Ai Overview

The landscape for NRI buying property India 2026 has evolved materially from what it was even three years ago. This creates a clean, fully repatriable fund trail that avoids the $1 million annual cap on NRO repatriation and simplifies the 15CA and 15CB compliance process when you eventually sell the property years later. 5% with no double taxation concern, making UAE the most tax-efficient NRI base for Indian property investment.

Key Takeaways

- 01. NRI property tax India 2026 rules apply 12.5 percent LTCG tax without indexation on properties sold after two years of holding from the sale date.

- 02. TDS on NRI property sale 2026 is deducted by the buyer at 20 percent for long-term and 30 percent for short-term capital gains before any payment.

- 03. FEMA rules NRI property India prohibit purchase of agricultural land, plantation property and farmhouses without prior RBI approval under any circumstance.

- 04. OCI property rules India are identical to NRI rules, allowing residential and commercial property purchase but prohibiting agricultural land and farmhouses.

- 05. NRE NRO account property purchase rules differ significantly, with NRE funds being fully repatriable but NRO funds subject to a $1 million annual repatriation cap.

- 06. Section 54 exemption NRI allows complete capital gains tax savings when sale proceeds are reinvested in one residential property within prescribed time limits.

- 07. DTAA India NRI property provisions allow NRIs in UAE, USA, UK, and Singapore to avoid being taxed twice on the same Indian property income legally.

- 08. Form 15CA 15CB NRI property repatriation is mandatory before any bank transfer of sale proceeds abroad and requires chartered accountant certification.

- 09. Real estate tokenization India 2026 allows NRIs to invest from as low as Rs 10,000 in fractional property with lower tax complexity than direct ownership.

- 10. Lower TDS certificate NRI through Form 13 can save lakhs in upfront tax deduction when actual capital gains tax liability is lower than the standard TDS rate.

Over eight years of advising NRI clients across Singapore, Dubai, the UK, and the United States, our firm has handled hundreds of Indian property transactions for non-resident investors. The single biggest source of financial loss we see, consistently, is not the property market itself but the tax and compliance mistakes made during buying, selling, and repatriation. NRI property tax India 2026 rules have seen significant updates through Budget changes, FEMA amendments, and the rapid emergence of new investment vehicles including real estate tokenization that are fundamentally changing how non-resident Indians invest in Indian property.

This guide covers everything an NRI needs to know about buying property in India 2026, selling property tax implications,[1] TDS obligations, capital gains treatment, DTAA benefits, repatriation rules, and the emerging world of tokenized real estate that is giving NRIs entirely new and more tax-efficient ways to gain Indian real estate exposure. Whether you are based in Dubai, Singapore, London, or New York, the rules covered here apply to your situation directly.

NRI Buying Property in India 2026: What Has Changed, What Is New and What You Must Know Before You Sign Any Deal

The landscape for NRI buying property India 2026 has evolved materially from what it was even three years ago. Budget 2024 changed long-term capital gains tax rates, removed indexation benefits for property, and introduced new TDS calculation methods that affect how buyers and sellers structure transactions. Budget 2026 has introduced further amendments to TDS compliance timelines and digital property transaction reporting that every NRI must understand before signing a sale agreement.

NRIs can purchase any number of residential and commercial properties in India without requiring RBI permission. The only restriction under FEMA is on agricultural land, plantation property, and farmhouses, which remain prohibited unless received through inheritance or gift from a resident Indian. There is no limit on the number of urban properties an NRI can own, and no restriction on the number of home loans an NRI can take from Indian banks.

What has changed significantly for NRI property tax India 2026 is the capital gains treatment. The removal of indexation benefit, which previously allowed sellers to adjust cost of acquisition for inflation thereby reducing taxable gains, has increased the effective tax burden for many long-term property holders. NRIs in particular are affected since they often hold properties for extended periods across multiple decades while living abroad in Singapore, Dubai, or the UK.

NRI Property Rules Budget 2026: The One Big Change That Will Make Buying and Selling Property in India Easier From October 2026

The most significant update in NRI property rules Budget 2026 relates to TDS compliance for property transactions involving non-resident sellers. The government has announced a rationalization of the TDS deduction process, with a new online verification system that allows buyers to check an NRI seller’s actual capital gains tax liability in real time before determining the TDS rate to apply. This addresses one of the longest-standing complaints from NRI sellers, which is that buyers routinely deduct TDS at the maximum statutory rate of 30 percent even when the seller’s actual tax liability is far lower.

From October 2026, the process for applying for a Lower TDS Certificate through Form 13 has been streamlined with a mandatory 30-day processing commitment from the Income Tax Department. Previously, delays of 60 to 90 days in Form 13 processing were causing NRI property transactions to collapse or be renegotiated due to cash flow uncertainty for sellers.

