Ai Overview

The global movement toward crypto wallets is not a speculative trend. 5 billion people have entered the crypto wallet ecosystem globally, representing over 40% of the world’s 8. Even Visa reported its stablecoin settlement network reached $7 billion in annualized transaction volume. USDT, issued by Tether, currently has a market cap of approximately $186 billion, making it the largest stablecoin by total value.

Key Takeaways

- ✓ Meta activated Meta USDC Creator Payments on April 29, 2026, via Stripe on Solana and Polygon blockchains, making it the biggest tech platform to deploy stablecoin payouts at scale.

- ✓ The pilot currently covers creators in Colombia and the Philippines, with expansion planned across 160-plus markets throughout 2026, including India, UAE, and Singapore.

- ✓ Solana settles USDC transactions in 400 milliseconds for under $0.001, replacing traditional wire transfers that cost 3 to 7 percent and take three to five days in pilot markets.

- ✓ Meta paid creators nearly $3 billion in 2025, a 35% year-on-year increase, giving the USDC payout pipeline immediate real-world transaction volume on Solana and Polygon.

- ✓ Unlike the failed Libra project, Meta is not issuing its own stablecoin. It uses Circle’s USDC, which is fully audited and aligned with the US GENIUS Act regulatory framework.

- ✓ Stripe, which acquired stablecoin infrastructure firm Bridge, handles the payout rails and crypto-specific tax reporting through its Link wallet service for all Meta creator payouts.

- ✓ USDC is the dominant stablecoin in Western and regulated markets while USDT leads in Asia, India, Turkey, and UAE, creating distinct adoption dynamics for Meta’s global rollout strategy.

- ✓ As creators receive USDC and move funds to exchanges, indirect Bitcoin adoption could accelerate, since USDC acts as an on-ramp to the broader crypto asset ecosystem worldwide.

- ✓ Governments including India and UAE face a looming taxation challenge as creators using USDC for direct transactions without fiat conversion create gaps in current crypto tax frameworks.

- ✓ Meta’s move signals that big tech is becoming the primary driver of blockchain payment infrastructure adoption, with Telegram, Shopify, and other platforms expected to follow rapidly.

Something significant happened on April 29, 2026, and the global payments industry will not look the same after it. Meta, the company behind Facebook, Instagram, and WhatsApp, quietly activated stablecoin payouts for creators, allowing them to receive earnings directly in USDC on the Solana and Polygon blockchains. No press conference. No advertising blitz. Just a quiet update to Meta’s Business Help Center that sent shockwaves through the fintech, crypto, and creator economy worlds simultaneously.

For our team, which has spent eight-plus years tracking the convergence of blockchain technology with mainstream consumer platforms, this moment is not a surprise. It is a confirmation. The infrastructure has been maturing, the regulatory environment has been shifting, and the creator economy has been demanding better cross-border payment solutions. Meta’s Crypto Payment move is the moment where all of these forces aligned into a single, commercially deployed product used by real creators earning real money.

This is not a small experiment. Meta has 3.1 billion monthly active users on Facebook, over 2 billion on Instagram, and over 2 billion on WhatsApp across 180 countries. Even in its current pilot stage, the Meta USDC creator payments program touches a platform scale that no previous blockchain payment initiative has ever reached. What happens next in Colombia and the Philippines will determine the trajectory of stablecoin adoption for billions of people across India, UAE, Singapore, and the world.

Why Billions of Users Are Moving Toward Crypto Wallets

The global movement toward crypto wallets is not a speculative trend. It is a measurable, accelerating behavioral shift driven by practical financial necessity. Approximately 3.5 billion people have entered the crypto wallet ecosystem globally, representing over 40% of the world’s 8.4 billion population. This figure is no longer driven primarily by speculative investors chasing Bitcoin price movements. It is increasingly driven by everyday users in emerging markets seeking faster, cheaper, and more accessible financial tools than their local banking systems provide.

In India, crypto wallet adoption has been fueled by a combination of rising smartphone penetration, UPI payment familiarity, and growing awareness of stablecoins as a dollar-equivalent savings tool in a period of INR volatility. In Dubai and across the UAE, high-net-worth individuals and expatriate workers making cross-border remittances have driven crypto wallet adoption well above global averages. In Singapore, the MAS-regulated digital asset environment has created a sophisticated institutional and retail crypto wallet user base.

What unites these diverse user groups is a shared frustration with traditional banking rails. International wire transfers are slow, expensive, and restricted by banking hours. For a creator in the Philippines earning dollars on Instagram, waiting three to five days for a wire transfer that costs up to 7% of the payout amount is not a minor inconvenience. It is a structural tax on their livelihood. USDC on Solana, settling in 400 milliseconds for under one cent, is not an incremental improvement. It is a category transformation. Meta’s decision to deploy this technology for its creator base is simply the largest-scale acknowledgment yet that crypto wallets are ready for mainstream payment infrastructure.To stay updated on the latest trends in social media and blockchain, you can follow platforms like Snap Story America, which are integrating these technologies for smoother transactions.

