traditional AI models built for prediction or classification, generative models produce net-new outputs that can mimic, extend, or improve upon human-created material. The commercial applications span from marketing automation and software engineering to scientific research, medical imaging, financial analysis, and customer service.

What makes 2026 particularly significant for the generative AI market is the convergence of several macro forces: reduced foundation model costs, the emergence of open-source models competitive with proprietary giants, rapid cloud infrastructure scaling, and deepening regulatory clarity in major markets. These forces together are driving generative AI market growth at a pace that analysts consistently revise upward each quarter.

Generative AI Market Size and Key Statistics

Understanding the generative AI market size requires acknowledging that different research methodologies yield different estimates, but every credible source agrees on one thing: the trajectory is steeply upward. The variation in exact figures reflects differences in scope some include only software, while others encompass hardware, services, and infrastructure.

According to Fortune Business Insights, the global generative AI market is projected to grow from $83.3 billion in 2026 to over $988 billion by 2035 at a CAGR of 31.6 percent. MarketsandMarkets places the 2026 figure higher, forecasting the market will reach $890.59 billion by 2032 from $71.36 billion in 2025 at a CAGR of 43.4 percent. Grand View Research estimates a 2026 value of approximately $29.6 billion for core software and services, growing to $324.68 billion by 2033. The divergence in figures underscores the breadth of what falls under the generative AI market umbrella. The table below provides a consolidated view across leading research firms.

| Research Firm | 2026 Market Size | End Year | Forecast Value | CAGR |

|---|---|---|---|---|

| MarketsandMarkets | ~$93B est. | 2032 | $890.59B | 43.4% |

| Fortune Business Insights | $161B | 2034 | $1,260.15B | 29.3% |

| Global Market Insights | $83.3B | 2035 | $988.4B | 31.6% |

| Grand View Research | $29.63B | 2033 | $324.68B | 40.8% |

| Coherent Market Insights | $121.10B | 2033 | $900.74B | 33.2% |

Generative AI Market Analysis: Current Scenario and Insights

A rigorous generative AI market analysis reveals a sector operating at two speeds simultaneously. At the frontier, hyperscalers and foundation model labs OpenAI, Google DeepMind, Anthropic, Meta AI are racing to build more capable, efficient, and multimodal models. At the enterprise layer, a vast and growing ecosystem of SaaS companies, systems integrators, and specialist consultancies is translating that frontier capability into practical business workflows.

Our generative AI market analysis across client engagements in Dubai and Indian metros shows a clear pattern: businesses that treated 2023 and 2024 as learning years are now moving to scaled production in 2026. The most common use cases being operationalised include AI-assisted content generation, intelligent document processing, customer service automation, code generation, and synthetic data production for model training.

The software segment continues to lead the generative AI market, accounting for approximately 81 percent of total market revenue in 2025. Within software, generative AI SaaS is the fastest-growing sub-segment, reflecting enterprises’ preference for cloud-native, API-first solutions that minimise upfront capital expenditure and allow rapid iteration. The services segment encompassing consulting, integration, and managed AI operations is also expanding quickly as organisations build internal AI governance capabilities.

Transformer architecture continues to dominate the technology landscape, holding approximately 40.9 percent of overall generative AI market share in 2025. Large language models built on transformers underpin the majority of commercial generative AI applications, from code assistants to legal document analysis. Meanwhile, GANs retain strong relevance in image, video, and audio synthesis, accounting for a projected 57.5 percent of the technology segment share in 2026.

Key Drivers Behind Generative AI Market Growth

Generative AI market growth is propelled by a convergence of technical, commercial, and macroeconomic forces. Understanding these drivers is essential for business leaders seeking to time and prioritise their AI investments.

Automation Demand

Enterprises in every sector are under relentless pressure to reduce operational costs. Generative AI offers a credible path to automating repetitive, high-volume tasks in content production, data entry, customer communication, and code review.

Falling Compute Costs

GPU and cloud inference costs have dropped dramatically, making it economically viable for mid-market businesses and SMEs in India and the UAE to deploy generative AI at scale without prohibitive upfront investment.