Additionally, Budget 2026 has introduced a digital property transaction reporting requirement for all property sales above Rs 50 lakh involving NRI sellers, with mandatory e-filing of Form 26QB by buyers within 30 days of transaction registration. NRIs selling property through power of attorney held by a resident Indian must ensure their representative complies with this new filing timeline or face penalties of Rs 200 per day of default.

FEMA Rules NRI Property India: Which Properties Can NRI Legally Buy and Which Ones Are Completely Off Limits

FEMA rules NRI property India are governed by the Foreign Exchange Management (Acquisition and Transfer of Immovable Property in India) Regulations 2018. Understanding these rules is non-negotiable for any NRI considering Indian real estate investment. The regulations clearly divide properties into permitted and prohibited categories with no grey areas.

Permitted Without RBI Permission

- Residential properties (any number)

- Commercial properties including offices and shops

- Under-construction flats and apartments

- Industrial plots in designated zones

- Properties received by inheritance from resident Indians

Prohibited Without Special RBI Permission

- Agricultural land and farms

- Plantation property of any kind

- Farmhouses and rural agricultural plots

- Land outside designated urban limits

- Properties in restricted border zones

A key practical point for NRIs in Dubai and Singapore: all property purchases must be funded through legitimate banking channels, either by inward remittance in foreign currency or from funds held in an NRE or NRO account. Cash payments from Indian resident friends or family on behalf of the NRI are a FEMA violation even if the NRI later reimburses the resident. The fund trail from foreign source to Indian property must be clean and documented for future repatriation to work.

OCI Property Rules India: Can OCI Card Holders Buy Property in India and Are the Rules Same as NRI

OCI property rules India mirror NRI rules almost exactly. Overseas Citizens of India card holders can purchase any number of residential and commercial properties in India without seeking prior permission from the RBI or FEMA authorities. They are subject to the same restrictions on agricultural land and farmhouses. The tax treatment for capital gains, TDS obligations on property sale, and repatriation rules are identical between NRIs and OCI card holders.

The critical distinction is in the definition. An NRI is an Indian citizen residing abroad for tax purposes, meaning they hold an Indian passport. An OCI card holder has given up Indian citizenship (often by acquiring Singapore, US, UK, or UAE citizenship) but holds an OCI card issued by India as a lifetime visa. Despite the citizenship difference, FEMA treats both categories identically for property investment purposes.

One practical difference we see consistently in our practice: OCI card holders who have been abroad for many years sometimes lose track of their Indian PAN card status, which is mandatory for property registration and TDS compliance. An expired or unavailable PAN creates significant delays in property transactions. Both NRIs and OCIs should ensure their PAN is active and linked to their current Indian bank account before initiating any property transaction in 2026.

NRE NRO Account Property Purchase: Which Account Should NRI Use to Buy Property in India and What Is the Difference

The NRE NRO account property purchase decision is one of the most consequential choices an NRI makes, not just for the purchase itself but for the repatriation of proceeds years later. The account type determines how freely you can move your money back to Dubai, Singapore, the UK, or the US after the property is sold. The following table clarifies the key differences.

| Feature | NRE Account | NRO Account |

|---|---|---|

| Currency | Indian Rupee (funded from abroad) | Indian Rupee (Indian or foreign source) |

| Repatriation | Fully freely repatriable | Up to $1 million per year with compliance |

| Tax on Interest | Tax free in India | Taxable in India at applicable rates |

| Rental Income Credit | Not permitted directly | Rental income can be credited here |

| Property Sale Proceeds | Can be credited if bought via NRE | Credited here with $1M repatriation cap |

| Best For | New purchases funded from abroad | Indian income, rent, existing property |

Our firm’s consistent advice to NRI clients in Dubai and Singapore is to fund new property purchases through the NRE account using foreign inward remittances wherever possible. This creates a clean, fully repatriable fund trail that avoids the $1 million annual cap on NRO repatriation and simplifies the 15CA and 15CB compliance process when you eventually sell the property years later.

NRI Home Loan India 2026: Can NRI Get Home Loan in India, Which Banks Offer It and What Are the Latest Interest Rates

NRI home loan India 2026 eligibility has improved significantly as Indian banks have streamlined their NRI lending processes. All major nationalized and private banks including SBI, HDFC Bank, ICICI Bank, Axis Bank, and Bank of Baroda offer dedicated NRI home loan products. The basic eligibility criteria require the NRI to have a valid Indian passport or OCI card, a minimum of two years of employment abroad with documented salary income, and a credit profile acceptable to the lending bank.

Interest rates on NRI home loans in 2026 typically range from 8.5 percent to 9.5 percent per annum depending on the bank, loan amount, employment type, and whether the NRI is employed in a government or private sector position. NRIs employed in countries like UAE and Singapore with documented salary slips and employment contracts generally receive better rate offers than self-employed NRIs due to income verification simplicity.