Meta’s Massive User Base and Its Global Influence

To understand why Meta USDC creator payments represent a watershed moment for the global payments industry, you first need to appreciate the sheer scale of what Meta operates. Facebook has approximately 3.1 billion monthly active users, making it the largest social network in human history. Instagram has over 2 billion monthly active users across every major country. WhatsApp serves over 2 billion users across 180 countries and is the primary messaging application in India, UAE, large parts of Europe, Latin America, and Southeast Asia. Together, Meta’s platforms reach approximately 3.6 billion unique users, which represents roughly 43 percent of the entire world population.

This scale is the critical differentiator that separates Meta USDC creator payments from every previous stablecoin payment initiative. PayPal launched its own stablecoin PYUSD in 2023 to a modest reception. Stripe resumed crypto payouts the same year. Even Visa reported its stablecoin settlement network reached $7 billion in annualized transaction volume. All of these are meaningful milestones, but none of them approach the distribution potential of a platform where over 3 billion people are already logged in and transacting daily.

Meta paid its creator base nearly $3 billion in 2025 alone, a 35 percent increase from the previous year. That is $3 billion in real money that could now flow through Solana and Polygon if the USDC program scales globally. For context, Solana already processes over 167 million monthly active wallets. Adding Meta’s creator payment volume to that network is not a marginal upgrade. It is a validation of Solana and Polygon as enterprise-grade global payment rails that will be noticed by every financial institution, fintech company, and competing social platform watching this pilot unfold.