Open-Source Model Proliferation

The availability of capable open-source foundation models has democratised access to generative AI capabilities, enabling organisations to fine-tune domain-specific models on proprietary data without licensing large proprietary systems.

Government AI Mandates

The UAE has mandated AI education and is boosting national AI investment. India’s Digital India and National AI Mission initiatives are accelerating public and private sector adoption, creating fertile ground for generative AI market expansion.

Surging Enterprise Investment

Corporate investment in generative AI more than doubled in 2025. Boards and CEOs are now viewing generative AI not as an IT experiment but as a core strategic asset that belongs in annual capital allocation budgets.

Digital Workforce Demand

Skilled talent shortages in software, content, legal, and research functions are pushing organisations to supplement human capacity with generative AI tools, improving output quality while reducing hiring pressure.

Top Generative AI Market Trends Shaping the Industry

Tracking generative AI market trends is no longer optional for strategic planners. The trends below are not speculative they are actively reshaping procurement decisions, product roadmaps, and competitive positioning across markets including India, Dubai, and global enterprise hubs.

1. Multimodal AI Goes Mainstream

The multimodal AI segment is projected to register the highest CAGR of 56.6 percent through 2032. Models that simultaneously process and generate text, images, video, and audio are replacing single-modality tools, enabling richer customer experiences and more powerful enterprise workflows. Businesses in the media, retail, and healthcare sectors in India and the UAE are among the fastest adopters of multimodal generative AI capabilities.

2. Agentic AI and Autonomous Workflows

AI agents that can plan, execute multi-step tasks, and interact with external tools are moving from research to production. In early 2026, Microsoft, IBM, and Salesforce all expanded their enterprise AI agent platforms. This trend represents a significant evolution in the generative AI market, shifting from single-prompt generation toward sustained autonomous task completion that can handle complex business processes end to end.

3. Domain-Specific Foundation Models

General-purpose large language models are giving way to domain-specific models fine-tuned on legal, medical, financial, and engineering data. These specialised models outperform general models on vertical tasks while reducing hallucination risk, making them far more suitable for regulated industries. This trend is particularly relevant for financial services firms in Dubai and pharmaceutical companies across India.

4. AI-First Product Architectures

More enterprises are rebuilding core products around generative AI capabilities rather than layering AI on top of existing architecture. This AI-first approach is reshaping the software industry, with generative AI becoming essential infrastructure for competitive advantage rather than a feature add-on. Startups in India’s Bengaluru and Mumbai ecosystems and Dubai’s DIFC tech district are leading this architectural shift.

5. Generative AI Regulation Maturing

Regulatory frameworks around AI transparency, copyright, data usage, and safety are maturing across the EU, US, UAE, and India. Rather than slowing the generative AI market growth, clear regulation is actually accelerating enterprise adoption by reducing compliance uncertainty and building end-user trust in AI-generated outputs.

Generative AI Market Forecast Analysis for 2026–2032

The generative AI market forecast analysis for the period 2026 to 2032 presents one of the most compelling growth stories in technology sector history. Across all credible projections, the compound annual growth rate exceeds 30 percent, with several estimates above 40 percent. This is not speculative hype it reflects the structural shift in how enterprises view AI as a core operational input rather than a discretionary tool.

MarketsandMarkets’ generative AI market forecast analysis, published in March 2026, projects the market will surge from $71.36 billion in 2025 to $890.59 billion by 2032 an almost 12-fold increase in seven years. This forecast is supported by expanding enterprise deployment, the growth of AI SaaS platforms, increasing multimodal model capabilities, and deeper integration into productivity software used by hundreds of millions of workers globally.

Generative AI Market Size Growth Trajectory (2025–2032)

From a generative AI market forecast analysis perspective, the SaaS segment deserves particular attention. With a projected CAGR of 57 percent through 2032, it is growing nearly 15 percentage points faster than the overall market. This reflects the fundamental shift in how businesses procure AI capabilities favouring subscription-based, API-driven access over custom infrastructure builds.