Loan EMIs must be serviced from the NRI’s NRE or NRO account in India. The property being purchased serves as collateral for the loan. NRIs cannot service home loan EMIs directly from their overseas bank account to an Indian bank. The funds must flow through the NRI’s Indian NRE or NRO account, creating a documented fund trail that also helps with future repatriation planning.

NRI Selling Property Tax India 2026: How Much Tax Will You Pay and Is It More Than What Resident Indians Pay

NRI selling property tax India 2026 is a subject that requires careful calculation before signing any sale agreement. The tax treatment for NRIs differs from resident Indians in one critical way: the TDS mechanism. While a resident Indian seller is responsible for self-assessment and payment of capital gains tax through their ITR, an NRI seller has the tax deducted at source by the buyer before receiving any payment. This means the NRI’s cash flow is affected immediately, unlike the resident Indian who pays taxes only after filing their return.[2]

For long-term capital gains on properties held more than two years, the tax rate for NRIs is 12.5 percent without the benefit of indexation following the Budget 2024 amendment. This is the same rate applicable to resident Indians, which represents a partial improvement from the previous differential treatment. However, the removal of indexation benefits means properties held for 10, 15, or 20 years no longer get their purchase price adjusted for inflation, significantly increasing the taxable gain and thus the actual tax paid.

Real example from our practice: An NRI client in Singapore purchased a Mumbai flat in 2005 for Rs 40 lakh. They sold it in 2025 for Rs 2.4 crore. Under the old indexation system, the adjusted cost would have been approximately Rs 1.1 crore, creating a taxable gain of Rs 1.3 crore taxed at 20 percent, totalling Rs 26 lakh. Under the new system without indexation at 12.5 percent, the gain of Rs 2 crore (Rs 2.4 crore minus Rs 40 lakh) attracts tax of Rs 25 lakh. The savings are marginal on a 20-year hold period, but for shorter holds the removal of indexation hurts more significantly.

Capital Gains Tax NRI India 2026: Short Term Versus Long Term and Why the Removal of Indexation Benefit Hurts NRI Sellers the Most

| Parameter | Short-Term Capital Gains | Long-Term Capital Gains |

|---|---|---|

| Holding Period | Less than 2 years | 2 years or more |

| Tax Rate NRI | Slab rate (up to 30%) | 12.5% (no indexation) |

| TDS Rate by Buyer | 30% on sale value | 20% on sale value |

| Indexation Benefit | Not applicable | Removed from FY 2024-25 |

| Section 54 Exemption | Not available | Available for reinvestment |

| Form 13 Benefit | Applicable if actual rate lower | Applicable if actual rate lower |

The capital gains tax NRI India 2026 framework clearly incentivizes holding property for more than two years. For NRIs who have held property for long periods in cities like Hyderabad, Bengaluru, or Pune, the absence of indexation is painful but the 12.5 percent LTCG rate remains relatively moderate compared to income tax rates of 30 percent that would apply on short-term gains. Strategic holding period management is one of the most effective tax planning tools available to NRI property investors.

TDS on NRI Property Sale 2026: Why Buyer Has to Pay 30 Percent TDS and How Both Buyer and Seller Can Avoid Overpaying

TDS on NRI property sale 2026 is one of the most misunderstood aspects of Indian real estate transactions. The statutory obligation to deduct TDS falls entirely on the buyer, not the seller. Under Section 195 of the Income Tax Act, any buyer purchasing property from an NRI must deduct TDS before making payment. Failure to deduct TDS makes the buyer personally liable for the tax amount plus interest and penalties, which in large property transactions can run into significant sums.[3]

The standard rates are 20 percent of the sale consideration for long-term capital gains properties and 30 percent for short-term gains properties. Note carefully: TDS is calculated on the entire sale consideration, not just the gain. So if an NRI sells a property for Rs 2 crore, the buyer must deduct Rs 40 lakh at 20 percent TDS before paying. The NRI can later claim a refund if their actual tax liability is lower. However, NRIs in Singapore, Dubai, and the UK often face cash flow problems waiting for Indian tax refunds that can take 6 to 18 months to process.

The solution is the Lower TDS Certificate through Form 13. By computing actual capital gains and applying the correct tax rate with applicable exemptions before the sale, the NRI can apply for a certificate from the Income Tax Department authorizing the buyer to deduct TDS at the lower actual rate. This protects the NRI seller’s immediate cash flow and avoids the inconvenience of waiting for a large refund from Indian tax authorities.