Meta Announces Creator Payments in USDC Stablecoin

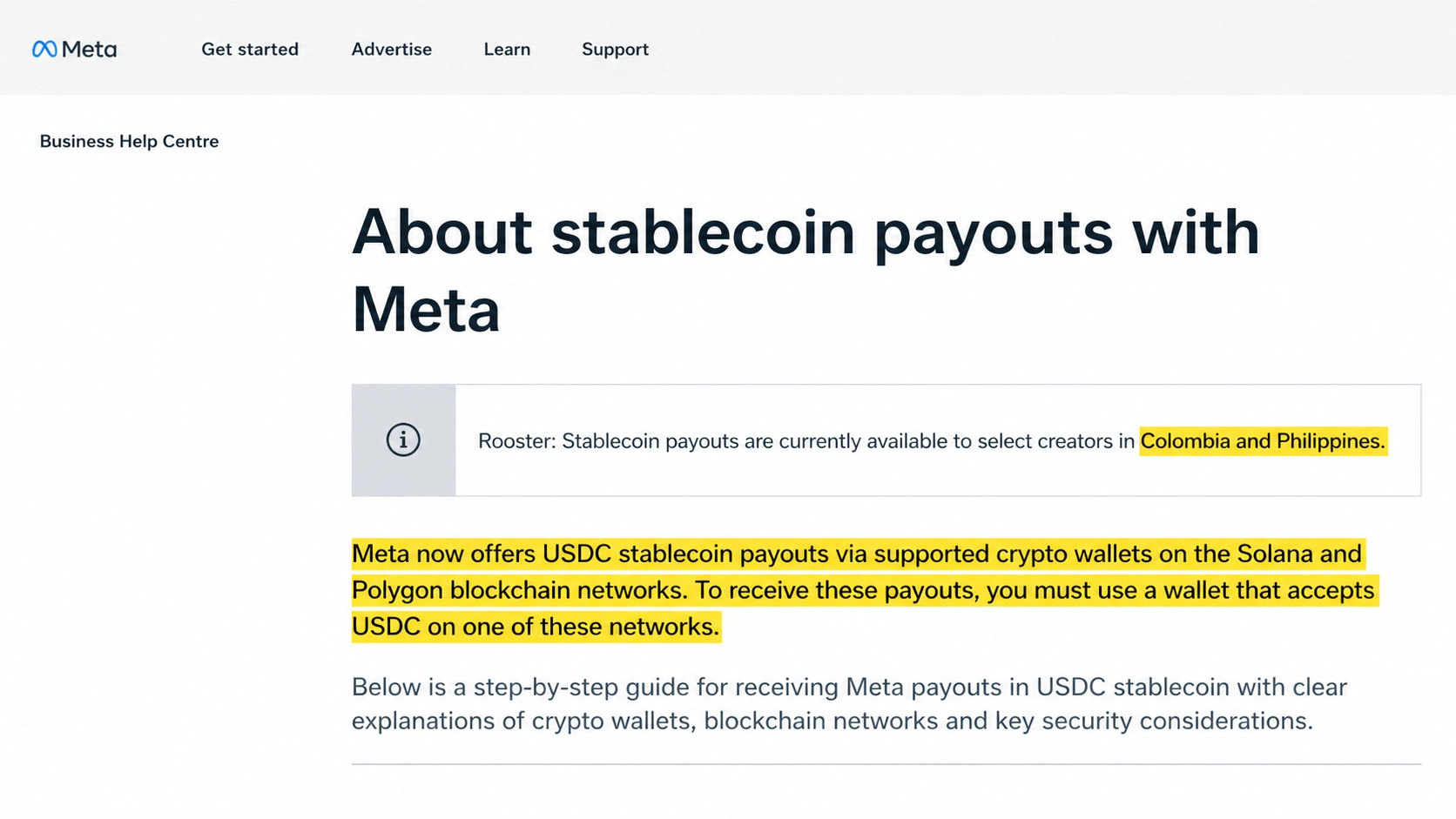

April 29, 2026 · Meta Business Help Center

“Meta now offers USDC stablecoin payouts via supported crypto wallets on the Solana and Polygon blockchain networks. To receive these payouts, you must use a wallet that accepts USDC on one of these networks.”

Source: Meta Business Help Center, confirmed by CoinDesk, Fortune, and PYMNTS

On April 29, 2026, Meta quietly updated its Business Help Center to confirm that USDC stablecoin payouts were now live for eligible creators in Colombia and the Philippines. The announcement came with no fanfare. No press release. No Mark Zuckerberg keynote. Just a factual update to a help page that was picked up by CoinDesk and immediately rippled across the global crypto and fintech media ecosystem.

The Meta USDC creator payments program works straightforwardly. Eligible creators who monetize through Facebook, Instagram, or WhatsApp opt in through their existing monetization settings. They enter a compatible crypto wallet address, such as MetaMask or Phantom on Solana, or GCash’s GCrypto and Coins.ph for Philippine-based creators. Once linked, their earnings arrive in USDC instead of fiat currency, settling on-chain in under a second. Meta generates standard tax forms such as Form 1099 or 1042 covering total earnings, while Stripe separately provides crypto-specific tax documentation for the digital asset transactions.

One important detail that Meta has been explicit about: the company does not offer fiat conversion services. Creators who receive USDC and want local currency must convert through third-party crypto exchanges independently. This design choice is deliberate. It keeps Meta in the role of a payment distributor rather than a financial institution, reducing regulatory complexity while still delivering the core value of instant, low-cost cross-border stablecoin payouts to creators who need them most.

How Facebook Instagram and WhatsApp Form the Meta Ecosystem

The true strategic power of Meta USDC creator payments lies not in any single platform but in the combined ecosystem that Meta operates. Facebook, Instagram, and WhatsApp are not merely three separate apps. They are a unified distribution network for human attention, communication, and increasingly, commerce, that operates at a scale no other private company in history has approached. Understanding how these three platforms interact is essential for grasping why Meta’s stablecoin move carries implications far beyond a simple creator payout program.

Facebook remains the world’s largest social network, with particular strength in markets across India, Southeast Asia, Latin America, and Africa where it is often synonymous with the internet itself. Instagram has become the dominant creator monetization platform for visual content, with its Reels, Stories, and subscription features generating billions in creator payouts annually. For those looking to view or analyze these stories, Instagram Stories offers a useful tool. WhatsApp is the world’s default messaging app in India, UAE, and across Southeast Asia, with over 100 billion messages sent daily and a rapidly growing commerce layer through WhatsApp Business.

When Meta activates USDC payments across this ecosystem, it is not limited to content creators on Instagram. It creates a potential payment layer that touches every creator, business owner, and active user across all three platforms simultaneously. A merchant in Dubai running Facebook Ads, a creator in India publishing Instagram Reels, and a small business in Singapore using WhatsApp Business for customer payments could all eventually be participants in the same blockchain payment infrastructure that Meta is now piloting in Colombia and the Philippines.

Role of Stripe in Enabling Instant Crypto Payments

Stripe’s role in the Meta USDC creator payments program is not incidental. It is foundational. Stripe has been positioning itself as what its leadership calls the “AWS of payments,” a backend infrastructure layer that other companies build financial products on top of. The company’s 2024 acquisition of Bridge, a stablecoin infrastructure firm, gave Stripe the technical capability to process, settle, and report on stablecoin transactions at institutional scale. The Meta partnership is the largest public deployment of this capability to date.

Jay Shah, head of Link at Stripe, confirmed the partnership in a public statement: “Businesses can now send stablecoin payouts directly to customers using Link. We’re already partnering with Meta so their creators can receive stablecoins in their Link wallets in countries like the Philippines and Colombia.” This statement from a senior Stripe executive publicly confirmed not just the current pilot but the broader ambition. Link is Stripe’s customer checkout infrastructure, and enabling stablecoin payouts through it signals that crypto payments are now a first-class payment method within Stripe’s product suite, not an experimental add-on.

Stripe’s infrastructure handles multiple critical functions in the Meta USDC creator payments stack. It manages the wallet linking process, validates creator eligibility, settles USDC transactions on Solana and Polygon, and generates the crypto-specific tax documentation that creators need for compliance. Creators receive standard earnings forms from Meta and separate digital asset documentation from Stripe, creating a dual-reporting framework that attempts to satisfy both traditional tax requirements and the evolving digital asset reporting standards being formalized under the US GENIUS Act.