Looking at regional generative AI market forecast analysis, Asia Pacific is expected to be the fastest-growing region overall. Within Asia Pacific, India stands out as the most dynamic growth market. For the UAE and the broader Gulf Cooperation Council region, the combination of government AI mandates, high per-capita digital engagement, and robust private investment positions the Middle East as a generative AI market growth story that rivals much larger economies in proportional terms.

[1]

Generative AI Market Growth Across Major Industries

Generative AI market growth is not uniform across sectors. Some industries are experiencing rapid, transformative adoption while others are in earlier stages. Understanding sector-specific dynamics is critical for investment prioritisation and partnership strategy.

Healthcare and Life Sciences

This sector is among the fastest-growing end-user segments for generative AI. Applications include drug molecule design, protein structure prediction, personalised medicine, clinical trial optimisation, and intelligent patient support automation. Indian pharmaceutical firms and UAE hospital networks are both investing heavily in generative AI-driven research tools.

Financial Services and Banking

BFSI firms are deploying generative AI for real-time fraud detection, automated report generation, personalised financial advice, regulatory compliance documentation, and risk scenario modelling. Dubai’s DIFC financial hub and Indian banking majors are at the forefront of generative AI adoption in this vertical.

Retail and E-Commerce

Personalised product recommendations, AI-generated product descriptions, dynamic pricing models, virtual try-on experiences, and conversational commerce are all driving strong generative AI market growth in retail. India’s massive e-commerce market and the UAE’s thriving luxury retail sector are both accelerating adoption.

Media and Entertainment

AI-generated video, music composition, scriptwriting, visual effects, and interactive content are transforming the media production pipeline. Cost savings from generative AI content creation tools are enabling smaller studios in India and the Middle East to compete with larger productions for the first time.

Manufacturing and Engineering

Generative design tools, predictive maintenance models, synthetic training data for quality inspection, and AI-assisted engineering documentation are creating significant productivity gains. Indian manufacturing corridors and UAE industrial zones are actively piloting these generative AI applications.

Education and EdTech

Personalised learning pathways, AI tutors, automated assessment generation, multilingual content translation, and curriculum design automation are reshaping the generative AI market’s role in education. Both India’s massive EdTech ecosystem and UAE’s national digital education initiatives represent significant market opportunities.

Regional Generative AI Market Size and Growth Insights

Regional dynamics play a defining role in shaping generative AI market growth trajectories. North America currently leads by revenue share, but the most compelling growth stories in the 2026 to 2032 forecast window are unfolding in Asia Pacific particularly India and the Middle East, specifically the UAE.

| Region | 2025 Revenue Share | Growth Rate | Key Drivers |

|---|---|---|---|

| North America | ~43% | High | Enterprise adoption, frontier model labs, cloud infrastructure |

| Europe | ~23% | Strong (43% CAGR) | AI Act compliance driving structured adoption, fintech, auto |

| Asia Pacific (India) | Growing fast | Fastest region | IT sector, digital SMEs, govt mandates, low-cost AI talent |

| Middle East (UAE) | Emerging | Very High | AI mandates, $4B private investment, 80%+ enterprise adoption |

| Latin America / Africa | ~5% | Moderate | SME digitisation, open-source model access, mobile-first AI |

India’s generative AI market deserves special emphasis. As the fastest-growing market in Asia Pacific, India benefits from a massive pool of AI-skilled engineers, a vibrant startup ecosystem, and an enterprise IT sector that is deeply familiar with cloud infrastructure. The India generative AI market is projected to reach $8.3 billion by 2030. From our direct engagement with Indian technology leaders in cities including Bengaluru, Hyderabad, Mumbai, and Pune, we see generative AI being embedded across BPO operations, banking platforms, healthcare record systems, and e-governance applications.

In the UAE, particularly in Dubai’s smart city and financial technology corridors, the generative AI market is accelerating rapidly. Stanford University’s AI Index 2026 identifies the UAE as a top-tier nation for AI adoption. With private AI investment reaching $4 billion and an organisational AI adoption rate exceeding 80 percent among employees, the UAE has built the conditions for an outsized generative AI market presence relative to its population size.