Lower TDS Certificate NRI: What Is Form 13, How to Apply for It and How It Can Save Lakhs in Tax on Your Property Sale

The lower TDS certificate NRI process through Form 13 is one of the most valuable tax planning tools available to NRI property sellers in India. Form 13 is an application submitted to the Assessing Officer (Income Tax) having jurisdiction over the NRI’s PAN. The form requires the NRI to provide details of the property, purchase price, sale price, computation of actual capital gains, applicable exemptions under Section 54 or other provisions, and the resulting actual tax liability.

Once approved, the Income Tax Department issues a certificate specifying the lower TDS rate applicable to the specific transaction. The buyer then deducts TDS at this lower certified rate rather than the standard 20 or 30 percent statutory rate. For a property sold at Rs 3 crore where actual LTCG tax liability after Section 54 exemption is only Rs 8 lakh, the Form 13 certificate could reduce TDS from Rs 60 lakh to Rs 8 lakh, a saving of Rs 52 lakh in immediate cash deduction, even though the final tax payable is the same.

Our firm processes Form 13 applications regularly for NRI clients based in Dubai, Singapore, and the UK. Under Budget 2026’s improved 30-day processing commitment, the timeline for obtaining lower TDS certificates has improved significantly. We recommend NRI sellers initiate Form 13 at least 60 days before the expected property registration date to ensure the certificate is available in time for the buyer to apply the lower rate at registration.

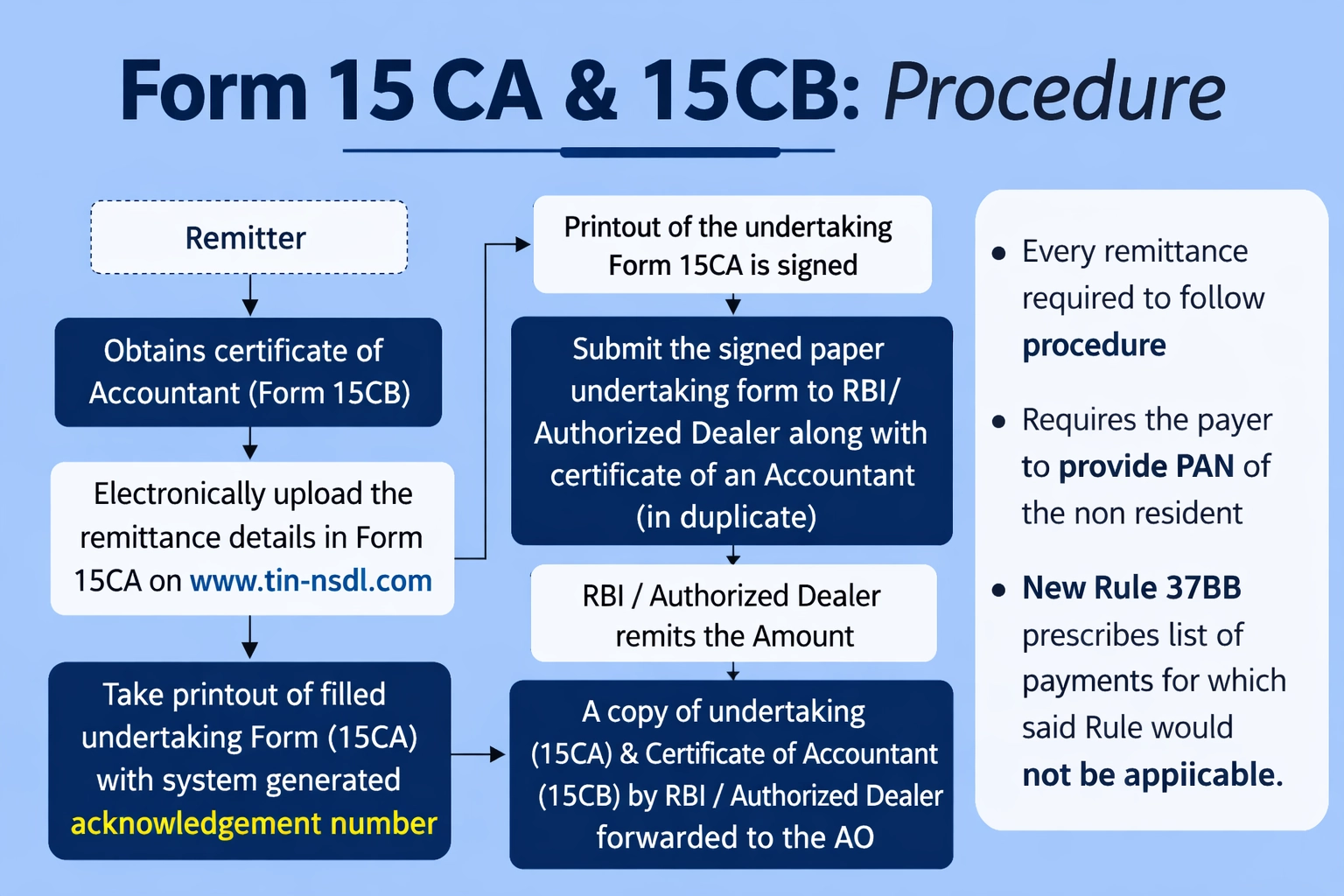

Form 15CA 15CB NRI Property: What These Two Forms Are, Who Fills Them and What Happens If You Skip This Step

Form 15CA 15CB NRI property compliance is mandatory for every repatriation of property sale proceeds from India to an NRI’s overseas account. Without these forms, Indian banks are legally prohibited from processing the international transfer. Form 15CA is a self-declaration filed online on the Income Tax portal by the person making the remittance, confirming that applicable taxes have been paid or deducted on the amount being repatriated.

