Ai Overview

The banking industry has changed more in the last five years than it did in the previous twenty. According to PYMNTS Intelligence research, 75% of banks struggle to implement new digital payment solutions because their old infrastructure simply cannot keep up. With IT turnover costs ranging from $50,000 to $100,000 per employee, preventing even a few employees from leaving pays back the training investment within 12 to 18 months. Given that legacy systems eat up to 70% of IT budgets, this savings is significant.

Key Takeaways

- The global core banking software market was valued at USD 16.79 billion in 2024 and is expected to reach USD 64.96 billion by 2032, growing at a CAGR of 18.6%, showing how fast banks are investing in software upgrades and integration tools.

[1] - About 75% of banks face difficulties when trying to add new digital payment solutions because their old infrastructure cannot support modern technology, according to PYMNTS Intelligence research.

[2] - Nearly 47% of financial institutions are choosing to upgrade their core systems step by step using APIs rather than doing a full system replacement, which only 13% of banks attempt.

[3] - Open banking API call volume globally reached 137 billion in 2025 and is projected to grow by 427% to 722 billion by 2029, showing the massive role APIs play in financial system integration.

- A 10x Banking study from June 2024 found that 55% of banks view their legacy core banking systems as the biggest roadblock to achieving their digital transformation goals.

[4] - The global real-time payments market was valued at USD 24.91 billion in 2024 and is projected to reach USD 284.49 billion by 2032 at a CAGR of 35.4%, proving how important real-time payment system integration has become.

[5]

Banks today are stuck between two worlds. On one side, they have systems that were built decades ago, many of them still running on programming languages like COBOL. On the other side, customers expect instant payments, mobile banking, and smooth digital experiences. The gap between these two sides is growing wider, and banks that do not act fast enough risk losing customers to fintech companies and digital-only banks.

This is where the need to integrate with existing banking systems becomes unavoidable. Whether a bank wants to add real-time payments, connect with fintech partners, or simply offer mobile banking, it must find a way to connect its old systems with new technology. This process is what we call banking system integration, and it is one of the most important topics in the financial world right now.

In this blog, we will walk through everything you need to know about bank integration solutions, from understanding why integration matters, to the tools and methods used, to the challenges banks face, and the strategies that actually work. Whether you are a fintech startup looking to connect with banks or a financial institution planning to upgrade, this guide will give you a clear picture of how payment system integration and financial system integration work in practice.

Why Banks Need to Integrate with Existing Banking Systems

The banking industry has changed more in the last five years than it did in the previous twenty. Customers no longer want to visit a branch or wait for a check to clear. They want to send money instantly, check their balance on their phone, and manage their finances from a single app. But most banks were not built for this kind of speed.

According to PYMNTS Intelligence research, 75% of banks struggle to implement new digital payment solutions because their old infrastructure simply cannot keep up. And it is not just about technology. Fintechs and digital banks captured 47% of new account openings in the first half of 2023, up from 36% in 2020. That is a huge shift in customer behavior, and traditional banks are feeling the pressure.

The answer is not to throw away everything and start fresh. That is too risky and too expensive. Instead, banks need to integrate with existing banking systems by connecting their legacy platforms with modern tools. This allows them to offer new services without rebuilding from scratch. It is like adding a new engine to an old car rather than buying a completely new vehicle.

Banking system integration also matters for regulatory reasons. Governments around the world are pushing for open banking, which means banks must share customer data (with permission) through APIs. In Europe, PSD2 regulations require this, and in the United States, the Consumer Financial Protection Bureau finalized its Section 1033 rule in October 2024, which mandates banks to share consumer authorized financial data with third parties.

Understanding the Current State of Banking Infrastructure

Before we talk about solutions, let us look at where banks stand right now. The picture is not great for most traditional financial institutions.

A study by 10x Banking conducted in June 2024 surveyed over 200 senior IT decision makers and found that 55% of banks see their core banking systems as the single biggest barrier to digital goals. On top of that, 53% of institutions using legacy systems struggle to grow their operations because of data silos and production bottlenecks.