Competitive Landscape of the Generative AI Market

The competitive landscape of the generative AI market is characterised by high concentration at the top tier and intense fragmentation in specialised niches. The five largest players OpenAI, Microsoft, Google, NVIDIA, and Anthropic collectively held 58.1 percent of global market share in 2025. This concentration reflects the enormous capital requirements for training frontier models and the network effects that accrue to platforms with millions of enterprise users.

However, the competitive picture below the top tier is dynamic and increasingly interesting. Companies like Scale AI, Midjourney, H2O.ai, Cohere, and Mistral have carved out strong positions in specialised segments including data labelling, image generation, enterprise NLP, and European-market-compliant models. Adobe’s integration of generative AI into Creative Cloud represents a different competitive strategy embedding AI capabilities within an existing dominant platform rather than competing on model capabilities alone.

Investment Trends Fueling Generative AI Market Growth

Investment flows into the generative AI market have been nothing short of extraordinary. Corporate investment more than doubled in 2025 compared to 2024, driven by a combination of venture capital deployment into startups, hyperscale capital expenditure on AI infrastructure, and enterprise AI budget allocations that are now treated as essential operating line items rather than innovation experiments.

The UAE placed $4 billion in private AI investment in 2025, making it the 15th largest national investor in AI globally a remarkable position for an economy of its size. This investment is being channelled into AI research institutes, startup ecosystems in Abu Dhabi and Dubai, and strategic partnerships with global AI leaders. For context, the US led global private AI investment with over $757 billion, reflecting its position as the primary engine of generative AI market innovation.

India’s investment picture is characterised by the convergence of domestic venture capital, US institutional funding, and government-backed programmes under the National AI Mission. Indian AI startups are attracting attention across generative AI use cases spanning vernacular language models, agricultural AI, legal tech, and healthcare document intelligence. This investment foundation is contributing directly to India’s position as the fastest-growing regional market within Asia Pacific.

Generative AI Market Opportunities Across Sectors

The generative AI market opportunities available to businesses in 2026 span both established technology categories and genuinely new solution spaces that did not exist three years ago. From our advisory practice, we identify the following as the highest-priority opportunity areas for enterprises operating in India and the UAE.

Vernacular and Multilingual AI: With India hosting over 22 officially recognised languages and the UAE serving a population representing over 200 nationalities, the market opportunity for vernacular and multilingual generative AI is immense. Models capable of generating, translating, and understanding content in Hindi, Tamil, Marathi, Arabic, Urdu, and dozens of other languages are dramatically underserved relative to English-language AI capabilities.

Synthetic Data Generation: As privacy regulations tighten globally, the ability to generate high-quality synthetic training data is becoming a critical enterprise capability. This is particularly relevant for healthcare, financial services, and telecom organisations that need large labelled datasets without exposing real customer data.

AI-Augmented Professional Services: The same shift is visible in marketing and digital PR, where AI can speed up content planning, prospecting, and campaign research. But businesses still need reliable platforms to secure real placements, brand mentions, and backlinks. This is where Serpbays link building platform works as a one-stop solution for Digital PR, link insertions, guest posting, and authority backlink placements, allowing users to browse websites, compare placement options, and place orders directly. The firms that build proprietary generative AI workflows first will have a durable competitive advantage over peers who wait. Companies such as Brimcove are helping businesses combine AI-driven strategies with scalable digital growth initiatives to stay ahead in increasingly competitive markets.

SME Democratisation: Accessible SaaS generative AI tools are creating a real opportunity for small and medium enterprises across both markets to access capabilities previously available only to large corporations. This democratisation of the generative AI market is one of the most important structural trends for regional economic competitiveness.

Challenges Impacting Generative AI Market Growth

While the generative AI market growth story is overwhelmingly positive, honest strategic counsel requires acknowledging the real challenges that businesses will encounter as they scale AI adoption. These challenges are neither trivial nor insurmountable, but they require deliberate management.

Data Privacy and Security

Feeding sensitive enterprise data into third-party generative AI systems creates real privacy and security risks. This is a critical concern for healthcare, legal, and financial services firms in both India’s DPDP framework and the UAE’s data protection regulations.