What USDC Stablecoin Is and How It Works

For anyone new to stablecoins, the concept is straightforward and important to understand before grasping the full significance of Meta USDC creator payments. USDC, which stands for USD Coin, is a stablecoin issued by Circle. A stablecoin is a type of cryptocurrency designed to maintain a fixed value against a reference asset, in this case the US dollar. This means that 1 USDC always equals 1 US dollar, regardless of what is happening in the broader crypto market. Bitcoin and Ethereum fluctuate in price daily. USDC does not.

USDC maintains its dollar peg through a reserve-backing model. For every USDC token in circulation, Circle holds one dollar worth of cash or short-term US Treasury bills in regulated financial institutions. Circle publishes monthly attestation reports from independent auditors confirming these reserves, which is a key reason why regulators and institutional players prefer USDC over alternatives with less transparent backing. The entire USDC supply is audited, documented, and verifiable, giving it a level of trust that other stablecoins have struggled to match.

On the technical side, USDC operates as a smart contract token on multiple blockchain networks. Meta’s current implementation uses Solana and Polygon. On Solana, USDC transactions settle in approximately 400 milliseconds, the time it takes to blink, for a fee of less than one cent. This is the core operational advantage that makes USDC on blockchain networks fundamentally superior to traditional wire transfers for cross-border creator payments. The same payment that costs up to 7 percent and takes five business days through correspondent banking costs a fraction of a cent and arrives in under a second on Solana.

Traditional Wire Transfer

- ✗ Settlement: 3 to 5 business days

- ✗ Fees: 3 to 7 percent per transfer

- ✗ Banking hours required

- ✗ Intermediary banks involved

USDC on Solana (Meta)

- ✓ Settlement: Under 400 milliseconds

- ✓ Fees: Under $0.001 per transaction

- ✓ Available 24 hours, 7 days a week

- ✓ Direct wallet-to-wallet, no intermediaries

Difference Between USDT and USDC in Global Markets

A common question when discussing Meta USDC creator payments is why Meta chose USDC rather than USDT, the world’s largest stablecoin by market capitalization. Both are dollar-pegged stablecoins, but they differ significantly in their governance model, regulatory alignment, and geographic adoption patterns. Understanding this distinction explains both Meta’s strategic choice and the varying reception that this announcement will receive across different markets.

USDT, issued by Tether, currently has a market cap of approximately $186 billion, making it the largest stablecoin by total value. However, Tether has historically faced scrutiny over its reserve disclosures and has been less transparent about the composition of its backing assets compared to Circle’s USDC. This opacity has made regulators in the United States, European Union, and other Western jurisdictions cautious about USDT as a regulated payment instrument. For a company like Meta that operates under intense regulatory scrutiny, using USDT would have introduced significant compliance risk.

| Factor | USDC (Circle) | USDT (Tether) |

|---|---|---|

| Market Cap (2026) | ~$58 billion | ~$186 billion |

| Reserve Transparency | Full monthly audits | Limited attestations |

| Regulatory Alignment | GENIUS Act aligned | Limited regulatory integration |

| Preferred Regions | USA, Europe, Singapore | Asia, India, UAE, Turkey |

| Meta Partnership | Yes (April 2026) | No |

Why USDT Is Popular in Asia and USDC in Western Countries

The geographic split between USDT and USDC adoption is one of the most interesting dynamics in the global stablecoin market, and it has direct implications for how Meta USDC creator payments will be received across different markets. In broad terms, USDT dominates trading volume and retail adoption across Asia, including India, UAE, Turkey, and much of Southeast Asia. USDC commands stronger institutional and regulatory acceptance across Western Europe, the United States, and increasingly Singapore as a regulated financial hub.

The reasons for this geographic split are rooted in history and market access. USDT became the default trading pair on most Asian crypto exchanges because it launched first and achieved liquidity depth before USDC entered the market. In India, where crypto trading volume through exchanges like WazirX and CoinDCX is dominated by retail investors seeking quick trading pairs, USDT’s established liquidity made it the natural default. In Dubai’s crypto trading community, USDT serves as the bridge currency for most peer-to-peer transactions given its deep market depth.

For Meta’s rollout strategy, this geographic preference split creates an interesting challenge. When Meta USDC creator payments expand to India and UAE, creators in those markets who receive USDC will need to convert it to their preferred assets through exchanges that likely hold deeper USDT liquidity. This is not a barrier to adoption. It is an on-ramp friction point that can be resolved through exchange integrations and education. But it does mean that Meta’s expansion into Asian markets will require additional infrastructure coordination to ensure smooth creator experience.

Meta’s Previous Attempt with Libra and Why It Failed

To fully appreciate the significance of Meta USDC creator payments, you need to understand why Meta’s first attempt at crypto payments failed so spectacularly. In 2019, Meta, then operating as Facebook, announced Libra, an ambitious plan to create a global digital currency that would allow its billions of users to send and receive money as easily as sending a message. Mark Zuckerberg’s vision was compelling: a borderless, low-cost currency for the people who were underserved by traditional banking, which described a large proportion of Meta’s user base across India, Africa, and Southeast Asia.