Research from Basikon shows that 43% of financial institutions still run on systems that are more than 20 years old. Maintaining these old systems consumes up to 70% of their IT budgets. That means out of every dollar a bank spends on technology, 70 cents goes toward just keeping the lights on, not building anything new.

The talent problem makes things worse. The engineers who built these old systems are retiring, and younger developers do not want to work with outdated technologies. COBOL programmers, who are critical for maintaining many banking cores, are becoming harder to find and more expensive to hire. According to Forrester, 95% of ATM transactions still depend on COBOL, and there are around 220 billion lines of COBOL code in use globally.

These numbers make one thing very clear: banks cannot keep running on old systems forever. They need proper bank integration solutions to connect their existing infrastructure with the tools and technologies that modern customers demand.

Recommended Reading:

BFSI Software Market Growth A Comprehensive Statistical Review 2024 – 2034

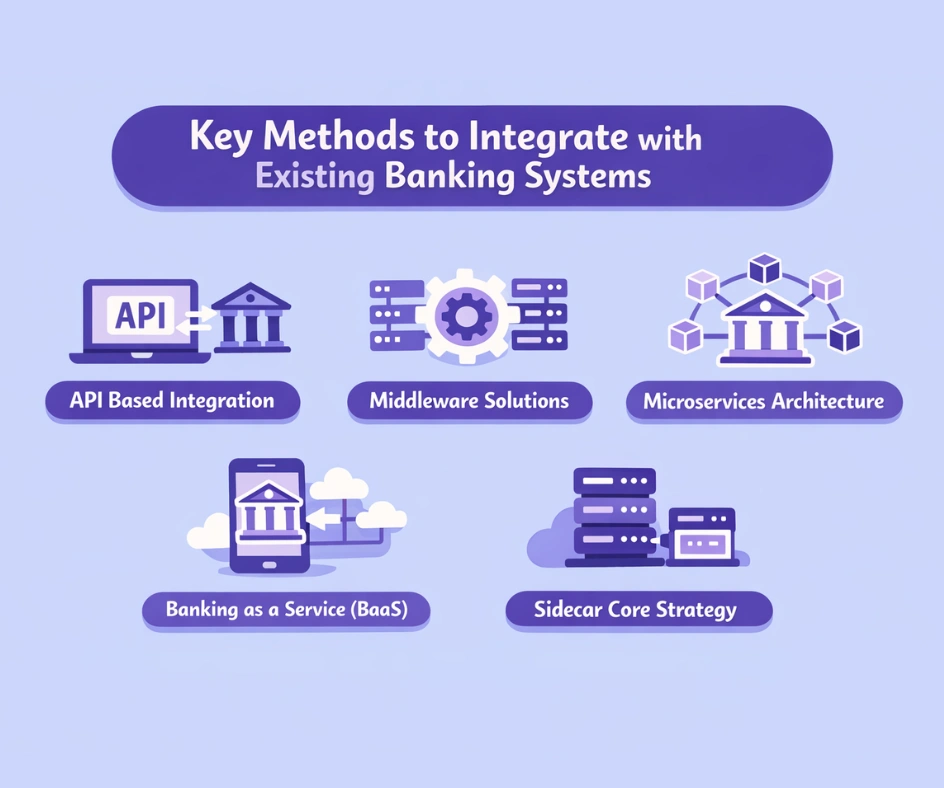

Key Methods to Integrate with Existing Banking Systems

There is no single way to connect old systems with new ones. Banks and fintech companies use several different approaches depending on what they need, how much they can spend, and how much risk they are willing to take. Here are the main methods used for financial system integration.

1. API Based Integration

APIs (Application Programming Interfaces) are by far the most popular method for modern banking system integration. Think of an API as a waiter in a restaurant. The customer (your app) tells the waiter (the API) what they want, and the waiter goes to the kitchen (the bank’s core system), gets the order, and brings it back.

In 2025, more than 81% of banks have adopted open banking APIs, with the United States leading at 97% of financial institutions. Global API usage reached 137 billion calls, marking a sharp year-over-year increase. On average, banks now offer 16 APIs each, with account information services making up 63% of total API traffic.