High Infrastructure and Compute Costs

While costs are falling, training large custom models still requires significant compute investment. For many businesses outside the top tier of enterprise, this remains a meaningful barrier to advanced generative AI market participation.

Hallucination and Accuracy Risks

Generative AI models can produce plausible-sounding but factually incorrect outputs. In high-stakes domains medical, legal, financial hallucination risks require robust human-in-the-loop review processes and careful prompt engineering discipline.

AI Talent Shortage

Despite large numbers of AI graduates in India and growing AI education programmes in the UAE, the demand for experienced generative AI practitioners significantly outpaces supply. This talent gap creates salary inflation and project timeline risk for enterprises scaling AI initiatives.

Legacy System Integration

Most enterprises carry significant technical debt in the form of legacy data infrastructure that is incompatible with modern generative AI architectures. The cost and complexity of integration frequently extends project timelines and increases total cost of AI ownership.

Generative AI Market Analysis by Technology and Use Case

A detailed generative AI market analysis by technology reveals that different model architectures are finding distinct homes in the commercial ecosystem. Understanding which technology suits which use case is essential for practitioners tasked with selecting and deploying generative AI solutions.

| Technology | 2026 Market Share | Primary Use Cases | Maturity |

|---|---|---|---|

| Transformers / LLMs | ~41% | Text generation, code assist, document processing, Q&A | Production Ready |

| GANs | ~57.5%* | Image synthesis, video generation, audio deepfakes, gaming | Production Ready |

| Diffusion Models | Growing | High-fidelity image and video, drug molecule design, design generation | Maturing |

| Multimodal Models | 56.6% CAGR | Vision-language tasks, video understanding, cross-modal search | Rapidly Growing |

| AI Agents | Emerging | Autonomous workflow execution, multi-step research, robotic process AI | Early Production |

*GAN share refers to the image/video/audio sub-segment. LLM transformers dominate text-based applications.