The global regulatory response was immediate and overwhelming. Lawmakers in the United States, European Union, United Kingdom, and dozens of other jurisdictions reacted with alarm to the prospect of a private company with billions of users controlling its own global currency. The US Congress grilled Zuckerberg in public hearings. European regulators threatened to block the project outright. The Bank of England warned about systemic financial stability risks. Libra’s founding consortium, which initially included Visa, Mastercard, PayPal, and others, began falling apart as corporate members withdrew to avoid regulatory confrontation.

The core problem was structural. Regulators were not opposed to digital payments. They were opposed to Meta controlling an entire monetary system. The combination of Meta as stablecoin issuer, Meta as the wallet provider, and Meta as the primary payment network created a concentration of financial power that no regulatory framework in 2019 was prepared to accept from a private technology company. Libra was eventually rebranded as Diem, narrowed in scope, and sold to Silvergate Capital for approximately $200 million in January 2022 before being shut down entirely.

From Libra to Diem and the Regulatory Pressure on Meta

The journey from Libra to Diem to the current Meta USDC creator payments program illustrates how regulatory pressure ultimately shaped a better product than the original vision. After Libra collapsed under regulatory opposition in 2019 and 2020, Meta rebranded the project as Diem in December 2020, attempting to signal a more modest and regulatory-compliant ambition. Diem would be a simpler, US-dollar-backed stablecoin rather than the basket-currency originally proposed for Libra. But the regulatory damage was done. Regulators who had expressed opposition to Libra did not significantly change their position for Diem, and the project never launched publicly.

What changed between 2022 and 2026 is the regulatory environment itself. The election of a more crypto-friendly US administration, the advancement of the GENIUS Act as a formal stablecoin regulatory framework, and the demonstrated success of regulated stablecoins like USDC in institutional use cases collectively created a window of regulatory tolerance that simply did not exist when Diem was attempting to operate. Meta recognized this shift and began quietly exploring stablecoin options again in 2025.

The strategic genius of the current USDC approach is what Meta is not doing. It is not issuing its own stablecoin. It is not operating its own wallet infrastructure. It is not positioning itself as a financial institution. Instead, Meta is purely a customer of existing, regulated infrastructure. Circle issues USDC. Stripe handles the payments. Solana and Polygon process the transactions. Meta simply integrates these services into its existing creator payout system. This three-party model removes every regulatory objection that killed Libra while still delivering the same core user value.[1]

Current Rollout in Colombia and Philippines Explained

The selection of Colombia and the Philippines as the launch markets for Meta USDC creator payments was not random. Both countries share a set of characteristics that make them ideal testing grounds for blockchain-based creator payouts, and both illustrate the pain points that USDC on Solana directly addresses. Creators in these markets earn their income in US dollars through Meta’s platforms but live in economies where converting those dollars into local currency through traditional banking channels is expensive, slow, and sometimes inaccessible.

In the Philippines specifically, the creator economy is substantial and growing rapidly. The country has one of the highest rates of social media engagement in Asia, with a large population of English-speaking content creators who monetize through Facebook and Instagram. Traditional international wire transfers for these creators cost between 3 and 7 percent per transfer and take three to five business days to clear. For a creator receiving $500 monthly in Meta earnings, that fee structure represents $15 to $35 in losses every single month, purely from the payment infrastructure inefficiency.

USDC on Solana eliminates this friction entirely. The same $500 payout arrives in the creator’s wallet in under a second for a fee of less than one cent. The creator can then decide independently what to do with the USDC: convert it to Philippine pesos through Coins.ph, hold it as a dollar-denominated savings asset, or convert it to other crypto assets. Meta’s decision to not offer conversion services is actually liberating in this context. It gives creators full financial autonomy over their earnings once they arrive on-chain, which is a meaningful upgrade over the controlled, fee-heavy fiat withdrawal systems of traditional platforms.

How Platforms Scale Crypto Adoption Step by Step

The pattern of how major platforms scale crypto adoption follows a consistent and observable playbook that our team has tracked across eight-plus years of working in this space. It always begins small: one region, one asset, one use case, limited user eligibility. The purpose is not timidity. It is risk management and regulatory learning. By starting with a contained pilot, the company can identify technical issues, compliance gaps, user behavior patterns, and regulatory responses before committing to global deployment.

Crypto exchanges followed this exact pattern. Most began with Bitcoin and Ethereum only, in a single geographic market with limited fiat on-ramp options. Over time they added more assets, more markets, more payment methods, and more financial products. The largest exchanges today offering hundreds of trading pairs and sophisticated financial instruments all started from a single-asset, single-market pilot phase. Meta’s USDC rollout is following the same playbook at a far larger scale.