The beauty of API based integration is that it lets banks keep their old core systems while adding new features on top. A fintech company can connect to a bank’s API to access account information, start payments, or verify identities, all without touching the bank’s core platform.

2. Middleware Solutions

Middleware acts as a bridge between old and new systems. It sits in the middle and translates data between different formats and protocols. For banks with very old systems that cannot support modern APIs directly, middleware is often the first step toward integration.

Middleware solutions handle things like message routing, data transformation, and protocol conversion. For example, if a bank’s old system communicates using SOAP (an older messaging format) and the new app uses REST (a modern format), middleware can translate between the two so they can talk to each other.

3. Microservices Architecture

Instead of having one big system that does everything (called a monolithic system), banks can break their functions into small, independent services. Each microservice handles one specific task, like processing payments, managing accounts, or handling customer authentication.

This approach makes it much easier to update or replace individual parts of the system without affecting the rest. If the payment processing service needs an upgrade, the bank can update just that piece without touching the account management system.

4. Banking as a Service (BaaS)

BaaS is a model where banks open up their core services, like account creation, payments, and lending, as APIs that other companies can use. This lets fintech companies build their own products on top of a bank’s infrastructure without needing their own banking license.

According to a study by Finastra, BaaS is expected to grow by 25% over the next three years, and 86% of market players are planning to adopt open APIs to enable banking capabilities. This approach helps banks earn revenue from their existing systems while also reaching customers through third-party apps.

5. Sidecar Core Strategy

This is a newer approach where banks run a modern core system alongside their legacy system. The old system keeps handling existing operations, while the new system handles new customers or new products. Over time, the bank gradually moves more functions to the new system.

IDC projects that by 2026, 40% of global banks will use sidecar strategies, running modern cores alongside legacy systems. By 2028, that number is expected to reach 70 to 80%. This approach reduces risk because the old system is still there as a backup, and any problems with the new system stay isolated.

The Role of APIs in Payment System Integration

APIs deserve their own section because they are the backbone of modern payment system integration. Without APIs, most of the financial services we use daily, from mobile banking apps to payment gateways, simply would not work.

Here is how APIs are transforming banking:

Payment Processing: APIs allow businesses to accept payments directly from customers’ bank accounts, bypassing traditional card networks. Account-to-account (A2A) payments, powered by open banking APIs, are growing fast because they reduce transaction fees for both merchants and consumers.

Identity Verification: Instead of asking customers to fill out long forms, banks can use KYC (Know Your Customer) APIs to verify identities instantly by cross-checking government records. This speeds up the onboarding process from days to minutes.

Account Aggregation: APIs like those provided by Plaid and Yodlee allow customers to view accounts from multiple banks in one place. These APIs connect to over 16,000 global data sources and normalize financial information into a single, easy-to-read format.

Credit Scoring: Lending platforms use APIs to instantly access a customer’s financial data, assess their creditworthiness, and approve or deny loans in real time. This has turned loan processing from a weeks-long process into something that happens in minutes.

The open banking market itself shows just how important APIs have become. According to Grand View Research, the global open banking market was valued at USD 31.61 billion in 2024 and is projected to reach USD 135.17 billion by 2030, growing at a CAGR of 27.6%.

Common Banking Integration Approaches Compared

| Integration Method | Best For | Key Considerations |

|---|---|---|

| API Based Integration | Banks with some modern capabilities are looking to connect with fintech partners and third-party apps | Requires API gateway infrastructure, ongoing documentation, and developer support for external partners |

| Middleware Solutions | Banks with very old core systems that cannot directly support modern API connections | Acts as a translator between legacy protocols (SOAP) and modern formats (REST), adding a layer of complexity |

| Microservices Architecture | Banks that want to modernize gradually by breaking their system into small, independent components | Allows updating individual functions without affecting the whole system, and needs strong DevOps practices |

| Banking as a Service (BaaS) | Banks want to earn new revenue by letting fintech companies build products on their infrastructure | Expected to grow 25% over the next three years, requires strong compliance and partner management |

| Sidecar Core Strategy | Banks that want to test modern systems with a small customer base before fully switching over | 40% of global banks are expected to adopt by 2026, keep legacy as backup, and reduce migration risk |

| Full Core Replacement | Banks that have the budget and time for a complete overhaul of their entire technology stack | Only 13% of banks choose this path, high risk and can cost over $1 billion (Commonwealth Bank spent 5 years) |

| Cloud-Based Integration | Banks are looking to reduce infrastructure costs and gain flexibility in deployment and scaling | 62.5% of real-time payment platforms use cloud deployment, which supports multi-region operations |