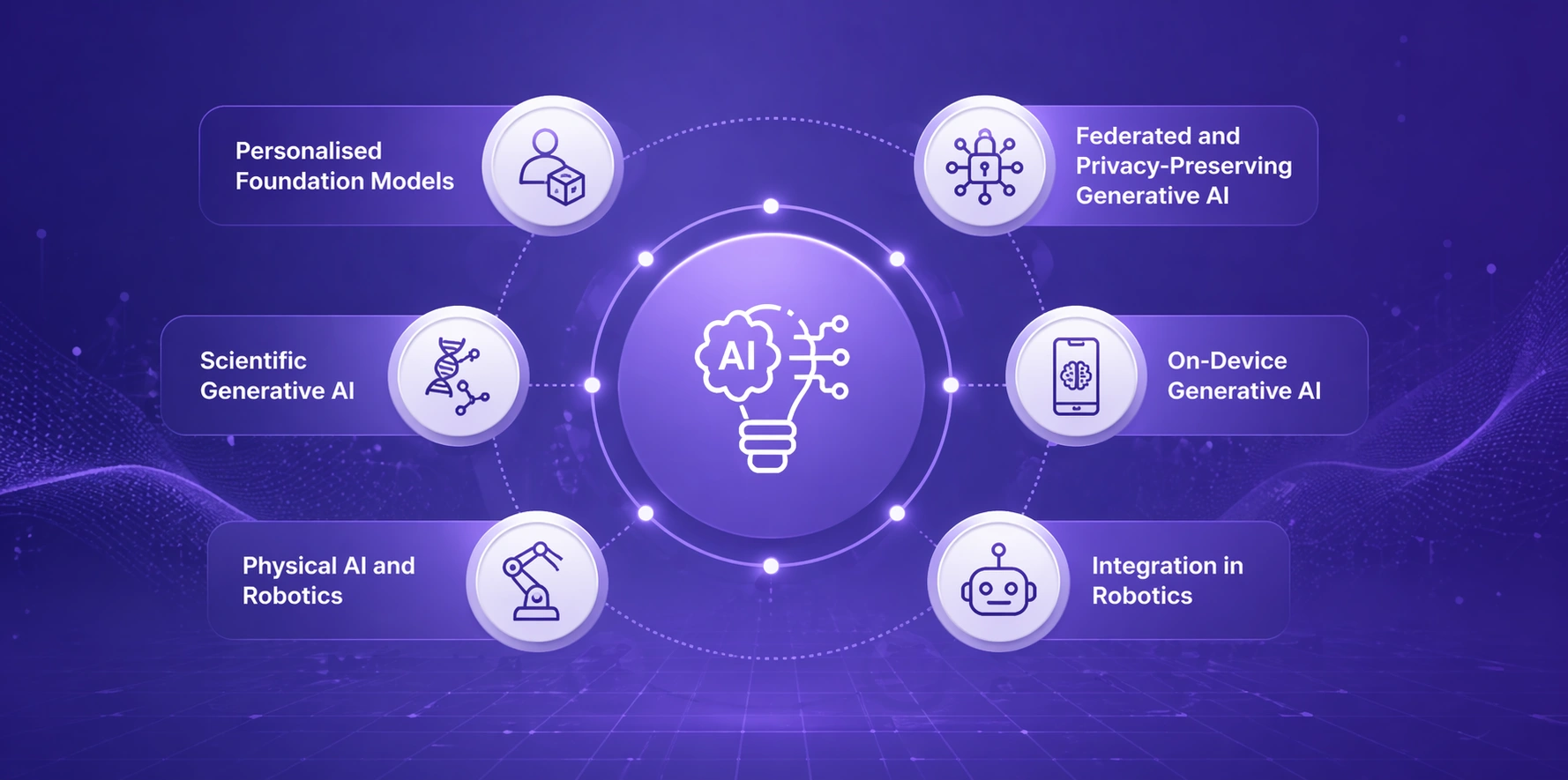

Future Generative AI Market Trends and Innovations

Looking beyond 2026, the generative AI market trends that will define the next phase of growth are already visible in research labs, startup pitches, and enterprise innovation programmes. These are not distant science fiction scenarios they are developments that will reach commercial scale within the 2026 to 2032 forecast window.

Physical AI and Robotics Integration: Generative AI is being fused with physical robotics to create systems that can understand, reason about, and interact with the physical world. This convergence, known as Physical AI in manufacturing automation, will reshape manufacturing and logistics in India’s industrial corridors and the UAE’s automated port and logistics operations.

On-Device Generative AI: Model compression and specialised AI silicon are enabling powerful generative AI to run directly on smartphones and edge devices. This shift will expand the generative AI market into regions and use cases where cloud connectivity is limited, including rural India and remote operational sites in the Middle East.

Scientific Generative AI: Generative AI is accelerating scientific discovery in materials science, climate modelling, genomics, and fundamental physics. The ability to generate and evaluate hypotheses at machine speed is compressing research timelines that previously took decades. Leading Indian research institutions and UAE science cities are investing to capture this innovation wave.

Federated and Privacy-Preserving Generative AI: New training paradigms that allow model training across distributed datasets without centralising sensitive data will unlock generative AI in highly regulated industries. This innovation is critical for healthcare and financial services applications in both the India and UAE markets.

Personalised Foundation Models: The next frontier is foundation models that adapt dynamically to individual user preferences, organisational knowledge bases, and real-time context going far beyond today’s static fine-tuning approaches. This will make generative AI outputs dramatically more relevant and accurate for specific business contexts.

Long-Term Generative AI Market Forecast Analysis and Outlook

The long-term generative AI market forecast analysis through 2032 and beyond presents a picture of sustained, structural growth rather than a cyclical technology bubble. The fundamental drivers automation demand, digital transformation imperatives, falling AI costs, and expanding model capabilities are durable trends rooted in economic necessity rather than novelty alone.

Based on our eight-plus years of market advisory experience and synthesis of leading research, the generative AI market forecast analysis for the period 2026 to 2032 points to a market that will likely exceed $800 billion in conservative estimates and could approach $1.3 trillion in optimistic scenarios that assume continued breakthroughs in model efficiency and capability. The range of outcomes reflects genuine uncertainty around the pace of regulatory developments, compute cost trajectories, and the timing of next-generation AI architectures.