Form 15CB is a certificate issued by a chartered accountant that verifies the tax compliance of the remittance. The CA certifies that the correct amount of TDS was deducted, that no taxes remain outstanding on the remitted amount, and that the remittance complies with all applicable FEMA regulations. Banks require both 15CA and 15CB before processing any NRI repatriation above specified thresholds.

Skipping this step creates serious consequences. Banks that process international transfers without 15CA and 15CB can face penalties and regulatory action. The NRI remitter can face penalties under FEMA for unauthorized foreign exchange transactions. In our practice, we have seen NRIs based in Dubai who completed property sales but were unable to receive their money for 6 to 12 months because 15CA and 15CB were not prepared in advance. Preparation of these documents should begin simultaneously with property sale negotiations, not after registration.

NRI Repatriation Property Sale: How to Legally Send Your Property Sale Money Abroad and What Is the Maximum Limit Per Year

NRI repatriation property sale rules define how and how much of the sale proceeds an NRI can transfer back to their overseas bank account after selling Indian property. The repatriation limit depends critically on how the property was originally purchased. Properties purchased using foreign inward remittances or funds from NRE accounts have full repatriation rights with no annual cap. The entire sale proceeds, after deduction of applicable TDS and taxes, can be repatriated freely.

For properties purchased using NRO account funds, rental income accumulated in India, or Indian rupee sources, repatriation is capped at USD 1 million per financial year. NRIs with multiple properties or large portfolio values must plan their sale sequencing carefully to stay within annual repatriation limits or obtain specific RBI approval for higher amounts. An NRI in Singapore selling three properties worth Rs 5 crore each in the same financial year would face significant repatriation constraints if the properties were acquired through NRO funds.

The repatriation process requires the NRI to file Form 15CA online, obtain Form 15CB from a CA, present these along with property registration documents, sale deed, tax payment receipts, and PAN card to the authorized dealer bank. Banks are required to process valid repatriation requests within a defined timeline. Having a qualified tax advisor coordinate this process, especially for NRIs not based in India, significantly reduces delays and errors.

Section 54 Exemption NRI: How to Legally Pay Zero Capital Gains Tax on Property Sale by Reinvesting in a New Property

Section 54 exemption NRI is among the most powerful tax saving provisions available under the Income Tax Act for NRI property sellers. The provision allows an NRI who has earned long-term capital gains on the sale of a residential property to claim full exemption from capital gains tax by reinvesting the capital gains amount in the purchase of one new residential property in India. The exemption applies to gains, not to the entire sale consideration, so only the taxable profit needs to be reinvested.

The time conditions for Section 54 are strict. The new property must be purchased within one year before the sale date or within two years after the sale date. For under-construction properties, the construction must be completed within three years of the sale. NRIs who buy a plot and build a new home to claim this exemption should engage a reliable house construction company in cities like Chennai or Bengaluru that can deliver within the three-year deadline, since delays beyond this window result in the exemption being denied. If the capital gains amount cannot be immediately reinvested within the tax filing deadline, the gains can be deposited in a Capital Gains Account Scheme at a scheduled bank and withdrawn for property purchase within the permitted timeline.

The new property purchased under Section 54 must be held for at least three years. If sold earlier, the exemption is reversed and the original capital gains become taxable in the year of the new sale. For NRIs using Section 54, it is essential that the Form 13 application for lower TDS reflects the intended Section 54 reinvestment plan, and that the CA certifying Form 15CB acknowledges the Section 54 exemption computation in the 15CB certificate. Without this coordination, TDS may still be deducted at the full rate despite the exemption entitlement.

DTAA India NRI Property: How Double Taxation Avoidance Agreement Saves NRIs Living in UAE, USA, UK and Singapore From Paying Tax Twice

DTAA India NRI property provisions are particularly valuable for NRIs living in countries that tax worldwide income. India has DTAAs with over 90 countries including the UAE, USA, UK, Singapore, Canada, and Australia. Each DTAA contains specific provisions determining which country has the primary right to tax different types of property income including rental income, capital gains, and repatriated sale proceeds.