Challenges of Banking System Integration

Connecting old and new systems sounds great in theory, but in practice, it is full of obstacles. Understanding these challenges is the first step to overcoming them. Here are the most common problems banks face when trying to integrate with existing banking systems.

1. Legacy System Complexity

Most banking cores were built as monolithic systems where everything is connected to everything else. Changing one part can break another. This tangled web of connections is what bankers often call “spaghetti architecture.” According to the PYMNTS report, 59% of bankers describe their legacy systems as a “spaghetti” of interconnected but outdated technologies. This makes even small changes risky and time-consuming.

2. Data Migration Risks

Moving data from old systems to new ones is one of the riskiest parts of any integration project. Banks deal with millions of customer records, transaction histories, and regulatory data. If even a small amount of data gets lost or corrupted during migration, the consequences can be serious, from regulatory fines to loss of customer trust.

3. Regulatory Compliance

Banks operate in one of the most heavily regulated industries in the world. Any change to their systems must meet strict rules around data privacy, anti-money laundering (AML), and know your customer (KYC) requirements. Different countries have different rules, which makes financial system integration even harder for banks that operate across borders.

4. Security Concerns

Every new connection point between systems is a potential entry point for hackers. According to FIS and Oxford Economics research, the average financial institution loses $93.6 million per year due to various issues tied to outdated systems and security vulnerabilities. Banks must ensure that every integration point is protected with proper encryption, authentication, and monitoring.

5. Talent Shortage

Finding people who understand both old banking systems and modern technology is extremely difficult. Research shows that 78% of banking leaders are prioritizing upskilling to stay competitive, with 70% of banking roles requiring new digital skills. At the same time, IT turnover costs in banking range from $50,000 to $100,000 per employee, making the talent gap expensive to manage.

6. Cost and Time Overruns

Integration projects are notorious for going over budget and over time. Commonwealth Bank of Australia spent over $1 billion and five years replacing its legacy core. German institutions have abandoned entire modernization programs after years of work and hundreds of millions spent. These stories make many banks hesitant to even begin the process.

Recommended Reading:

How Cryptocurrency Banking Applications Improve Financial Access

Real Time Payments and Financial System Integration

One of the biggest drivers behind the push to integrate with existing banking systems is the demand for real-time payments. Customers and businesses no longer want to wait hours or days for their money to move. They want it done in seconds.

The numbers tell a powerful story. Real-time payment transactions globally grew by 42.2% in 2023, reaching 266.2 billion transactions. The global real-time payments market was valued at USD 24.91 billion in 2024 and is projected to grow to USD 284.49 billion by 2032, at a CAGR of 35.4%.

In India, the UPI (Unified Payments Interface) system processed approximately 25.1 trillion rupees (around $293 billion) in transactions in May 2025 alone, making it the largest real-time payment system by volume in the world. Brazil’s PIX system handled over 41 billion transactions in 2023, with more than 70% of the adult population using it. In Europe, the SEPA Instant Credit Transfer limit was raised to 1 million euros in 2025, enabling real-time settlement for business payments across the EU.

For banks, supporting real-time payments means their systems must be able to process transactions 24 hours a day, 7 days a week, 365 days a year. This is a huge shift from the old batch processing model, where transactions were grouped together and processed at specific times. Payment system integration for real-time capabilities requires upgrades to payment rails, fraud detection systems, and settlement infrastructure.

In the United States, two real-time payment systems are now operating: The Clearing House’s RTP network and the Federal Reserve’s FedNow Service. The RTP network set multiple records in early 2024, including 76 million transactions in a single quarter. Banks that want to participate in these networks must ensure their systems can handle instant transaction processing, immediate confirmation, and round-the-clock availability.