For businesses operating in India and the UAE, the long-term generative AI market forecast analysis carries a clear strategic implication: the window for building genuine AI capability at a manageable cost is open now but will narrow as talent becomes scarcer and competitive differentiation through AI becomes harder to achieve for late movers. The enterprises that invest deliberately and build proprietary AI capabilities in 2026 and 2027 will establish structural advantages that compound over the following five years.

At the macro level, the generative AI market is evolving from a set of point solutions into critical digital infrastructure as foundational to enterprise operations in 2032 as cloud computing became by 2020. Businesses that treat generative AI as infrastructure rather than an optional enhancement will be the ones best positioned to capture value from the generative AI market growth that the next six years will deliver.

Generative AI Market: Key Outlook Summary

Partner with Generative AI Market Experts

With 8+ years guiding enterprises across India and UAE, we turn generative AI market insights into tangible competitive advantage for your business.

People Also Ask

Q1.What is the generative AI market and why is it growing so fast?

The generative AI market refers to the global ecosystem of AI tools, platforms, and services that create text, images, code, audio, and video. It is growing rapidly due to soaring enterprise adoption, falling compute costs, and massive investment from both private firms and governments worldwide.

Q2.How big is the generative AI market in 2026?

Multiple research firms estimate the generative AI market size at between $83 billion and $161 billion in 2026, depending on the scope of measurement. The market is forecast to exceed $890 billion by 2032, reflecting a compound annual growth rate of over 40 percent across most projections.

Q3.Which industries are adopting generative AI the fastest?

Healthcare, financial services, retail, and media are leading early adopters. Healthcare uses generative AI for drug discovery and patient engagement, while finance relies on it for fraud detection, report generation, and risk analysis. Retail and media use it heavily for personalized content and customer support.

Q4.Is the generative AI market relevant for businesses in India?

Absolutely. India is among the fastest-growing markets for generative AI in Asia Pacific, with projections pointing to over $8 billion in market size by 2030. Indian enterprises across IT, banking, and e-commerce are actively embedding generative AI into operations to cut costs and improve service delivery.

Q5.How is the UAE positioned in the global generative AI market?

The UAE, particularly Dubai, is a global front-runner in AI adoption. Stanford University’s AI Index Report ranks the UAE among the top nations for AI adoption and talent. The country has placed $4 billion in private AI investment and over 80 percent of employees in the UAE regularly use AI at work.

Q6.What are the biggest generative AI market trends right now?

Key trends include the rise of multimodal AI models, AI agent automation, enterprise SaaS embedding of generative AI, increased regulatory frameworks, and the shift from pilot projects to full-scale production deployment. Domain-specific foundation models are also accelerating industry adoption.

Q7.What are the main challenges slowing down generative AI market growth?

Data privacy concerns, high compute infrastructure costs, integration complexity with legacy systems, regulatory uncertainty, and a shortage of AI-skilled talent are the primary barriers businesses face when scaling generative AI solutions across their organizations.

Q8.Who are the leading companies in the generative AI market?

OpenAI, Microsoft, Google, NVIDIA, Anthropic, Adobe, Amazon Web Services, and IBM are among the dominant players. Collectively the top five companies held over 58 percent of the global generative AI market share in 2025, signaling high concentration at the top end.

Q9.. What is the generative AI market forecast for 2032?

According to MarketsandMarkets, the generative AI market is forecast to reach $890.59 billion by 2032, growing at a CAGR of 43.4 percent. Fortune Business Insights projects an even higher figure of $1.26 trillion by 2034, while Grand View Research estimates $324.68 billion by 2033 at a CAGR of 40.8 percent.

Q10.How should a business start using generative AI to stay competitive?

Begin with a clear use-case audit to identify where generative AI can save time or improve quality. Start with low-risk pilots in content creation, customer support, or internal documentation. Then scale using SaaS-based generative AI platforms before moving to custom model fine-tuning aligned with your data.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.