The expected scaling trajectory for Meta USDC creator payments based on historical platform patterns looks something like this. Colombia and Philippines launch in April 2026. Additional Latin American and Southeast Asian markets follow in the second half of 2026. India, UAE, and Singapore enter the expansion wave as regulatory clarity in those jurisdictions is confirmed. By 2027, USDC payouts become a standard offering across all Meta creator programs globally. And then comes the next phase: accepting crypto payments from advertisers, enabling peer-to-peer transfers within apps, and expanding into financial services that Telegram is already beginning to pioneer for its large global user base.

Meta USDC Scaling Roadmap (Predicted Pattern)

How USDC Payments Could Drive Bitcoin Adoption Indirectly

One of the most underappreciated second-order effects of Meta USDC creator payments is the indirect acceleration it may provide to Bitcoin and broader crypto asset adoption. The mechanism is straightforward and grounded in observable user behavior patterns from previous stablecoin adoption cycles. When users receive USDC for the first time through a trusted, familiar platform like Meta, they inevitably engage with the crypto ecosystem for the first time or more deeply than before. And the crypto ecosystem, once entered, has a strong tendency to lead users toward other digital assets.

Consider the typical creator journey after receiving their first USDC payout. They open a compatible wallet, link it to their Meta account, and receive USDC. Now they have a crypto wallet for the first time. They can see their balance. They can see what other assets are available. They might convert some USDC to Bitcoin as a store of value hedge. They might explore DeFi yield options. They might simply hold the USDC and convert it to local currency through an exchange that shows them the rest of the crypto market as they navigate to the withdrawal function. Each of these actions deepens their engagement with the blockchain ecosystem.

At Meta’s scale, even a small percentage of creators who expand from USDC into other crypto assets represents tens of millions of new or deeper crypto participants. For Bitcoin specifically, institutional adoption has already driven prices above $100,000. But sustained long-term Bitcoin adoption requires the kind of grassroots retail onboarding that Meta USDC creator payments could deliver organically, without requiring creators to specifically seek out Bitcoin. USDC becomes the gateway, and the crypto ecosystem becomes the destination for those who want to explore further.

Future Possibility of Meta Accepting Crypto Payments

The logical progression from Meta paying creators in USDC is Meta eventually accepting crypto payments from users and advertisers on its platforms. This is not speculation. It is the natural product evolution that every company deploying crypto payment infrastructure has followed once they establish the foundational payment rails. PayPal started with stablecoin issuance and is now exploring broader crypto payment acceptance. Stripe moved from crypto payouts to broader stablecoin payment infrastructure. Meta’s current creator payout program is almost certainly step one in a multi-phase blockchain payments strategy.

Think about what accepting crypto payments from advertisers would mean for Meta’s business. Businesses running Facebook and Instagram advertising campaigns currently pay in fiat currency through credit cards, bank transfers, or PayPal. If Meta enables USDC payment for advertising purchases, it creates a closed-loop system where creators earn USDC and advertisers spend USDC, with Meta capturing the transaction fees and data value in between. This is not a distant futuristic scenario. It is a commercially logical next step that Telegram is already beginning to explore with its large global user base offering crypto-related services.

There is also a strong possibility that Meta will eventually launch its own crypto wallet as a standalone financial product. The company already operates Novi, a digital wallet product that has been dormant since the Libra collapse. Reviving and relaunching Novi with USDC support and a broader range of financial services would align perfectly with Meta’s stated long-term ambition to provide financial infrastructure for underserved populations globally. Once that happens, the prediction is that other major social media, content, and commerce platforms will accelerate their own crypto payment integration timelines to remain competitive.