Step-by-Step Process for Banking System Integration

Integrating old banking systems with new technology is not something you can do over a weekend. It requires careful planning, testing, and execution. Here is a practical step-by-step approach that banks and fintech companies follow for successful bank integration solutions.

1. Audit Your Current Systems

The first step is to understand exactly what you are working with. Map out every system, database, and connection in your current technology stack. Identify which systems are most critical, which ones are the most outdated, and where the biggest pain points are. This audit will help you prioritize what needs to be integrated first.

2. Define Your Integration Goals

What exactly do you want to achieve? Are you trying to add mobile banking? Enable real-time payments? Connect with fintech partners? Each goal will require a different type of integration. Be specific about what you need and set measurable targets so you can track progress.

3. Choose the Right Integration Method

Based on your current systems and your goals, decide which approach makes the most sense. For most banks, a combination of API based integration and middleware works best. If your systems are extremely old, you might need middleware first to create API layers on top of legacy systems. If you are starting fresh, a microservices approach gives you the most flexibility.

4. Start with a Data Assessment

BAI research shows that most archived data receives minimal access after the first 18 months, which means not everything needs to be migrated right away. Start your data assessment six to nine months before migration begins. Clean your data, remove duplicates, and categorize what needs to move now versus what can wait.

5. Build and Test in Stages

Never try to integrate everything at once. Start with a small, low-risk part of the system, build the integration, test it thoroughly, and only then move on to the next piece. This is why the sidecar approach is gaining popularity. You can test new systems with 1 to 5% of your customer base before rolling out to everyone.

6. Invest in Team Training

Integration is not just a technology project. Your people need to understand the new systems. Banks that invest in reskilling report 33% higher employee retention rates. With IT turnover costs ranging from $50,000 to $100,000 per employee, preventing even a few employees from leaving pays back the training investment within 12 to 18 months.

7. Monitor, Measure, and Improve

After integration, the work is not over. You need to continuously monitor performance, track key metrics, and make improvements. Set up dashboards that show transaction processing times, system uptime, error rates, and customer satisfaction scores. Use this data to identify and fix issues before they become major problems.

Open Banking and Its Impact on Bank Integration Solutions

Open banking is probably the single biggest force pushing banks to integrate with existing banking systems right now. It is a regulatory and technology framework that requires banks to share customer data (with the customer’s permission) through standardized APIs.

The concept started in Europe with the PSD2 directive and has since spread to dozens of countries. Here is where open banking stands today:

In the UK, open banking reached 16.5 million user connections by December 2025, up from 12.1 million the year before. The ecosystem recorded 24.0 billion successful API calls in 2025, a 27% increase over 2024. Payment volumes climbed to 351 million, a 57% increase year over year.

In Brazil, open banking already has over 9.8 million users, making it the leader in Latin America. India’s Account Aggregator Framework supports over 1.2 billion API calls per quarter, one of the fastest-growing systems in the world. In Australia, more than 90 accredited data recipients now participate in the Consumer Data Right (CDR) program.

For banks, open banking creates both opportunities and requirements. On one hand, it forces banks to invest in banking system integration to meet regulatory demands. On the other hand, it opens up new revenue streams by allowing banks to offer their services through third-party apps and platforms.

The global open banking market was valued at USD 30.89 billion in 2024 and is expected to grow to USD 38.86 billion in 2025, showing strong year over year expansion. By 2030, Grand View Research projects it will reach USD 135.17 billion. These numbers make it clear that open banking is not a trend. It is the future of financial services, and every bank must prepare for it.