UAE NRIs

UAE has no personal income tax. Indian property income is taxed only in India. UAE-based NRIs pay Indian LTCG at 12.5% with no double taxation concern, making UAE the most tax-efficient NRI base for Indian property investment.

UK NRIs

India-UK DTAA allows credit for Indian tax paid against UK tax liability. NRIs must disclose Indian property income to HMRC but can offset Indian TDS paid as foreign tax credit against UK capital gains tax, reducing net tax burden.

Singapore NRIs

Singapore does not tax capital gains. Indian property capital gains are taxed only in India. Singapore-based NRIs are in an advantageous position similar to UAE residents, with no domestic capital gains tax creating additional liability on Indian property sales.

USA NRIs

US taxes worldwide income. Indian capital gains must be reported to IRS but Indian TDS paid can be credited as foreign tax. India-USA DTAA provisions help prevent full double taxation, though US NRIs typically still owe some net US tax after crediting Indian taxes paid.

To claim DTAA benefits in India, NRIs must submit a Tax Residency Certificate from their country of residence and file Form 10F with the Indian Income Tax Department. Without these documents, Indian tax authorities cannot process the DTAA claim and will tax the property income at standard rates applicable to non-residents without treaty relief.

NRI Real Estate Investment India 2026: Which Cities Give the Best Returns and Why Hyderabad Bangalore and Pune Are the Top Picks Right Now

NRI real estate investment India 2026 is increasingly concentrated in three Tier 1 cities that combine strong rental yields with consistent capital appreciation. Hyderabad, Bengaluru, and Pune have consistently delivered 6 to 9 percent gross rental yields on residential property and 8 to 12 percent on Grade A commercial assets, outperforming Mumbai and Delhi NCR where entry prices are higher relative to rental income.

Hyderabad’s HITEC City and Financial District corridors have attracted major global technology corporations and offer some of the most professionally managed residential communities suitable for NRI investment. Property price appreciation in Hyderabad over the 2019 to 2025 period has averaged 8 to 10 percent annually in key IT corridors, outperforming many global real estate markets including parts of Dubai and Singapore on a risk-adjusted basis.

Bengaluru’s Whitefield, Sarjapur Road, and Electronic City corridors serve a rapidly expanding technology workforce driving consistent rental demand. Pune’s Hinjawadi and Baner areas combine automotive and IT sector employment with growing residential supply in the mid-to-premium segment that NRI investors from Singapore and Dubai find attractive for both yield and appreciation. For NRI investors, these three cities also have the most active professional property management ecosystems, which is essential for absentee NRI landlords.

What Is Fractional Ownership and How Can NRI Invest in Indian Real Estate With as Little as Rs 10,000 Without Buying a Full Property

Fractional ownership platforms have opened Indian commercial and residential real estate to NRI investors who previously could not afford the full purchase price of a meaningful investment property. Instead of buying an entire apartment or office for Rs 1 crore or more, fractional platforms allow NRIs to purchase a percentage ownership in a property alongside other investors, proportionally receiving rental income and capital appreciation based on their ownership stake.

Indian fractional ownership platforms like hBits and RealX have served NRI clients from Singapore, Dubai, and the UK who want targeted Indian city exposure without the complexity of direct property ownership abroad. Minimum investment amounts on these platforms range from Rs 10,000 on tokenized platforms to Rs 25 lakh on premium commercial fractional platforms. The choice of entry point determines the asset type, expected yield, and level of platform management involved.

The tax treatment of fractional ownership income depends on the legal structure of the platform. SPV-based fractional platforms treat NRI income as house property income taxable at slab rates. Fractional ownership through platforms structured as securities may attract different tax treatment. NRIs should obtain specific platform tax documentation before investing and ensure the income reporting is compatible with their DTAA position in their country of residence.

Real Estate Tokenization India 2026: Why NRIs Are the Biggest Beneficiaries of Blockchain Based Property Investment and How It Works

Real estate tokenization India 2026 represents the most significant structural shift in Indian property investment since the introduction of REITs in 2019. For NRIs specifically, tokenization removes virtually every barrier that makes direct property investment in India complex: currency transfer, property management, legal title processes, repatriation compliance, and geographic distance. A blockchain-based token representing fractional ownership in a Hyderabad commercial property can be purchased by an NRI in Dubai in minutes through a compliant platform, with rental income automatically distributed to their digital wallet monthly by smart contract.

The tokenization process in India currently operates primarily through SPV structures on platforms like RealX and hBits. The regulatory framework is evolving, with SEBI’s consultation process on digital real estate securities expected to produce formal guidance by 2027. NRIs who invest through compliant SPV-based platforms today are positioned to benefit from both the current income yield and the regulatory clarity that will come as India formalizes its tokenization framework.