Taxation Challenges When Crypto Is Used Without Converting to Fiat

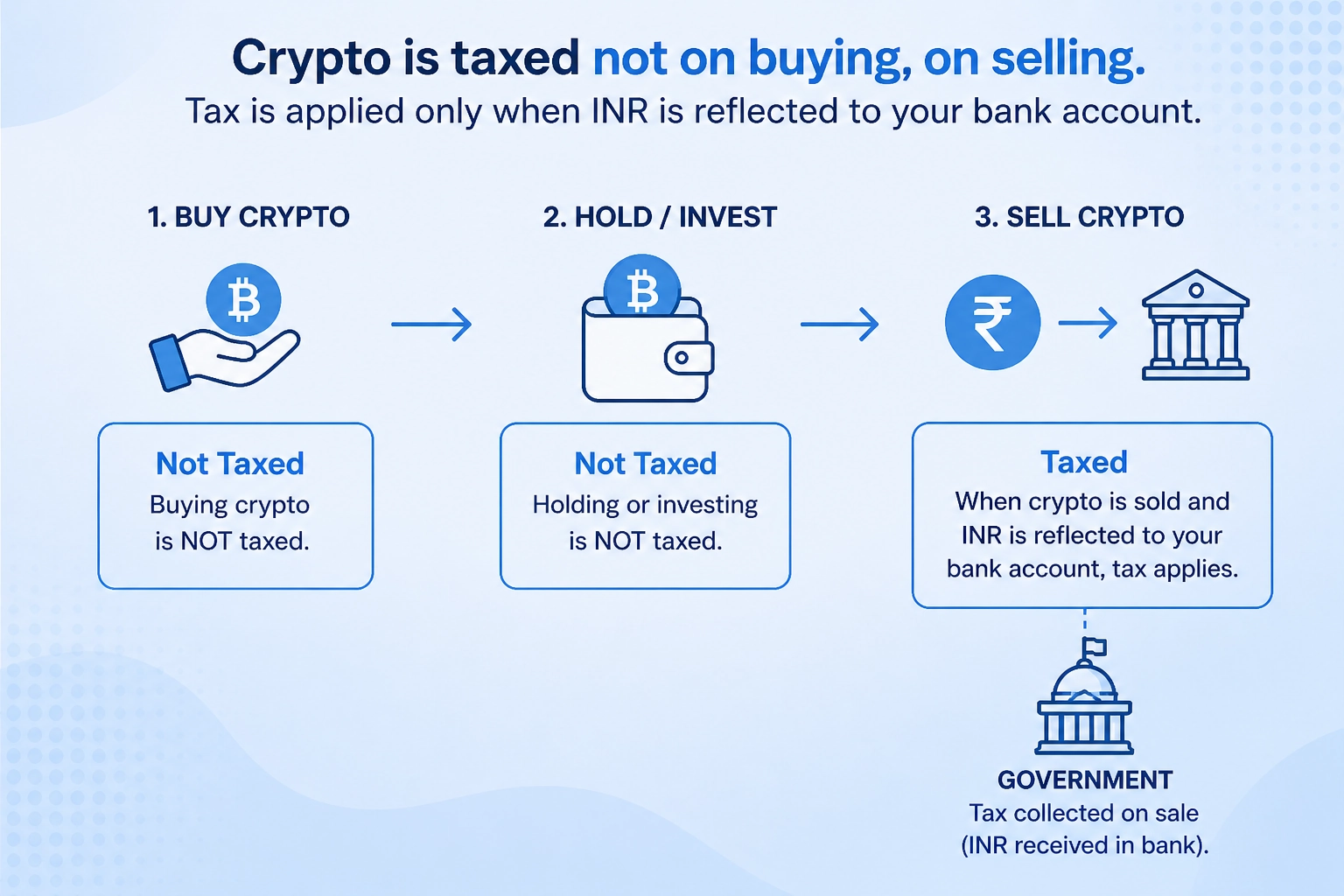

Perhaps the most profound long-term implication of Meta USDC creator payments is the regulatory and taxation challenge it creates when crypto assets are used for real economic activity without ever being converted to fiat currency. Most countries currently tax crypto at the point of fiat conversion. In India, for example, crypto gains are taxed at 30% when sold and converted to INR. In the UAE, crypto transactions are generally untaxed for individuals, but corporate activities may attract VAT. In Singapore, MAS treats crypto assets as property for tax purposes, with gains taxed under specific conditions.

Finally, there is a big question around government taxation. In most countries, crypto is taxed when it is converted into fiat currency (like INR) and transferred to a bank account. Buying crypto is usually not taxed, but selling is.

So if users start using crypto directly for daily transactions without converting it into fiat, it becomes unclear how governments will apply taxes in such scenarios.

The current frameworks assume that the primary use case for crypto is speculative trading with eventual conversion to fiat. But Meta USDC creator payments represent a different paradigm entirely. A creator who receives USDC, holds it, and uses it to pay for goods and services without ever converting to INR or AED never triggers the traditional tax recognition event under current frameworks. As more creators adopt this behavior at scale, governments will face mounting pressure to develop new tax frameworks that capture economic activity occurring entirely within the on-chain economy.

This is not a theoretical concern. Stripe already issues crypto-specific tax documents to creators receiving Meta USDC payouts. Meta separately generates standard earnings forms. But the documentation frameworks were designed for traditional fiat transactions. As the on-chain economy grows, the gap between what tax authorities can document and what actually occurs in creator wallets will widen. India, UAE, and Singapore tax authorities are among the most technologically sophisticated in their regions, and all three are likely to be among the first to develop blockchain-native tax reporting standards that address this emerging gap directly.

India

30% tax on crypto gains when converted to INR. Direct USDC spending may create a taxation grey area that SEBI and income tax authorities are yet to formally address.

UAE (Dubai)

No personal crypto tax for UAE residents. However, corporate entities using USDC for business transactions may face VAT obligations under FTA guidelines.

Singapore

MAS treats crypto as property. Creator income in USDC is likely taxable as income. Ongoing use without fiat conversion creates documentation challenges for IRAS reporting.

USA

IRS treats crypto as property. USDC earnings are income. Using USDC for purchases triggers capital gain events even for stablecoins, creating significant tax complexity for creators.