Key Statistics on Global Banking System Integration

| Metric | Value | Source |

|---|---|---|

| Core Banking Software Market (2024) | USD 16.79 billion | Fortune Business Insights |

| Core Banking Software Market (2032 Projection) | USD 64.96 billion (CAGR 18.6%) | Fortune Business Insights |

| Open Banking Market (2024) | USD 31.61 billion | Grand View Research |

| Open Banking API Calls (2025) | 137 billion globally | Juniper Research |

| Real Time Payments Market (2024) | USD 24.91 billion | Fortune Business Insights |

| Banks Struggling with Legacy Infrastructure | 75% of banks | PYMNTS Intelligence |

| Banks Adopting Open Banking APIs (2025) | 81% globally, 97% in the US | Market.us |

| IT Budget Spent on Legacy Maintenance | Up to 70% | Basikon Research |

| Global Real Time Transactions (2023) | 266.2 billion transactions (42.2% YoY growth) | ACI Worldwide |

How AI and Blockchain Are Changing Financial System Integration

Two technologies are having a major impact on how banks integrate with existing banking systems: artificial intelligence and blockchain.

1. Artificial Intelligence in Banking Integration

AI is being used in several ways to make integration easier and more effective:

Legacy Code Translation: One of the biggest challenges in integration is understanding old code. AI tools can now analyze, translate, and modernize legacy code written in languages like COBOL, freeing up developers for higher-value work. This addresses one of the most pressing problems in banking: the shortage of people who understand legacy systems.

Fraud Detection: AI-powered fraud detection systems analyze more than 500 variables per transaction to identify suspicious patterns. The global AI in fraud detection market was valued at $15.1 billion in 2024 and is projected to reach $23.4 billion by 2026, a 55% growth rate. Integration of AI fraud detection with existing payment systems has become a top priority for banks.

Customer Service: AI chatbots integrated with banking systems handle routine customer queries 24/7. Over 37% of Americans have already interacted with a bank chatbot, and that number is expected to grow to 110.9 million users by 2026.

2. Blockchain in Banking Integration

Blockchain technology is being tested and used by banks in several areas:

Cross-Border Payments: In 2024, stablecoin transaction volumes reached $32 trillion, with $6 trillion going specifically toward payments. This accounted for roughly 3% of the estimated $195 trillion in global cross-border payments. Blockchain removes intermediaries from cross-border transactions, reducing costs and processing time.

Smart Contracts: These self-executing contracts automate banking processes like loan disbursements, insurance claims, and trade settlements. When predefined conditions are met, the contract executes automatically without any human involvement.

Digital Identity: Blockchain-based identity systems allow banks to verify customers once and share that verification across multiple platforms, reducing the need for repeated KYC processes.

According to a report, blockchain-based transaction verification is being tested in over 27% of Tier 1 global banks, showing that this technology is moving beyond experiments into real-world use.

Recommended Reading:

Benefits of Successful Banking System Integration

When done right, banking system integration delivers real, measurable benefits. Here is what banks can expect after a successful integration project.

1. Reduced Maintenance Costs

Banks that implement unified platform solutions report a 40% reduction in system maintenance costs, according to the Federal Reserve’s banking operations survey. Given that legacy systems eat up to 70% of IT budgets, this savings is significant. It frees up funds that can be redirected toward innovation and new product development.

2. Faster Time to Market

With proper API integration, companies can launch fintech products 70 to 80% faster than building banking infrastructure from scratch. What used to take 2 to 5 years can now be done in months. This speed advantage is critical in a market where customer expectations change rapidly.

3. Better Customer Experience

Integration enables banks to offer the kind of digital experiences that customers now expect: instant payments, real-time balance updates, personalized product recommendations, and smooth mobile banking. The fact that 85% of American adults now use mobile banking shows how important these digital capabilities have become.

4. New Revenue Streams

Through BaaS and open banking APIs, banks can earn revenue from their existing infrastructure by letting other companies build on top of it. This turns the bank from a service provider into a platform, similar to how Apple earns revenue from apps built on its platform.

5. Improved Compliance

Modern integrated systems make it easier to track transactions, generate audit trails, and meet regulatory requirements. With 80% of major banks now using regulatory technology (RegTech) solutions integrated into their digital banking platforms, compliance has shifted from being a burden to being automated.

6. Stronger Security

Integrated systems with modern security layers provide better protection than patched-up legacy systems. Features like biometric authentication, real-time fraud monitoring, and encryption are much easier to implement and maintain on modern platforms. AI-based fraud detection systems that analyze hundreds of variables per transaction can be layered on top of existing banking systems through API integration.