For NRI property tax India 2026 purposes, tokenized real estate income currently flows through the SPV and is treated as proportional house property income for the NRI token holder. The same TDS, repatriation, and DTAA rules that apply to direct property ownership apply to tokenized property income. However, the much lower capital commitment, the absence of direct property management responsibilities, and the ability to hold smaller diversified positions across multiple properties makes tokenization structurally more tax-efficient for NRIs managing multiple investment positions.

NRI and Dubai Real Estate Tokenization: How Thousands of Indians Are Already Investing in Dubai Properties Through Digital Tokens From Their Phone

While real estate tokenization India 2026 is still in its regulatory formation phase, Dubai has already moved to Phase 2 of its government-led tokenization program under the Dubai Land Department. For NRIs based in Dubai and for Indian investors looking for international real estate exposure, Dubai’s tokenized real estate market offers a fully regulated, government-backed investment option that is accessible from India through compliant platforms.

Indian investors can use the Liberalised Remittance Scheme to invest up to $250,000 per year in Dubai tokenized real estate, gaining exposure to UAE dirham-denominated and USD-denominated assets with 0 percent capital gains tax in the UAE. The combination of Dubai’s high rental yields of 6 to 8 percent, zero capital gains tax, strong tenant demand from global professionals, and the government registry backing of Dubai Land Department tokenization makes this an increasingly popular choice among sophisticated Indian investors seeking international diversification.

NRIs already based in Dubai can invest in both Indian and Dubai tokenized real estate simultaneously from a single digital platform, building a geographically diversified real estate portfolio that combines India’s capital appreciation potential with Dubai’s rental yield and tax efficiency. This dual-market tokenization strategy is one of the most sophisticated NRI real estate approaches we have seen emerging in our practice across 2025 and 2026.

Model Selection Criteria: 6-Step Framework for NRI Property Investment Decisions in 2026

Tokenized Real Estate Versus Traditional NRI Property Investment: Which One Has Lower Tax, Lower Risk and Higher Liquidity in 2026

| Investment Factor | Tokenized Real Estate | Traditional Direct Property |

|---|---|---|

| Minimum Investment | Rs 10,000 and upward | Rs 30 lakh to crores |

| Liquidity | Secondary market (growing) | Highly illiquid, months to sell |

| TDS Complexity | Handled by platform | Complex, buyer deducts, NRI files |

| Repatriation Process | Platform managed | Full 15CA, 15CB, bank process |

| Management Required | None (platform managed) | Active property management needed |

| Regulatory Framework | Emerging (SPV-based) | Fully established FEMA/IT Act |

Authoritative Principles: 8 Standards Every NRI Property Investor Must Follow in 2026

01. Fund Only Through Banking Channels

All property purchases must be funded through documented banking channels from NRE or NRO accounts. Cash transactions or informal fund transfers violate FEMA and permanently damage repatriation rights.

02. Apply Form 13 Before Listing Property

Lower TDS certificate applications take 30 to 60 days. Begin the process before accepting any buyer offer to ensure TDS is deducted at your actual tax rate rather than the maximum statutory rate.

03. Maintain Complete Transaction Records

Every FEMA-compliant transaction must be documented with bank statements, purchase receipts, NRE or NRO account records, and all correspondence with the property developer. These records are essential for repatriation compliance years later.

04. File Indian ITR Even If TDS Covers All Tax

NRIs with Indian income above the basic exemption limit must file Indian income tax returns regardless of whether TDS has already been deducted. Non-filing attracts notices, interest, and penalties that outweigh the cost of filing compliance.

05. Plan Section 54 Reinvestment Before Sale

If you intend to claim Section 54 exemption, identify your reinvestment property or Capital Gains Account Scheme deposit strategy before the sale completes. Post-sale planning is too late to optimize this exemption effectively.

06. Verify DTAA Documentation Requirements

Tax Residency Certificates and Form 10F must be filed with Indian authorities before DTAA benefits can be applied. Obtain your TRC from your country of residence’s tax authority well before the Indian tax filing deadline.

07. Appoint a Local Indian Tax Representative

NRIs with substantial Indian property holdings should appoint a qualified resident Indian tax advisor or CA as their representative for income tax notices, assessments, and compliance filings to avoid missed deadlines and penalty accumulation.

08. Review Portfolio for Tokenization Opportunities

NRIs with underperforming legacy direct property holdings should evaluate whether fractional or tokenized real estate exposure in growth markets like Hyderabad or Bengaluru offers better risk-adjusted returns with significantly lower compliance burden in 2026.

The Future of NRI Real Estate Investment: How Blockchain, Smart Contracts and Tokenization Will Replace Traditional Property Buying by 2030

The trajectory of NRI real estate investment through 2030 points unambiguously toward blockchain-based property ownership as the dominant model for cross-border fractional investment. The convergence of regulatory maturity in Dubai and Singapore, the ongoing SEBI consultation on digital real estate securities in India, and the massive capital efficiency gains that tokenization offers over traditional property purchase are creating unstoppable structural pressure on the conventional model.