This Is the Moment the Internet’s Payment Layer Began to Change

Meta USDC creator payments is not just a new payout option for Instagram creators. It is the opening move in the largest stablecoin payment deployment in history, executed by the company with more logged-in users than any other platform on earth. When Meta’s USDC pilot scales across 160-plus markets throughout 2026, it will bring stablecoin payments to a scale of users, creators, and economic activity that no blockchain payment initiative has previously reached.

For creators in India, UAE, and Singapore, the implications are direct and near-term. Faster payouts. Lower fees. Dollar-denominated earnings that bypass expensive fiat conversion. For the broader fintech and blockchain ecosystem, Meta’s move validates Solana and Polygon as enterprise payment infrastructure, strengthens USDC’s position as the regulated stablecoin of choice for mainstream platforms, and signals that the next phase of internet payments will be built on blockchain rails.

The internet is changing its payment layer. Meta just fired the starting gun. What follows in Colombia and the Philippines today will arrive in every major market in the world very soon. The platforms, creators, businesses, and governments that understand this shift now will be the ones best positioned to capture its opportunities and navigate its challenges when it arrives at full global scale.

Ready to Build on Stablecoin Payment Infrastructure?

Our team builds blockchain payment systems for platforms in India, UAE, and Singapore. From USDC integration to full Web3 payment rails, we deliver production-ready solutions.

Frequently Asked Questions

Q1.1. What is Meta doing with USDC and why is it a big deal?

Meta activated USDC stablecoin payouts for select creators on April 29, 2026, using Solana and Polygon blockchains via Stripe. This makes Meta one of the largest tech companies to use blockchain rails for real-world creator earnings distribution globally.

Q2.2. Which countries can get Meta USDC creator payments right now?

The Meta USDC creator payments pilot launched in Colombia and the Philippines. These markets were chosen because creators there earn in US dollars but face slow, expensive traditional banking rails, making USDC on Solana a significantly faster and cheaper alternative.

Q3.3. How do creators receive USDC from Meta?

Eligible creators opt in through their Meta monetization settings, enter a compatible crypto wallet address such as MetaMask or Phantom, and start receiving earnings directly in USDC on either the Solana or Polygon blockchain network, processed by Stripe.

Q4.4. What is Stripe's role in Meta USDC creator payments?

Stripe acts as the payment infrastructure partner, handling USDC payout delivery through its Link wallet service, processing crypto-specific tax reporting, and settling transactions on Solana and Polygon. Jay Shah, head of Stripe Link, confirmed the partnership publicly.

Q5.5. Why is Meta using USDC instead of making its own coin again?

After Libra and Diem failed due to regulatory opposition, Meta chose to use Circle’s USDC, which is audited and aligned with the US GENIUS Act framework. This lets Meta operate as a customer of existing infrastructure rather than a regulated stablecoin issuer.

Q6.6. What is the difference between USDC and USDT?

Both are stablecoins pegged 1:1 to the US dollar. USDT has a larger market cap of approximately $186 billion but historically less transparent reserves. USDC has stronger regulatory alignment and is preferred by Western platforms like Meta and Stripe due to its audited, fully backed reserves.

Q7.7. Will Meta USDC payments expand to India, UAE, and Singapore?

Meta has announced plans to expand stablecoin payouts globally across 160-plus markets throughout 2026. India, UAE, and Singapore are among the high-priority targets given their large creator populations and significant cross-border payment costs through traditional banking channels.

Q8.8. Can creators convert USDC to local currency through Meta?

No. Meta explicitly does not offer fiat conversion services. Creators who want to convert USDC to INR, AED, SGD, or other local currencies must use third-party crypto exchanges independently. Meta strictly handles the USDC payout delivery only.

Q9.9. How fast are USDC payments on Solana compared to bank transfers?

USDC transactions on Solana settle in approximately 400 milliseconds with fees under $0.001 per transaction. Traditional international wire transfers for creators in Colombia and the Philippines typically take three to five days and cost between 3% and 7% in fees.

Q10.10. Could Meta eventually accept crypto payments from advertisers and buyers?

This is a strong possibility. Meta is already paying creators in USDC. The logical next step in the company’s long-term blockchain payment strategy would be accepting crypto from advertisers, enabling peer-to-peer payments within its apps, and potentially launching its own crypto wallet infrastructure.

Explore Services

Related Services

Reviewed by

Aman Vaths

Founder of Nadcab Labs

Aman Vaths is the Founder & CTO of Nadcab Labs, a global digital engineering company delivering enterprise-grade solutions across AI, Web3, Blockchain, Big Data, Cloud, Cybersecurity, and Modern Application Development. With deep technical leadership and product innovation experience, Aman has positioned Nadcab Labs as one of the most advanced engineering companies driving the next era of intelligent, secure, and scalable software systems. Under his leadership, Nadcab Labs has built 2,000+ global projects across sectors including fintech, banking, healthcare, real estate, logistics, gaming, manufacturing, and next-generation DePIN networks. Aman’s strength lies in architecting high-performance systems, end-to-end platform engineering, and designing enterprise solutions that operate at global scale.