Real World Banking Integration Projects

The following projects show how modern integration principles are already being applied in fintech, crypto payments, and cross-border financial services. Each project demonstrates the same API driven, multi-system integration approach discussed throughout this blog, from payment gateway connections and banking infrastructure bridges to identity verification and real-time transaction processing.

💳

Tarality: Crypto to Banking Bridge Platform

Built a comprehensive platform that merges traditional financial services with crypto capabilities. The system supports direct bank transfers, INR trading pairs, crypto-backed lending, Buy Now Pay Later features, and fixed deposit options, all integrated with India’s banking infrastructure for withdrawals to bank accounts and digital wallets.

📱

INRx Pay: Crypto UPI Payment Integration

Developed India’s first all-in-one crypto payment and utility app that connects cryptocurrency holdings with the country’s UPI banking network. Users can send crypto to bank accounts, UPI IDs, and phone numbers, pay utility bills, recharge mobile services, and book travel, all powered by real-time integration with India’s payment infrastructure.

Build Your Banking Integration Solution Today:

Our specialized team handles everything from API development and middleware setup to payment gateway integration and legacy system modernization. Whether you need to connect your fintech app with banking infrastructure or modernize your bank’s core systems, we build solutions that work across traditional and blockchain-powered financial networks.

Final Thoughts

The need to integrate with existing banking systems is no longer optional for financial institutions. With 75% of banks struggling to implement new digital solutions because of outdated infrastructure, and fintechs capturing a growing share of new customers, the pressure to modernize is real and growing every day.

The good news is that banks do not need to replace everything at once. Methods like API based integration, middleware solutions, sidecar core strategies, and BaaS models give banks flexible paths forward. Nearly 47% of financial institutions are already pursuing step-by-step upgrades using APIs, proving that incremental approaches work.

The market data support this direction. The core banking software market is growing at 18.6% CAGR, the open banking market is on track to reach $135 billion by 2030, and real-time payments are expanding at 35% CAGR. These are not small numbers. They represent a fundamental shift in how financial services operate.

For banks, the message is clear: start now, start small, and keep moving. For fintech companies, the opportunity lies in building bank integration solutions that connect smoothly with the systems banks already have. And for businesses of all kinds, understanding financial system integration will be important as banking increasingly becomes embedded in everyday apps and services.

The banks that figure out how to connect their old infrastructure with new technology will be the ones that survive and grow. The ones that do not will find themselves losing customers, talent, and market share to competitors who moved faster.

Frequently Asked Questions

Q1.What does it mean to integrate with existing banking systems?

It means connecting a bank’s old or current technology infrastructure with new software, apps, or services. This is usually done through APIs, middleware, or other tools so that old systems and new systems can share data and work together without replacing the entire setup.

Q2.Why is banking system integration important for banks?

Banks need integration to offer modern services like mobile banking, real-time payments, and fintech partnerships. Without integration, banks cannot meet customer expectations, comply with open banking rules, or compete with digital-only banks that already offer these features.

Q3.What are the biggest challenges of payment system integration?

The main challenges include dealing with complex legacy systems, managing data migration risks, meeting strict regulatory requirements, finding talented professionals who understand both old and new technology, and controlling costs that can quickly go over budget.

Q4.How long does a banking integration project take?

It depends on the scope. Basic API integrations can be completed in weeks to a few months. Larger projects like core system replacements can take anywhere from one to five years. Most banks today prefer step-by-step approaches that deliver results in shorter cycles.

Q5.What role do APIs play in bank integration solutions?

APIs are the primary tool for modern banking integration. They allow different systems to communicate and share data in real time. Over 81% of banks globally have adopted open banking APIs, and global API call volume reached 137 billion in 2025, showing how central they are to the process.

Q6.Can small banks afford financial system integration?

Yes, small banks can start with affordable options like cloud-based integration platforms and Banking as a Service (BaaS) APIs. These solutions do not require massive upfront investment. Cloud-based real-time payment platforms, which 62.5% of the market uses, offer lower infrastructure costs and the ability to start small and grow over time.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.