By 2027, India is expected to have a formal regulatory framework for real estate security tokens issued by SEBI. This will create the same institutional clarity for Indian tokenized real estate that SEBI’s REIT regulations created for listed REITs in 2019. NRIs who build familiarity and experience with tokenized real estate platforms now, during the early regulatory formation period, will be positioned advantageously when the formal framework emerges and capital flows accelerate.

Smart contracts will increasingly automate the most painful aspects of NRI property tax India 2026 compliance. Automated TDS deduction and remittance to the Income Tax Department, smart contract-based rental income distribution with embedded withholding tax calculations, and blockchain-recorded ownership transfers that simultaneously update property registries are all technically feasible and actively being piloted across India, Dubai, and Singapore markets. The NRI investor who understands both the current regulatory framework covered in this guide and the emerging tokenization landscape is best placed to navigate the most significant transformation in Indian real estate investment of the coming decade.

Navigate NRI Property Tax India 2026 With Expert Guidance

From TDS planning and DTAA compliance to tokenized real estate entry, our specialists help NRIs across Dubai, Singapore and UK invest smarter in India.

Frequently Asked Questions

Q1.1. How much tax does an NRI pay when selling property in India?

An NRI selling property held for more than two years pays 12.5 percent long-term capital gains tax without indexation benefit after the Budget 2024 change. Short-term gains on property held under two years are taxed at the applicable income slab rate, which can go up to 30 percent for higher income NRIs.

Q2.2. What is TDS on NRI property sale in 2026 and who pays it?

When a buyer purchases property from an NRI seller, the buyer is legally required to deduct TDS at 20 percent for long-term capital gains properties or 30 percent for short-term gains before making payment. The buyer deposits this with the Income Tax Department and the NRI can claim a refund if actual tax liability is lower.

Q3.3. Can an NRI buy agricultural land in India?

No. Under FEMA rules, NRIs and OCI card holders cannot purchase agricultural land, plantation property, or farmhouses in India. They can receive agricultural land only through inheritance or as a gift from a resident Indian relative. Any purchase of restricted property without RBI approval is a FEMA violation with serious penalties.

Q4.4. Which bank account should NRI use to buy property in India, NRE or NRO?

NRIs can use either account, but the NRE account is generally preferred since funds are freely repatriable. Rental income received into an NRO account is repatriable up to $1 million per financial year with proper documentation. Using the wrong account for property transactions can create complications during repatriation of sale proceeds later.

Q5.5. What is Form 15CA and 15CB and does every NRI property sale need them?

Form 15CA is a declaration filed online by the remitter confirming tax has been deducted on a foreign remittance. Form 15CB is a chartered accountant certificate verifying the tax compliance of the remittance. Both are mandatory for repatriating property sale proceeds from India to the NRI’s overseas bank account and must be filed before the bank transfer.

Q6.6. Can an NRI save capital gains tax by reinvesting in another property?

Yes. Section 54 of the Income Tax Act allows NRIs to claim full exemption on long-term capital gains tax by reinvesting the gains in one residential property in India within the specified time limits. The reinvestment must be completed within one year before or two years after the sale, or three years for under-construction property.

Q7.7. Does DTAA help NRIs avoid double taxation on Indian property income?

Yes. India has Double Taxation Avoidance Agreements with over 90 countries including UAE, USA, UK, and Singapore. NRIs can use DTAA provisions to reduce or eliminate tax paid twice on the same property income. However, DTAA benefits require specific documentation including Tax Residency Certificates and Form 10F filing with Indian tax authorities.

Q8.8. What is Lower TDS Certificate and how does an NRI apply for it?

A Lower TDS Certificate, obtained through Form 13 filed with the Income Tax Department, allows the buyer to deduct TDS at an actual tax rate lower than the standard 20 or 30 percent. NRIs whose actual tax liability on the property sale is less than the standard TDS rate should apply for this certificate before the sale completes.

Q9.9. Can OCI card holders buy property in India like NRIs?

OCI card holders can buy residential and commercial property in India under the same rules as NRIs without RBI permission. They cannot buy agricultural land, plantation property, or farmhouses. The same FEMA rules, TDS obligations, capital gains tax treatment, and repatriation limits that apply to NRIs apply equally to OCI card holders.

Q10.10. How much money can an NRI repatriate after selling property in India?

An NRI can repatriate up to USD 1 million per financial year from the sale of up to two residential properties purchased using foreign inward remittances or NRE funds. Proceeds in an NRO account from sale of property acquired through NRO funds or gifts require additional RBI compliance. Repatriation requires 15CA, 15CB, and CA certification.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.